generic

generic Is Emerald Health Therapeutics (CVE:EMH) Weighed On By Its Debt Load?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Emerald Health Therapeutics, Inc. (CVE:EMH) does use debt in its business. But should shareholders be worried about its use of debt?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

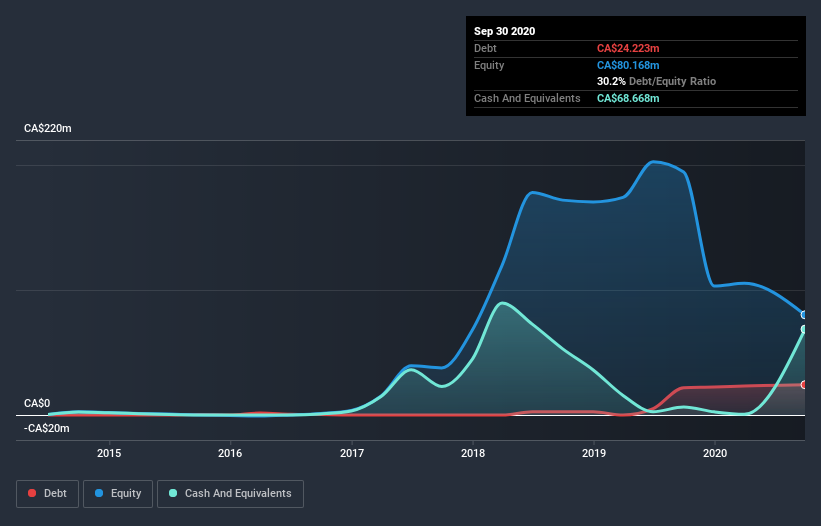

Check out our latest analysis for Emerald Health Therapeutics

How Much Debt Does Emerald Health Therapeutics Carry?

The image below, which you can click on for greater detail, shows that at September 2020 Emerald Health Therapeutics had debt of CA$24.2m, up from CA$21.9m in one year. But on the other hand it also has CA$68.7m in cash, leading to a CA$44.4m net cash position.

How Strong Is Emerald Health Therapeutics' Balance Sheet?

We can see from the most recent balance sheet that Emerald Health Therapeutics had liabilities of CA$26.9m falling due within a year, and liabilities of CA$27.4m due beyond that. On the other hand, it had cash of CA$68.7m and CA$1.56m worth of receivables due within a year. So it can boast CA$15.8m more liquid assets than total liabilities.

This surplus strongly suggests that Emerald Health Therapeutics has a rock-solid balance sheet (and the debt is of no concern whatsoever). With this in mind one could posit that its balance sheet means the company is able to handle some adversity. Simply put, the fact that Emerald Health Therapeutics has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Emerald Health Therapeutics's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Emerald Health Therapeutics made a loss at the EBIT level, and saw its revenue drop to CA$13m, which is a fall of 24%. That makes us nervous, to say the least.

So How Risky Is Emerald Health Therapeutics?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Emerald Health Therapeutics had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of CA$9.9m and booked a CA$125m accounting loss. With only CA$44.4m on the balance sheet, it would appear that its going to need to raise capital again soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Emerald Health Therapeutics has 4 warning signs (and 1 which is a bit unpleasant) we think you should know about.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.