China Insight: Where Is China’s Consumer Market Headed?

Double Eleven, Black Friday, Double Twelve, Gift Season for Christmas and New Year — a series of intensive promotional activities at the end of the year failed to recover the past glories of the Chinese consumer market.

What mostly concerns the fashion and beauty sectors in China is consumer psychology and future trends reflected in this year-end promotion season as a turning point this year and next, rather than speculation over “a shrinking consumer market in China.”

More from WWD

Canada Goose Taps Beth Clymer as President, Finance, Strategy, Admin

Louis Vuitton Picks Shanghai to Debut 'Voyager Show' Concept

Looking at 2023’s consumption data, it seems to indicate that the downturn in the market could be about to reverse.

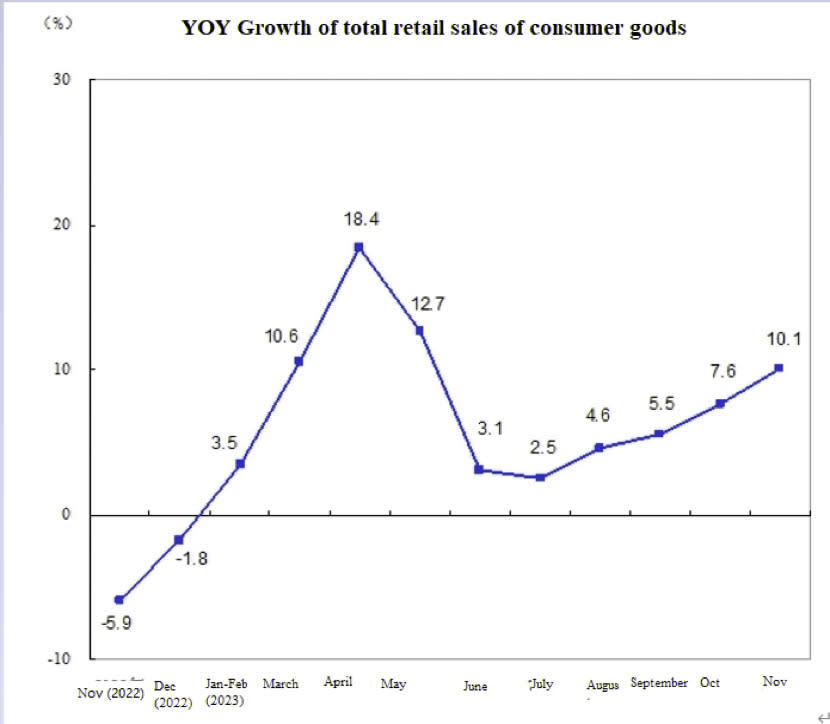

Consumer confidence showed signs of recovery earlier this year, with a promising start in the first quarter. But the good times didn’t last long, as a sudden decline occurred in the second quarter due to a slump in the property market, high volatility in the stock market, sluggish exports and many other adverse factors. Despite a struggling increase in the third quarter, consumer data confirmed the reality recognized by many industry insiders: China’s consumer market may be bidding farewell to double-digit growth.

Yet the fourth quarter saw a surprising 7.6 percent increase in total retail sales in October. According to the latest data from the National Bureau of Statistics, total retail sales of consumer goods in November saw a 10.1 percent year-on-year increase, hitting a new high in the second half of the year, with the growth rate of apparel retailing jumping 22 percent year-over-year, showing a reverse in the last quarter of the sluggish downturn that had lingered since April.

Looking at this data, what are the implications for the fashion consumer market?

In the fourth quarter, the eight-day-long national holiday saw 826 million trips, with per capita spending of only 912 renminbi ($128). During the Double 11 Shopping Festival that followed this less-than-expected “Golden Week,” sales increased only 2 percent year-over-year.

December is also a traditional shopping season in China with the Double 12 Shopping Festival featuring online and offline promotions, and Christmas and New Year’s Day gift shopping and year-end promotions throughout the country. Despite the hope for retail sales growth to surpass that of November and regain double digits, consumption, led by footwear and cosmetics, is facing headwinds in reaching higher growth.

