100 Years of Real Estate and Homeownership, Through the Pages of BHG

Take a decade-by-decade tour through the past 100 years of buying, selling, and owning homes.

Better Homes & Gardens

If home is where the heart is, home for Better Homes & Gardens has always been, well, in the home (and the garden, of course). Home is at the heart of everything we do and everything BHG has done for the last 100 years, and while we’ve covered how to decorate your home through the last 100 years, we’ve also explored obtaining that home.

Whether through a guide on how to shop for a home, tips on saving for and purchasing your dream house, or advice on whether buying a home is right for our readers, BHG has always supported homeownership. (We’ve even been part of the home buying experience through the Better Homes and Gardens Real Estate division since 1978.)

Homeownership rates have increased in the United States over the last 100 years, rising from a national rate of nearly 46% in 1920 to more than 65% in 2022, with some dips and peaks in the intervening years. The comfort and convenience—and, later, opportunity for building wealth—of owning your own home has long been emphasized, even becoming what Chris Masiello, chairman and CEO of Better Homes and Gardens Real Estate - The Masiello Group, calls a “fundamental underpinning” to how communities across the country function.

The goal of owning a home has persisted for many Americans through economic downturn, global wars, shifting priorities, financial challenges, and more, and even when access to that ownership was—and continues to be—offered unequally. While national homeownership rates have risen since 1922, the increase in ownership among White households has increased much more than it has for Black households and those of other racially marginalized groups. And, of course, what we want from our homes in terms of style, size, and even function has shifted drastically over the years.

To mark the 100th anniversary of Better Homes & Gardens, we’re exploring what home buying and owning has looked like in the United States since 1922—plus how our homes have changed over the last century. Read on for a decade-by-decade breakdown of homes, homeownership, and the circumstances that impacted both through the pages of Better Homes & Gardens.

Better Homes & Gardens

1920s: Building a Place to Live

The 1920s were a period of economic prosperity for the U.S. Homeownership rates were on the rise: Nearly 46% of households owned their home at the start of the decade, and that rate climbed to almost 48% by 1930, according to Census data.

While specific information about the housing market at this time is hard to come by, in 1922, the year Better Homes & Gardens launched as Fruit, Garden and Home, the median asking price for an existing house in Washington, D.C., (where the Census Bureau was based, making this a very subjective number) was around $7,200. Estimates for home size during this decade are around 1,000 square feet for a single-family home.

DIY Homeownership

The goal of owning your own home was supported by BHG from the start. The magazine published an article in January 1924 titled “It’s a Valiant Thing to Own Your Home,” and stories throughout the decade shared tips and tricks for achieving that goal of homeownership. BHG suggested setting aside money for a down payment through careful saving and cost-cutting measures, but our pages also recommended another path to homeownership: building your house yourself.

In August 1923, we published an article titled “Building a Home For a Thousand Dollars: Economical Construction Is Possible Even In This Era Of High Prices” with a guide to building a two-bedroom, two-bathroom home. The concept of building your own home appeared in other issues throughout the ’20s, all helping eager readers to become homeowners, even if they had to do it piecemeal: The September 1925 issue introduced the concept of building a small home, then expanding as needed over four building stages until readers had a home that suited them. Another suggested path to homeownership was to save up enough money to buy a lot, then to continue saving until you had enough money to build on that lot.

What Makes a Home?

Homes were much smaller in the ’20s than they are today, but expectations for which rooms were necessary remain much the same.

“There are certain rooms every family must have. For gracious and pleasant living, we need a living-room, dining-room, hall and kitchen. There must be stairways and closets and a fireplace,” architect Leland A. McBroom wrote in the July 1927 issue of BHG, also mentioning the need for bedrooms and even a designated guest room.

The house described by McBroom would have been larger than the average home and within reach for only wealthier households, but it gives you a sense of what rooms were included in many homes: a living room, a dining room, a kitchen, and bedrooms and bathrooms. While most new homes would have at least one bathroom—indoor plumbing was introduced in the U.S. in the mid-nineteenth century, several decades earlier—multiple bathrooms in one home were less common, and many of the homes depicted in the early pages of BHG featured just one full bathroom.

Houses as Expenses, Not Investments

The goal of owning a home was widely shared and essentially a given in certain socioeconomic groups, and especially among readers of BHG, but the value of that home beyond being a place to live was much less certain. The standard home in the ’20s was not an investment: It was a necessary expense in exchange for housing.

In September 1926, BHG published a letter from a reader sharing tips on practicing thriftiness at home. “When you build a house, depreciation, in the strict sense starts the day its use begins,” reader D. V. H. of Nebraska wrote. “Assuming that the value of the lot and the value of new lumber remains the same, the house will be of less value a year later than when brand new.”

In other words, the assumption that home values consistently increase over time—the concept behind the widely held belief that a house is a financial investment as much as it is a place to live—was yet to be part of the fabric of American life.

At the end of the decade, the stock market crash of 1929 plunged the U.S. into the Great Depression, with enormous—and eventually, lasting—impacts on homeownership.

Better Homes & Gardens

1930s: A More Modest Approach to the Home

The 1930s were defined by economic hardship. The Great Depression lasted until 1939, with financial impacts on all areas of life—especially housing and homeownership. At the start of the decade, coming off the success of the ’20s, the national homeownership rate had risen to almost 48%. By the 1940 Census, that rate had fallen below 44%.

