Only fools believe stock surge is just the ‘Magnificent 7’ — It’s not

Current mythology claims “just a handful of stocks” took the S&P 500 to new highs. Supposedly AI hype driving the “Magnificent 7” Tech stocks in a 2000-era bubblicious redux. Wrong. That just grasps at straws to dismiss the bull market so few foresaw. No, this bull market is a magnificently broad celebration of normalcy’s return. That so few fathom that means it has far further to run. Let me show you.

Sure, the Magnificent 7 boomed. That much is true. Alphabet (Google’s parent), Amazon, Apple, Meta (Facebook’s parent), Microsoft, Nvidia and Tesla—raced like Secretariat since 2022’s bear market bottom. And all but Tesla are Tech or Tech-like with AI exposure.

But every bull market has leaders and laggards. Normally, categories of stocks falling the most in a bear market bounce biggest early in the next bull. Guess what? Tech and Tech-like stocks led 2022’s decline downward. Tech’s big bounce since—which isn’t limited to the Magnificent 7—shouldn’t surprise.

But it’s not just Tech. How to know that? Look where Tech isn’t The Magnificent 7 are US-based, part of America’s hugely and globally outsized 30% Tech weight. But tech sparse overseas markets are soaring with industrials, financials–even utilities…but almost no tech. In local currencies to avoid skew, markets hitting total return all-time highs this year include: Australia’s ASX 200, Britain’s FTSE 100, the MSCI Denmark, France’s CAC 40, Germany’s DAX, the MSCI India, Ireland’s ISEQ, Italy’s MIB, Japan’s TOPIX, Netherland’s AEX and Spain’s IBEX. All! Repeat, all! Just the Magnificent 7? Got it? Magnitudes vary, but this magnificent market, while not everywhere, is significantly global and far broader than fantasized.

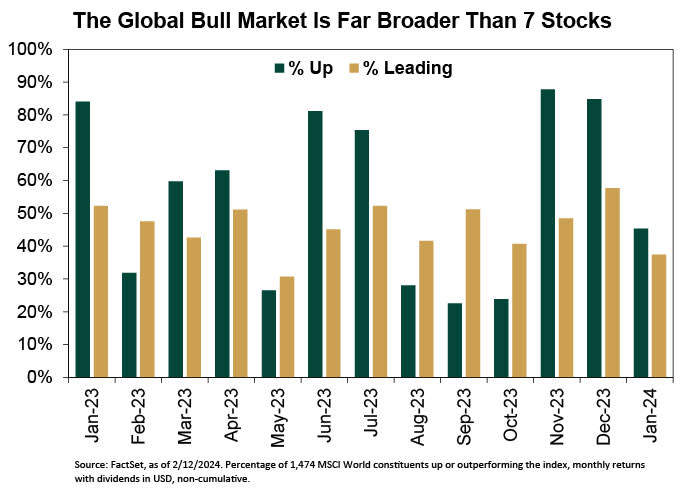

Or consider simply: In 2023, nearly 75% of the MSCI World’s more than 1,400 stocks rose. Fully 548 outperformed the World’s 23.8% return! How wiseacre pundits morph that into some seven-stock, bubble-like myth is a prime lesson in “The Pessimism of Disbelief.“

Sir John Templeton famously said, “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” Naysayers seemingly think we fast flipped from pessimism to euphoria. Remember 2000’s bubble? Or, even 2021’s slight froth? IPOs flooded the late 1990’s markets. Myriad SPAC offering dotted 2021. This is natural: Euphoria means firm founders and owners crave gorging at the IPO dessert buffet. Where are the IPOs now? Nowhere. (As I coined decades ago, IPO really means, “It’s Probably Overpriced.)

We aren’t near euphoria–which all these “Magnificent 7” doubts prove. That “It’s Just” skeptical, doubt-ish talk never flourishes in bubbles. Sure didn’t in 2000. It takes a long, long time for pessimism to warm into euphoria. We may be straddling somewhere between skepticism and optimism now.

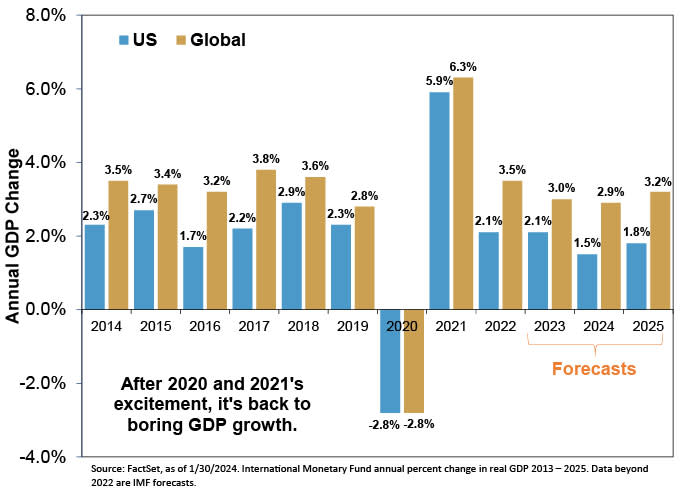

We have a massively misunderstood return of normal, pre-pandemic economic growth and inflation rates. Before 2020’s lockdown-driven collapse, America routinely grew between 1.7% and 2.9% annually. The world? Roughly 3%. Then in 2020, COVID-ized, all manner of economic data went wildly whacko, initially imploding–then, bouncing back bigtime. IMF data show American and global 2021 growth at a red-hot 5.9% and 6.3%, respectively. They then reverted in 2022 to historically normal 2.1% and 3.5%, with 2023 final estimates in midst those pre-pandemic norms. It’s just a return from a hyper fast 2021—to the old normal.

Maybe past growth rates feel scary. But the old normal was fantastic for stocks, fostering healthy sales and profits against nonstop griping that the economy wasn’t good enough. It was good enough to deliver history’s longest-ever bull market from 2009 – 2020. And is easily enough for this magnificent bull market to run now.

Ken Fisher is the founder and executive chairman of Fisher Investments, a four-time New York Times bestselling author, and regular columnist in 21 countries globally.