Viva Leisure (ASX:VVA) shareholders have endured a 60% loss from investing in the stock three years ago

If you love investing in stocks you're bound to buy some losers. Long term Viva Leisure Limited (ASX:VVA) shareholders know that all too well, since the share price is down considerably over three years. Unfortunately, they have held through a 61% decline in the share price in that time. And over the last year the share price fell 45%, so we doubt many shareholders are delighted. Unfortunately the share price momentum is still quite negative, with prices down 8.6% in thirty days.

Now let's have a look at the company's fundamentals, and see if the long term shareholder return has matched the performance of the underlying business.

Check out our latest analysis for Viva Leisure

Viva Leisure wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

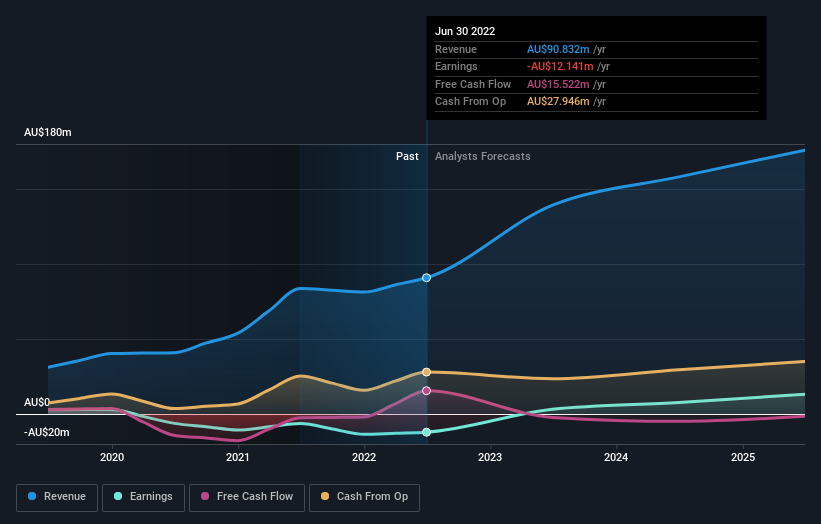

In the last three years, Viva Leisure saw its revenue grow by 37% per year, compound. That is faster than most pre-profit companies. The share price has moved in quite the opposite direction, down 17% over that time, a bad result. This could mean hype has come out of the stock because the losses are concerning investors. When we see revenue growth, paired with a falling share price, we can't help wonder if there is an opportunity for those who are willing to dig deeper.

The graphic below depicts how earnings and revenue have changed over time (unveil the exact values by clicking on the image).

If you are thinking of buying or selling Viva Leisure stock, you should check out this FREE detailed report on its balance sheet.

A Different Perspective

Viva Leisure shareholders are down 45% for the year, falling short of the market return. The market shed around 1.0%, no doubt weighing on the stock price. The three-year loss of 17% per year isn't as bad as the last twelve months, suggesting that the company has not been able to convince the market it has solved its problems. We would be wary of buying into a company with unsolved problems, although some investors will buy into struggling stocks if they believe the price is sufficiently attractive. It's always interesting to track share price performance over the longer term. But to understand Viva Leisure better, we need to consider many other factors. To that end, you should be aware of the 1 warning sign we've spotted with Viva Leisure .

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies we expect will grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on AU exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here