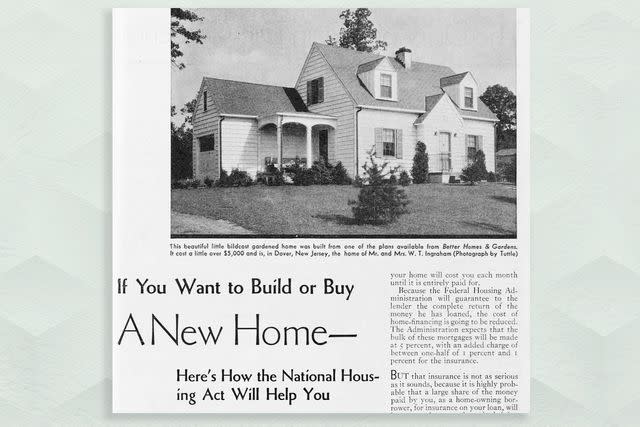

The challenges posed by the Great Depression led to substantial federal intervention to pull the country out of its financial downturn. Significantly for the housing market, the Federal Housing Administration (FHA) was established through the Housing Act of 1934, a key piece of President Franklin Delano Roosevelt’s New Deal legislation.

The FHA was intended to help boost the home building and finance industries, both of which suffered during the Great Depression, and provide housing for White middle- and lower-middle-class families. Together, these efforts increased the country’s housing stock—and made sure the newly built homes went mainly to White families through a number of discriminatory practices that continue in various forms today. The discriminatory legacy of these institutions would have lasting effects on homeownership rates among racially marginalized groups throughout the following decades—and those effects continue to be felt today.

While efforts to turn the housing market around eventually succeeded, the ’30s were still a period of economic restraint. Still, the pages of BHG reflect a persistent trend toward homeownership, even if economic conditions delayed the reality of owning a home for many families.

Better Homes & Gardens

Owning a Home with Care

BHG reflected a modest approach to the home during this time. Many articles focused on affordability and attainability, and one May 1937 article even argued that a small bathroom was even better than a larger one.

The pages of BHG also had a new focus on home improvement during this era, an approach that would eventually define the publication. In a September 1931 article titled “Keep Your Home Young,” we offered repair and remodeling tips, which included updating exterior siding—some things never change—to give smaller homes “an impression of breadth.”

“After all, $5,000 or $10,000 or $15,000 is a big investment—the biggest most of us ever make—and you want to know pretty thoroly [sic] what you’re getting in return.”

The article also addressed concerns about home values with a new optimism, encouraging readers to keep their homes “young” to maintain their value once market conditions improved: “You want to … keep your home young. Then, too, property values have gone down, temporarily at least. There isn’t a chance to sell without taking a loss. And when values rise again the house will be that much more behind the times.”

Beyond thrift and a new emphasis on repairing and even upgrading the home, there was an emphasis on choosing your home carefully. Articles throughout the ’30s encouraged checking all the details and separating needs from wants during the home search, putting needs first and avoiding putting too much emphasis on wants.

“Will you and your family take pride and pleasure in living on that spot now and for years to come?” one article asked.

However we put it, approaches to home ownership in the ’30s were cautious and intentional: “After all, $5,000 or $10,000 or $15,000 is a big investment—the biggest most of us ever make—and you want to know pretty thoroly [sic] what you’re getting in return,” we wrote in 1939.

By 1939, the U.S. housing market was settling into a new normal—and then World War II began.

Better Homes & Gardens

1940s: The Homeownership Boom

1940 Census data shows that less than 44% of Americans owned their homes at the start of the decade. By the end, that number had skyrocketed to 55%—a home-owning majority for the first time. As homeownership rates climbed, so did home prices: Census median asking price figures for Washington, D.C., went from around $6,500 in 1940 to $12,300 in 1947 (when the Census Bureau stopped tracking this figure). Other Census data says the median home value for the country was a little more than $2,900 in 1940, or $30,600 in 2000 dollars, when adjusted for inflation.

The first half of the decade was defined by World War II, which the U.S. formally entered in 1941. The early ’40s were almost entirely dedicated to the war effort. A January 1944 article in BHG titled “Build Your New Home Now” encouraged readers to wait and prepare for their post-war future: “While you’re waiting and planning for the postwar home that your War Savings Bonds are going to help you pay for, why not build a model of it and see it in miniature?”

After World War II ended in 1945, though, everything changed.

“If you take a look at the more formative years of housing, it really started post-Second World War with the baby boom,” Masiello says.

The baby boom was the enormous increase in the U.S. birth rate after World War II, as deployed military personnel returned home to rejoin or start their families. Some 75 million people were born during the baby boom, which stretched from 1946 to 1964, and all those growing families needed places to live. With the help of ongoing FHA efforts and special mortgages offered to returning members of the military, many bought homes, and home construction skyrocketed to meet this new demand. (As in other programs, these offerings were often discriminatory and mainly made available to White members of the military.)

According to Census data, construction began on 530,000 new housing units in 1940. Construction slowed during the wartime years, but by 1949, the number of housing starts had risen to 1.5 million new units.

The Home of the 1940s

While these ready-built or builder houses were convenient, there was some skepticism of these developments—and concern that they lacked character. In a June 1949 article titled “Ready-built house + your personality = The home you want,” BHG offered tips on making a new house a home. “You can’t buy a ready-made builder’s house and expect it to look like a lived-in house—to look like you and your family,” we wrote.