In 2023, the Double 12 Shopping Festival, launched by Taobao 12 years ago, was initially rumored to have been “canceled,” yet made a comeback with the name of “Shop for [a] Good Price.” Still, performance was weaker than in previous years in terms of discounts and the number of participating stores and products.

Major e-commerce companies declined to release key data, such as order volume, user size, turnover and other information, which they did in 2022. More importantly, platforms and brands woke up from the “GMV craze” of previous years and had to recognize that consumer demand has returned to a more rational level.

From January to November, online retail sales amounted to 1,395.71 billion yuan ($195.8 billion), up 11 percent year-over-year. Apparel, footwear, hats, knitwear and textile categories performed the best, up 22 percent year-over-year in November and 7.5 percent in October. A series of intensive year-end promotions was launched, including JD’s support in search, venue and other public domain traffic for brands to participate in promotions; “consumption coupons” and “search free” launched by TikTok, a platform that excels at both content and inventory, and 90 percent off on more than 5,000 brands at Vipshop at record low prices for many hot items. Taobao seemed to be the exception since it had anticipated the fierce price competition at the year’s end and took the lead by offering a “year-end good price” that focused on scenarios and a high performance-price ratio to stimulate consumers’ willingness to spend.

From a strategic point of view, the combined efforts of platforms and brands have set new records in terms of the abundance of products, price indexes, and simplified rules in China’s online market. However, in terms of market performance, the “good price,” which caters to “reverse consumption” and a “decent life with budgeted spending,” and the reorganized traffic supply and guidance model have not delivered higher results. The “dark horses” that delivered impressive results were accessories, sports and outdoor, coffee and tea, and nail and eyelash services. While demand for esports, cycling, skiing and trendy games continues to increase, the market overall has entered a more rational consumption pattern. Consumers no longer spend their money on fashion status symbols, but rather on their own needs.

As a result, emotional experience and the appeal of brands are still an important attraction. When emotional value becomes the key driving force for consumption, this enables brands to capture their target customers.

Expressing love and pampering oneself is the beginning of a lifelong pursuit for Chinese consumers, who are awakening to the importance of emotional value and spiritual feedback. For brands and platforms, this is an opportunity for sales throughout the year. The “season of gifts” has emerged on various platforms such as JD and Xiaohongshu, and has been validated by the market as an effective path to open up incremental markets.

“Season of gifts” is also a golden opportunity, especially for luxury goods. For example, positioning as premium gift-giving, luxury products such as Hermès and Chanel have launched promotions on Xiaohongshu for Christmas and New Year sales, with the former showing a 40 percent year-over-year increase in brand searches in December, and the latter also showing significant search boosts in the watch and jewelry categories.

In addition to the memorable slogan of “Cherish Love, Chopard Celebrates Every Moment of Love in Your Life” by Chopard, Bulgari also is reaching its target consumers with a scale effect during the Christmas and New Year period, while Valentino is focusing on “emotional marketing.” From Chinese New Year at the beginning of the year to the Chinese Valentine’s Day, the brand has been celebrating romance and has seen strong results. Piaget also taps into the lifestyles of its target consumers with its festival promotions.

As the aspirations for love and self pampering increase, companies and brands that are favored by consumers for their values become direct beneficiaries.

According to Maslow’s Needs-Hierarchy Theory, self-actualization — such as morality and creativity — is the highest level of self-pleasing. For companies and brands that actively fulfill their social responsibilities, consumers are willing to establish a connection with them and pay a premium so as to contribute their own efforts and give back to society through consumption. Moreover, companies and brands adhering to ESG governance will have a great deal to offer in meeting consumer demands for traceability in the supply chain and the origin of raw materials in 2024.

The path to recovery is unlikely to be smooth, but the fundamentals of the market seem to be stabilizing. The consumer mood as well as platform and brand strategies present a clear picture: The fashion industry in China appears to be heading for a future where consumers lose interest in frequently arranged price wars and promotions, and change their perceptions of consumption. Therefore, only brands with values that touch the hearts of the consumers can be winners.

Editor’s Note: China Insight is a monthly column from WWD’s sister publication WWD China offering insights into that key market for fashion, accessories and beauty.

Best of WWD