A lot can weigh on the exchange rate between one currency and another, raising questions about when currency fluctuations are, in fact, currency manipulation.

The U.S. Treasury has a bright line test for the latter, and has only denounced countries as currency manipulators four times: twice in 1988 when it enacted the law (Taiwan and South Korea), once in 1994 (China) and then again in August 2019 (China).

In the most recent case, the U.S. argued that China actively devalued its currency to make it more expensive for U.S. exporters to sell goods and services to Chinese buyers. The action is the latest in an escalating trade war between the two nations.

The Treasury has a three-pronged test for identifying a currency manipulator: it must be a net lender to the rest of the world (account surplus), it must be a net exporter relative to the U.S. (trade surplus), and it must be determined that the country levers its currency “for gaining unfair competitive advantage in international trade.”

The “currency manipulator” status is mostly symbolic. By statute, the law requires the Treasury Secretary to engage in negotiations with that country via the International Monetary Fund or in bilateral discussions, but punitive measures could not be taken unless the alleged currency manipulator fails to correct anything in the course of a year.

But not all currency devaluation is currency manipulation, and the difference comes down to how active a government pushes movements in the value of its currency.

Currency depreciation

If you’ve ever traveled to another country, you know that the value of your home currency can fluctuate day-to-day relative to the currency of the country you are visiting. Underpinning those exchange rate dynamics are a web of complex financial happenings at work: central bank actions, sovereign debt holdings, and/or investor speculation.

In general, foreign exchange rates are determined by the supply and demand of currencies across countries.

Holding all else equal, if demand for U.S. dollars increases across the world, purchases of more U.S. dollar-denominated assets would drive the value of the dollar higher against other currencies (appreciation). Conversely, if demand for U.S. dollars decreases across the world, outflows from U.S. dollar-denominated assets would decrease the value of the dollar against other currencies (depreciation).

Interest rates are an example of one factor that can change a currency’s value.

For an investor looking to deposit money and earn interest, a country with higher interest rates would be a more attractive place to park money compared to a country with lower interest rates. As a result, a country with higher interest rates will face higher demand for its domestic currency, strengthening that currency against others.

If the Federal Reserve (the central bank of the U.S.) raises rates to levels above other countries, investors around the world will demand more U.S. dollars thus strengthening the dollar and weakening the currencies of other countries seeing outflows.

But other factors are at play, as well. Even if interest rates are higher in one country, investors may prefer to park money in another country because of expectations for stronger growth. Investors may also steer money away from countries with high interest rates if those countries also suffer from unstable levels of inflation.

All of the dynamics explained above are examples of genuine market forces that can result in currency devaluation.

How to manipulate your currency

By the U.S. Treasury’s definition, currency devaluation becomes currency manipulation when it is actively done by a government for the purposes of gaining a trade advantage.

When a foreign currency depreciates against the U.S. dollar, American exports become more expensive for foreigners to buy. Similarly, the foreign goods become cheaper for Americans to buy, thus exacerbating the trade deficit if the foreign country already exports more goods to the U.S. than it imports.

Countries can manipulate their currencies by actively managing their reserves of foreign currencies to support their home currency at a desired level.

Recall that foreign exchange rates are determined by supply and demand. A country can build up a reserve of U.S. dollars so that if it wanted to weaken its currency, it could sell its own currency and buy U.S. dollars. The resulting demand for foreign currency would devalue the home country’s currency.

In countries that peg or benchmark their currencies to the U.S. dollar, managing currency reserves is mostly innocuous. Some countries, such as Panama, fix their home currency to the U.S. dollar at a rate, like 1-to-1. Doing so requires actively managing substantial reserves of U.S. dollars to keep the peg in place. In the case of a fixed exchange rate, the peg is a way of importing the monetary stability of another country, and leads to no trade advantage for the pegging country.

China, by contrast, runs a variation of a fixed exchange rate; it pegged the yuan to the U.S. dollar until 2005, and has since allowed the yuan to fluctuate within a band relative to other global currencies. But at times, such as in August 2019, the People’s Bank of China has loosened its control to allow the yuan to depreciate further.

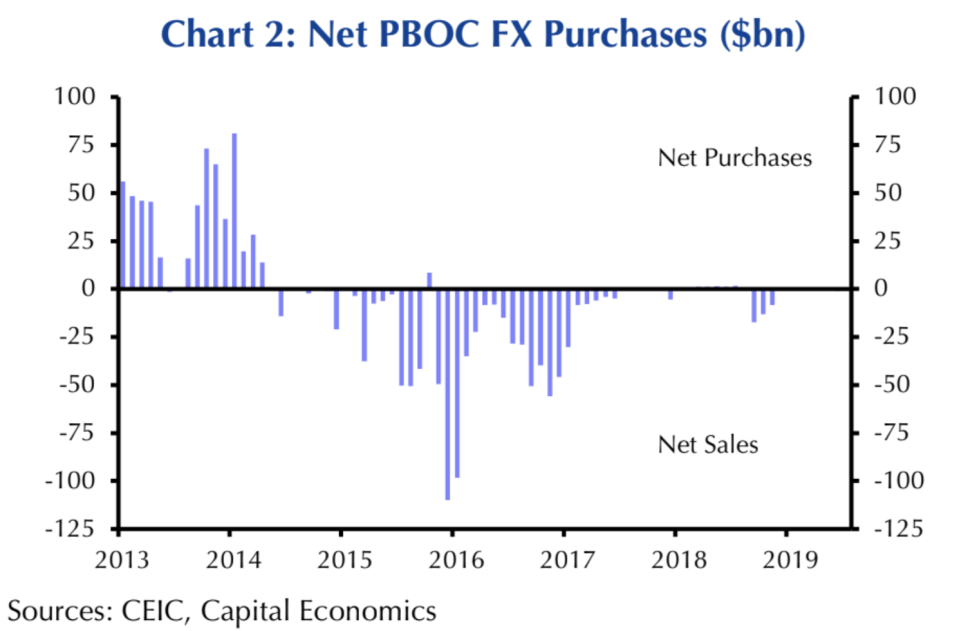

But the yuan’s depreciation appears to be the result of market pressures that China is willing to tolerate, not direct market intervention by the PBOC.

When the PBOC loosened the lower bound of its yuan band in August 2019, the USD/CNY spiked above 7, suggesting that China is not manipulating its currency to push the yuan down, but rather to keep the yuan propped up.

“The US decision to label China a currency manipulator is on shaky economic grounds since, if anything, the renminbi would be even weaker than it is now without policy support,” Capital Economics wrote August 6. Capital Economics also pointed to low activity in foreign exchange markets.

Still, they noted that there was “evidence” that the People’s Bank of China has been using the daily yuan fixing rate and leaning on state banks to “indirectly” intervene in the yuan’s value.

Regardless, with China now officially a “currency manipulator,” the risk of increased sanctions continues to turn the heat up on a trade war that has only gotten hotter as of late.

Brian Cheung is a reporter covering the banking industry and the intersection of finance and policy for Yahoo Finance. You can follow him on Twitter @bcheungz.

Boston Fed President: No 'clear and compelling' case for this week's rate cut

Fed faces questions on ‘data-dependence’ heading into possible rate cut

'Blew it!' Trump's Fed-bashing on Twitter escalates ahead of possible rate cut

Congress may have accidentally freed nearly all banks from the Volcker Rule

Read the latest financial and business news from Yahoo Finance