Otherwise, the layout and makeup of the standard home was becoming more similar to the homes we see today. BHG first wrote about “family hobby rooms”—the family room we know today—in 1944, and a May 1946 article broke down options for types and arrangement of rooms, alluding to an increasing interest in more personalized, functional layouts. The necessity of a basement was questioned, because “construction and heating improvements have eliminated the need for basements, so you have an actual choice today.” We discussed whether formal dining rooms were necessary, or if “an alcove at one end of the living room [would] serve as well.” The desire for more than one or two bathrooms was also addressed, with a caveat: “A bathroom for every bedroom is ideal, but too expensive for most of us.”

“There’s a deep, day-to-day satisfaction in escaping from the tight, mean little rooms so commonplace in yesterday’s small house.”

Finally, even laundry rooms evolved during this period. “Laundries no longer need be dark, steamy cubbyholes,” we wrote. “Modern equipment makes laundries as smart and attractive as kitchens. … You can have a compact laundry in connection with the kitchen, or in a separate utility room.”

You could even say the ’40s marked the beginning of the open floor plan. A July 1947 article titled “Open Planning Makes a Small Home Seem Larger” reads: “Advances in the science of building have made it possible to do away with many interior partitions. Even in low-cost homes, they’re not needed to hold up the roof. That means we can judge partitions in terms of what they do. We can use them where privacy is important, eliminate them in related living areas. This emancipation has brought a new concept to home architecture—open planning. It has many advantages, but the greatest in a small home is the feeling of spaciousness. There’s a deep, day-to-day satisfaction in escaping from the tight, mean little rooms so commonplace in yesterday’s small house.”

Achieving Homeownership

Even with all the new construction, not everyone had the means or access to buy a new home. BHG offered up the now-common concept of buying an older home and remodeling it in our February 1949 article, “Remodeling: The Best Way to Get a Home?”

“There is no sign that building costs are going to drop much in the near future,” we wrote. “But that needn’t stop you from having a home of your own. One good way is to buy an old building and remodel it. Not any old building, though—it must be structurally sound and capable of being renovated. Chances are that you will end up with as good a home at less cost than if you bought a house or built a new one. When you want to sell, you will probably be as well off financially, too.”

While national homeownership rates were climbing and the housing stock was improving, the reality of this era was that the full range of housing options weren’t truly available to everyone. The FHA and other initiatives helped a larger share of working and middle-class people become homeowners, eventually leading to the establishment of a property-owning majority in the U.S.—but that majority was mostly White. The rate for homeownership among White families was 45.6% in 1940, while the rate for Black homeowners was only 22.8%, and the rate for Asian households was 16.3%. (Data on the homeownership rate among Hispanic/Latino communities became available starting in 1970.)

The FHA and affiliated institutions made use of practices now known as redlining that effectively sought to prevent Black families and families of other racially marginalized groups from accessing the same home-buying opportunities White families enjoyed. Through various financial incentives, the FHA—and the mortgage lenders, financial institutions, and homebuilders who received support or funding from the FHA, as well as private institutions who copied the FHA’s policies—effectively prevented many families (mainly Black ones) from moving into the new homes and developments being built because of their race or ethnicity.

This practice—with societal and cultural enforcement by communities through acts of violence and harassment, among other strategies—effectively segregated many regions, ensuring new and improving communities mostly consisted of White families, while racially marginalized groups struggled to purchase homes outside less desirable areas with fewer resources.

Just as the housing and baby booms had lasting impacts on the U.S. housing market, so too would the legacy of these discriminatory practices, which established redlining as an ongoing practice and led to the creation of racially segregated communities and towns, many of which have maintained the same resident demographics that they had in the 1940s.

Better Homes & Gardens

1950s: Trading Up

By the 1950 census, due in huge part to various governmental home-buying initiatives, the homeownership rate was at 55%—a home-owning majority. That rate would continue to climb throughout the decade, and the high rate of construction seen in the ’40s continued, too. By 1950, the median home value in the U.S. had risen to more than $7,300, or $44,600 when adjusted for inflation.

The 1940s were a period of enormous shifts in housebuilding and buying. Comparatively, the ’50s were a period of continuation, rather than extreme change. The Housing Act of 1954 was passed in this decade, providing funding to improve deteriorating areas and increase public housing units. This marked a shift in federal emphasis from new construction to conservation and housing rehabilitation, a reprioritization that continues today.

Better Homes & Gardens

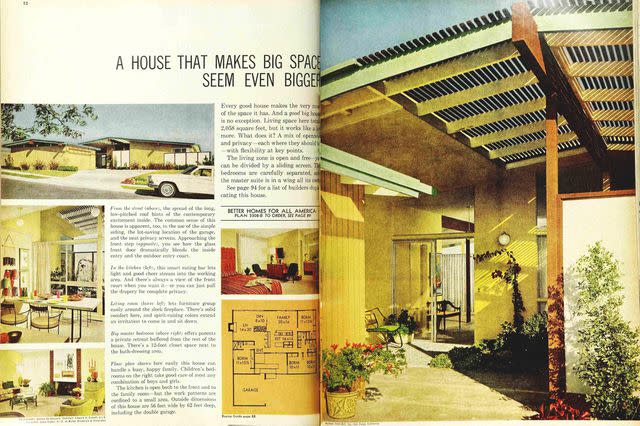

The Mid-Century House

In the pages of BHG, there was a strong focus on building your own house, mainly as a more affordable path to homeownership. (One article even recommended converting garages into living space to get more house for less.) A new house layout was introduced in this decade: In July 1955, BHG wrote about “a new way to build a two-story house.” Today, we know this layout as the bi-level or split-foyer home.

The ’50s also introduced a new concept in home-buying—trading in.

In a 1954 article titled “We Traded in Our Old Home on a New Model,” BHG wrote, “If the newest idea in real estate catches on—as it promises to—your friends and neighbors may be trading a small house for a larger one, or an old house for a new one, as casually as they now trade their old cars for the latest models.”

A home trade-in was when a homeowner agreed to sell their home to a real estate agent or home builder (the common options in the ’50s) at a fair market value. This guaranteed a sale for the homeowner, saved them the hassle of repairing, preparing, and showing their home, and gave them the money necessary to buy a new home with minimal delay. Often, trade-in agreements at this time included the stipulation that the buyer purchase their new home through or from the person purchasing their old home.

“If the newest idea in real estate catches on—as it promises to—your friends and neighbors may be trading a small house for a larger one, or an old house for a new one, as casually as they now trade their old cars for the latest models.”

The idea of trading in or up-sizing your home marked a new approach to homebuying (even if the actual logistics of that process have changed as trade-ins grew less popular). Whereas before a family may have expected to live in their home for their entire lives—and even intended to pass the house down from generation to generation—the idea that you would live in your home only until it felt too small or too old or you could afford a new one made owning a particular home a shorter commitment.

The precursor to the concept of the starter home, moving up—selling a smaller, older home in order to buy a bigger, nicer one once you had enough money saved up—would become a defining characteristic of the U.S. housing market. “You trade in your old car on a new one; why can’t you trade in your old home on a new house—or one better suited to your present needs? You can do that now,” BHG wrote in the ’50s.

The relative consistency of this decade in the housing market served as a backdrop to social change: The U.S. civil rights movement began in 1954 as Black Americans protested institutional segregation, discrimination, and disenfranchisement throughout the country. The Black homeownership rate in 1950 was 34.5%, while the rate for White families was 57%. (The rate of Asian homeownership had climbed from 16.3% in 1940 to 30.3% in 1950.) Together, these factors set the stage for shifts in accessibility, housing preference, and more for homeowners and aspiring buyers alike in the following decade.

Better Homes & Gardens

1960s: A More Modern Home Market

Homeownership continued to climb in the ’60s, albeit more slowly than during the ’40s and ’50s. The homeownership rate was just a touch below 62%, per the 1960 census, and it hit 64% in 1969. Average home sale price in 1963 was $19,300, and that figure had climbed to $27,100 in 1969.

Homeownership was a key theme for BHG throughout the ’60s: “Buy or sell, 1963 is the big year for home owning—even bigger than last year, when about 1.4 million new homes were started, and many times that were sold,” we wrote in the early part of the decade.

More Equal Access to Homeownership

Homeownership for Black, White, and Asian communities increased throughout the events of the ’60s. The Black homeownership rate had climbed to 38% by 1960, while the rate for White households was 65%, and the rate for Asian households was 44.1%. Because of redlining and other segregational practices, Black households (and other racially marginalized groups) still did not have the same access to homeownership, though. Home and neighborhood values were unequal, too, with homes in predominantly White neighborhoods increasing in value at higher rates than those in other neighborhoods, contributing to unequal accumulation of wealth.

Enter the Fair Housing Act: Passed in 1968, the Fair Housing Act protects people from discrimination on the basis of race, color, national origin, religion, and a number of other characteristics while they are renting or buying a home, applying for a mortgage, seeking housing assistance, or engaging in other housing-related activities. The Fair Housing Act was intended to address redlining and other discriminatory practices, and homeownership rates among communities of color continued to increase after its passage, despite the persistence of discriminatory housing practices, some of which also continue today.

Better Homes & Gardens

Getting a Better Home

The concept of moving—or remodeling—to get a home that better suited one’s family also flourished in the ’60s. Settling for a just-OK home was a thing of the past, and in 1961, we wrote, “Better Homes & Gardens believes your family’s consideration on remodeling should be whether your needs would be better satisfied by moving into a new home or expanding your present one.”

For homeowners new and old, the desire for more modern spaces continued. BHG guides to making the most of your space or better organizing a home to make it more functional abounded, particularly in the first half of the decade.

People still wanted more bathroom space, too: “How often do you wish for the convenience of an extra bathroom in your home?” we wrote in 1969. “Every morning? You aren’t alone. Many people, especially those owning older homes, are faced with the problem of sharing a single upstairs bathroom with the whole family.”

Trading in your home remained a popular option in the ’60s, giving current homeowners another way of obtaining a better-for-them house. “The point of a trade-in is to make a quick, sure sale when you don’t want to be paying for the new house while you’re still paying for the old one,” we said of the process in 1964.

“A Sound Financial Reason”

The concept of homeownership flourished throughout this decade, even if the financial benefits of buying a home fluctuated.

“Home ownership offers you many benefits—the right to live where you want as long as you want; full freedom to furnish and decorate and landscape; the satisfaction of raising your children in a place they can genuinely call home,” we wrote in a January 1964 article. “But beyond these intangibles is a sound financial reason for home ownership.”

“In today’s Alice-in-Wonderland housing market, no one knows exactly what a house will be worth five or ten years from now.”

By the end of the decade, that “sound financial reason” wasn’t so certain. The Recession of 1969-1970 led to a short-term drop in the homeownership rate, and home prices stayed roughly the same during that short economic downturn.

A September 1969 article titled “Is a Home Still a Good Investment” addressed increasing financial concerns surrounding homeownership: “In today’s Alice-in-Wonderland housing market, no one knows exactly what a house will be worth five or ten years from now.” Later in the same article, we wrote, “Unfortunately, the solid investment value of a home is seriously threatened today.”

That financial uncertainty continued into the ’70s, a period of relative stagnation for the housing market.

1970s: The Home as an Investment

Economically speaking, the 1970s were defined by two recessions: the Recession of 1969-1970 and the 1973-1975 recession. Together, these events meant that—though there were short-term spikes—the national homeownership rate hovered around 64% for the majority of the decade, ending at a little above 65% in 1979.

The Fair Housing Act was in place by the end of the prior decade; homeownership among Black households continued to climb, but slowly: from 38% in 1960 to a little less than 43% in 1970. The Black homeownership rate remained the lowest of any group. White homeownership was at 66.8% in 1970, Asian homeownership was at 48.9%, and the Hispanic/Latino homeownership rate was 43.8%.

Home values did not experience the same stagnation, and the average home sale price rose from $27,000 to $72,700 by the end of the ’70s.

Better Homes & Gardens

More Than Just a Place to Live

The huge increase in home value and sale prices meant that the home became an investment as much as it was a place to live. Current homeowners in highly prized areas were able to benefit from their home values increasing, while aspiring ones were told to act fast: “If you’re renting now but dream of someday buying your own house, the sooner you can manage it, the better off you’ll be,” we advised in a 1977 article.

Ultimately, the new, much higher cost of purchasing and maintaining a home was a serious concern throughout the ’70s.

“The cost of buying a new home has more than doubled in the past eight years,” said a 1979 BHG article. “Home prices went up 142 percent between 1970 and 1978, rising from a median of $23,000 to $56,000. And 1979 prices are even higher. That’s bad enough, but there’s more. The cost of owning and operating a home has gone up almost as fast as the cost of buying. Between 1970 and 1978, the median cost of maintaining a home soared 135 percent from $998 annually to a startling new high of $2,454 per year.”

Later in the article, we wrote, “The old rules of thumb for knowing when you can afford a new home are obsolete.”

With all that in mind, maintaining your investment in your home became a key theme in the pages of BHG.

Better Homes & Gardens

“For homeowning families, the conclusions are clear: Keep your house in good condition and it will probably grow in value more rapidly than any other investment you could make,” a March 1977 article read. “Trading up to a better house is also a financially sound move if you’re careful not to bite off more expense than you can chew.”

In an April 1977 article, we highlighted the home improvements that might offer the best return—and attract potential buyers: A new kitchen, a new or remodeled bathroom, additional bedrooms, and a new family room all made the list.

Even as costs increased, though, people still wanted more from their homes. By 1979, only 26% of new homes had 1½ baths or less. The general attitude toward all homes—new and remodeled—was to make them bigger and better.

“When houses were built in the ’30s and ’40s and ’50s, you had one bathroom,” Masiello says of this period. “Well, that doesn’t cut it anymore.”

Even those looking for a “no frills” house at a lower cost did so with the idea that they could fix it up or add on to it later: No one wanted to settle for a less-than perfect home, and many still wanted to be homeowners, even as prices continued to climb going into the following decade.

1980s: Bigger Homes, Fewer Buyers

After the incredible increase in home value seen in the ’70s, growth in the ’80s was much slower—but average sale price still continued to climb, going from $73,600 in 1980 to $151,200 by the end of 1989.

Homes were getting bigger, too. During the ’80s, the number of newly constructed homes of less than 1,200 square feet shrunk, and the number of homes that were 2,000 square feet or larger increased. The median single-family home at the time was around 1,600 square feet.

Rising home prices, plus the recessions of 1980 and 1981-1982, led to a sustained decline in the national homeownership rate for the first time since the Great Depression. More than 65% of households owned their homes in 1980: In 1989, that national number dipped below 64%. That decline primarily hit non-White homeowners. White homeownership actually increased between 1980 and 1990, while rates among Asian, Black, and Hispanic/Latino households all declined.

Making the Most of a Tough Market

In the pages of BHG, we continued to emphasize the achievability of buying a home, even if aspiring buyers had to get creative in how they did it. Even challenging economic circumstances couldn’t touch goals of homeownership: “The American Dream is alive and well—and changing,” we wrote in 1986. “Nothing new about the desire: Owning your own home is a goal that’s never wavered. It’s the house itself that’s being modified.”

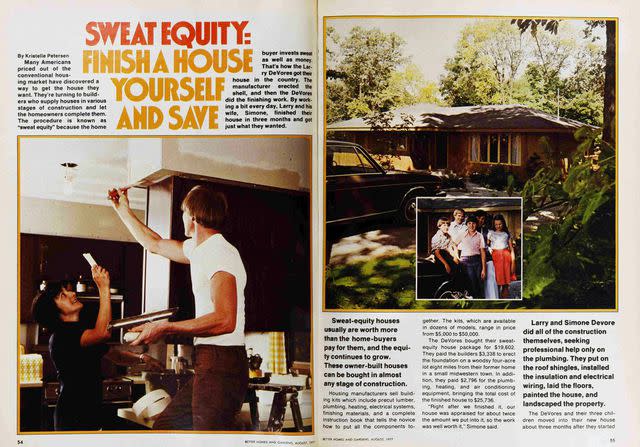

To help readers toward that goal, BHG discussed strategies for buying a less expensive home outside urban or suburban areas, tackling fixer-uppers and building “sweat equity,” buying a larger home and renting out part of it to help pay the mortgage, and even taking advantage of shared-equity mortgages, where well-off parents could help their adult children purchase their first home. We even returned to owner/builder approaches to homeownership that were popular in the ’20s and ’30s, offering guides to building your own home.

Better Homes & Gardens

Bigger Is Better

However one obtained their home, what those homes looked like was changing. Home spaces were becoming more casual and open, and through-views, high ceilings, and open concept floor plans were all considered essentials in a well-equipped home. These changes reflected a shift—one we still see today—in priority.

“There’s a big difference when people are choosing between wants and needs, right?” Masiello says. “A want is aspirational, and a need is more functional.” The new prioritization of wants, above and beyond needs, in home buying was a key contributor to the increasing size and luxuriousness of homes in the U.S.

“Most of today’s buyers have specific needs and wants in mind when they consider their dream home. Most don’t move until they find a house that says, ‘This is the real me.’”

In the ’80s, homeowners wanted more space—and less shared space—to support their busy lives and hobbies. 16% of homes built in 1989 had three or more bathrooms, a new high, and only 14% of homes had only one full bathroom.

The primary suite, consisting of closet space and a bathroom connected to the primary bedroom in the home, quickly became a top desire during this decade. “Couples who regularly get up together and get dressed to go to work need a place that fits both of them comfortably,” a 1989 article claimed. “And they really require a spacious [primary] bedroom suite to enjoy their health and fitness routines, as well.”

Expectations were high: “Most of today’s buyers have specific needs and wants in mind when they consider their dream home. Most don’t move until they find a house that says, ‘This is the real me.’ It has to have most of the things they want right when they buy it. And they’re willing to spend a little more on quality,” we wrote in 1989.

Altogether, despite falling homeownership rates and climbing prices, the real estate landscape of the ’80s set the stage for the market of the ’90s—the early version of the housing world we know today.

Susan Gilmore

1990s: Going Up and Up

After the stagnation and decline—and steep increase in the cost of buying a home—of the ’70s and ’80s, the ’90s were a period of growth, particularly in the second half of the decade. The national homeownership rate had climbed to nearly 67% by 1999, and that prosperity was distributed: Homeownership rates across all groups increased during this decade.

Home prices also continued to rise, strengthening the attitudes regarding homeownership as an investment that seemed so in doubt in the ’60s: Average home sale price in the U.S. surpassed $200,000 in 1999.

The desire to own a home remained omnipresent among BHG readers, despite high costs. “It turns out that, by a 3-1 margin, folks would rather own their own homes than retire 10 years early,” our then–Editor in Chief, David Jordan, wrote in his September 1992 letter from the editor. “By a 4-1 margin, they’d rather own a home than take a better job in a city where they could afford only to rent. And, two out of three would take a second job to own a home.”

The home-buying conditions of the time were beginning to reflect the landscape we see today.

“Owning a home is the dream of most families,” Jordan’s letter continued. “Of course, times have been tough for aspiring homeowners. It’s hard and harder for young folks to save up for a down payment. This creates a domino effect, making it harder for families who want to move up to bigger houses to sell their existing homes.”

Something New

Increased home prices notwithstanding, smaller houses—often considered starter homes for households who expected to eventually upsize into something larger, often to fit a growing family—were not as readily available as larger ones, particularly if you wanted a newer home. New homes just kept getting bigger: More than half of new houses built during this period had three bedrooms, and by the end of the decade, a third had four bedrooms or more.

More space wasn’t the only draw of new homes. People also craved the comfort and convenience—and updated styles. “New houses mirror today’s lifestyles,” an April 1997 article in BHG reads. “Families live differently than they did just 15 or 20 years ago. Cooking is a group experience, and no one wants to be too far from the television. New homes blend the kitchen, eating area, and family room into one informal space. New houses also have more and larger bathrooms and closets.”

New, better homes, high prices, and a two-fold national desire to own a home—for the stability and the investment opportunity—took the world of real estate into the new millennium, where new risks awaited.

Better Homes & Gardens

2000s: Highs and Lows

In the early 2000s, it seemed like things had never been better for the housing market. The homeownership rate hit an all-time high of 69.2% in 2004, and all groups seemed to be benefiting from increased access to mortgage money—and increasingly common use of adjustable-rate mortgages (also called variable-rate mortgages), which became available nationwide in the early ’80s.

The average home sale price peaked in 2007 at $322,100, and homes were bigger and better than ever as the median size inched closer to 1,800 square feet. Zillow, a digital property listing site that has helped to remake how we home-hunt, was founded in 2006, and buying a home started to become easier, logistically speaking, than ever.

That didn’t mean everyone was looking for a new home: “We know you’d rather stay in the house you love than move when your family grows and your needs change,” said a November 2005 BHG article. Many households were trying to improve the homes they already had, efforts supported by BHG.

“With the stock market in the doldrums, many people are looking for a more stable home for their money,” we wrote in 2003, in an article on the home improvement projects that would give homeowners the highest return for their money. “And some are finding that the best place to invest is in their home itself.”

The Great Recession

By 2007, our pages hinted at a decrease in home buying interest. “There are too many new homes for sale and not enough families to buy them—a dramatic turnabout from just a couple of years ago,” a June article claimed.

Still, data pointed toward a still-growing housing market—until the Great Recession changed everything. The Great Recession officially began at the end of 2007, lasted for the entirety of 2008, and ended mid-2009. Home sale prices plunged from an average of more than $305,000 to a low in 2009 of $257,000. More striking was the decline in homeownership, as many houses were foreclosed on. Families across the United States lost their homes—and the equity they’d invested into them.

The national homeownership rate dropped to 67.3% in 2009, close to where it had been at the beginning of the decade. More impactfully, that rate would continue to decline into the 2010s, setting the stage for new housing crises in the second decade of the millennium.

Better Homes & Gardens

2010s: Adapting to a New Market

While the Great Recession officially ended in 2009, it kicked off an overall decline in homeownership rates that would last until 2016, where the national rate hit a low of 62.9%—the lowest rate of homeownership seen since 1965. At the same time, outside a brief decline during the Great Recession, average sale prices continued to climb in the 2010s, hitting pre-recession numbers in 2013 and reaching more than $380,000 by the end of the decade.

The Great Recession shook long-held beliefs that buying was nearly always better than renting. For decades, BHG reflected the cultural assumption that buying a home was a goal for most people. The articles we published in the 2010s held a new uncertainty: “If you feel settled locationwise and financially, buying can be a smart move. A home is a potential built-in savings account,” a June 2018 article said. “That said,” we wrote later in the article, “buying isn’t the best choice for everyone who’s able.” An expert quoted in the story even advised against buying just for the sake of buying.

The home improvement guidance in our pages during this era held a new focus on upgrading and adapting rental homes, and we shared tips for making properties that may have been purchased as starter homes into forever homes, in case the dream of trading up for a larger home was no longer within reach for our readers.

Unequal Impacts

Homeowners and aspiring home buyers of all groups were shaken by the Great Recession, but some groups were more impacted than others. Homeownership rates for White and Black households declined from 2000 to 2010 (rates for Asian and Hispanic/Latino families actually increased during this time), and homeownership among all groups declined between 2010 and 2015. By 2019, though, rates had started to climb again. The national rate passed 65% in late 2019, and rates among White, Asian, and Hispanic/Latino households were on the rise again.

Black households were left out of this rebound. Black homeownership peaked at a little less than 50% in 2004 and has fallen below that number ever since, even hitting a low of 40.6% in 2019 before rising slightly again. With a sustained decline since 2000, Black homeownership is the lowest it’s been since the ’70s, when the Fair Housing Act had only just been passed.

“’08 was a huge setback for Black family homeownership,” says Debra Gore-Mann, president and CEO of The Greenlining Institute, an organization that advocates for inclusive and equitable housing policies.

The financial collapse, paired with the relative recency of increased homeownership rates among Black communities, has meant that Black homeownership rates have not been able to recover as well as those of other groups have, she says. With Black families targeted with subprime mortgages—thus particularly affected by the Great Recession—the foreclosures and loss of equity during and after the recession scared many Black people off the market, Gore-Mann says.

For this heavily impacted community, homeownership carries a risk that it didn’t before: “The idea of buying a house has just become so hard, a hard choice to make,” Gore-Mann says.

Just as homeownership rates seemed to be normalizing after the Great Recession, the tumult of 2020 turned everything on its head, yet again.

Nathan Kirkman

2020s: A Hot Housing Market and Beyond

We may only be two years into this new decade, but these two years have carved out their own legacy in the history of U.S. real estate. The onset of the COVID-19 pandemic in 2020 sent everyone into quarantine and isolation—and those who could scrambled to sit out the health crisis from the comfort of their own homes. Even after social distancing restrictions eased, the rush to purchase a home continued.

The national homeownership rate spiked from 65.3% at the start of 2020 to 67.9% by mid-year. The rate normalized to around 65% quickly, but the hurry to buy homes was clear: bidding wars, all-cash offers, hours-long stretches on the market, buyers making offers without ever having seen the house in person, little to no price negotiation, and other unusual features defined the market of 2020, 2021, and much of 2022.

Fortunately, no one expects that fire-hot market—during which many families were able to purchase new (and even their first) homes, yes, but many were also unable to compete—to persist. At the end of 2022, the market is already cooling off.

“This is not normal,” says Geoff Green of the Better Homes & Gardens Real Estate Green Team. “This is going away. This is not how it’s going to be. This is not how real estate markets are, ever. That was the unicorn type of situation.”

David Greer

Technology and Real Estate

The refrain that technology is the future holds true for real estate—though technology in this context can perpetuate problems as much as it solves them.

Americans are more likely to own a home in 2022 than they were ten years before, but the homeownership rate for Black Americans specifically is still lower than it was in 2010, and the National Association of Realtors (NAR) Research Group says Black homeowners are the group most likely to be affected by declines in homeownership rate before, during, and after the 2008 Great Recession. Homeownership rates for White Americans have hovered around 70% since 2017, while rates for Black Americans have been just more than 40%. Black Americans remain the group with the lowest homeownership rates: The rates for Hispanic Americans and Asian Americans have been above 47% and 59%, respectively, since 2017.

“It's lingering from ’08, but it’s actually been compounded by more things that we’ve seen,” Gore-Mann says. “You need a lot of things to be stable to buy a house.”

Outside affordability and financing efforts, initiatives to address modern forms of redlining may help close the home ownership gap. According to NAR’s “2022 Snapshot of Race and Homebuying in America” report, the most common form of discrimination in real estate transactions today is the steering of potential home buyers toward or away from certain neighborhoods. While that is a physical type of discrimination, there are also technological types.

The technology that has changed the way we shop for a home and even apply for a mortgage has made the whole home-buying process easier—but also opened the door to a new form of redlining called digital redlining or data redlining, where data on race, age, ethnicity, and more is used by algorithms to market certain products (including property listings and mortgage offerings) to specific people. The collected data can reflect systemic biases, the Greenlining Institute says, while the algorithms that process that data may perpetuate any biases held by their creators.

“The artifacts of the way we did housing physically [informs] the data used to do it digitally,” Gore-Mann says. “So [the data we use today] is based on data that was originally segregational and redlined.”

Think data organized by zip code, utility bill data, proximity to schools, and other information that might determine what kind of home you’d want or could afford today—and also may be informed by historical redlining practices.

The Greenlining Institute and other organizations are working to establish rules and guidelines regarding how our data is used to help fight this digital discrimination.

“You have more information at your fingertips,” Gore-Mann says. “We just need to have an awareness of how it is being captured and how it is being presented to us, so then we can use the tool in a way that is helpful. The key to everything is transparency.”

Beyond its implications for equity in homeownership, technology has also contributed to the increased expectations buyers have for their homes.

“People have so much information at their fingertips now, and they see how nice certain places are, and they want that for themselves, rightfully so,” Green says. “They’re a little bit more discerning.”

Still, while it’s changed parts of the house hunt, technology won’t replace the home tour or open house—and the trend of buyers purchasing homes based on a virtual tour and photos (sight-unseen outside of digital viewings) won’t continue.

“People will prefer to look at their home before they buy it,” Green says. “As we settle in to a more normalized marketplace, that will be the way people buy homes again. I don’t think that’s going away.”

Thayer Gowdy

The Homes We Want and Live in Today

Looking forward, it’s easy to see looming shifts in the homes we want and buy. Even before the chaos of the 2020 and 2021 market, BHG predicted a new approach to the starter home in our March 2020 issue. (Our printing schedule means these predictions would have been written well before the coronavirus reached the U.S. and the market took off.)

We said that the typical starter home buyer would be searching for higher-end homes with the benefits more often associated with second or even third homes, such as more space and better schools. This upgraded list of wants, we said, would put those looking to buy their first home in competition with move-up buyers (those looking to buy a new home as an upgrade from their starter home). At the same time, empty nesters or those looking to downsize would be searching for starter homes that they could retire or age in place in.

While we couldn’t have predicted the pandemic-induced housing market, we were right that buyers have higher expectations for their starter homes.

“What’s considered a starter home now is what we considered a forever home, for many of us,” Green says. “It’s a function of how much money people have.”

That housing cycle, from starter home to move-up home to downsized home, has persisted, almost despite shifting expectations for what those homes look like.

“If you take a look at today’s starter home, it’s also someone’s downsize,” Masiello says. “People move up and down the ladder of housing styles depending on where they are in their lifecycle.”

Still, while what constitutes a starter home may be changing, the concept of a starter home isn’t going anywhere. In our May 2022 issue, we advised first-time buyers to look for a starter home that they could live in for three to five years, where they could save and build equity to put toward a larger home eventually—and buyers will continue to search for that entry-level home, our experts say.

“I think the starter home is very much a real concept,” Green says. “I think the reality is, people are very mobile in today’s day and age, and whether they’re moving up, moving down, or sideways, those moves are going to take place for a very long time—indefinitely. That will not stop. Because people just like new things. I don’t think it’s really feasible for most people to stay in one home for their whole life. It’s just too difficult because our lives are too transient.”

Starter homes aren’t the only types of homes getting bigger: Homes of all styles have continued to increase in size. The median size of a completed single-family house in 2021 was 2,273 square feet, more than twice the size of estimates of the standard home size in the 1920s.

One explanation for the continued growth of our homes, despite increases in price and cost of building and less open land? Like so many things, it goes back to our new normal of more time at home, which started with the popularity of now-omnipresent innovations (think streaming services) that have brought activities we may have once done outside the home, such as going to the movies, inside. The pandemic sped up this trend, but we were spending more time at home even before 2020, our experts say.

“Nowadays, people actually spend more time at home,” Masiello says. “There are a lot of influences, both societal and technological, that are putting pressure on expanding the house, number of bedrooms, number of bathrooms. Even though the family size or the family composition hasn’t changed much, how we’re using the space has changed quite a bit.”

That use will continue to shift, but one thing certainly won’t: Our collective desire to own our homes, whatever they look like. Throughout the 100 years of Better Homes & Gardens, that home-owning goal has persisted, and it’s not likely to disappear in the next 100 years, either.