Reports of Walmart's Demise Are Overblown

The share prices of retailers like Walmart (NYSE:WMT) are taking a beating. I do not believe the gloomy forecasts, though, especially for Walmart. In fact, I think the slip following the disappointing first-quarter earnings release presents a potential value opportunity.

Analysts once worshipped at the altar of Americas retailers. Consumer spending has always been considered the engine driving Americas economic life and growth. Following last quarter's reports, they now bemoan retailers, with one analyst dubbing the entire sector as Dead money for the foreseeable future, at best.

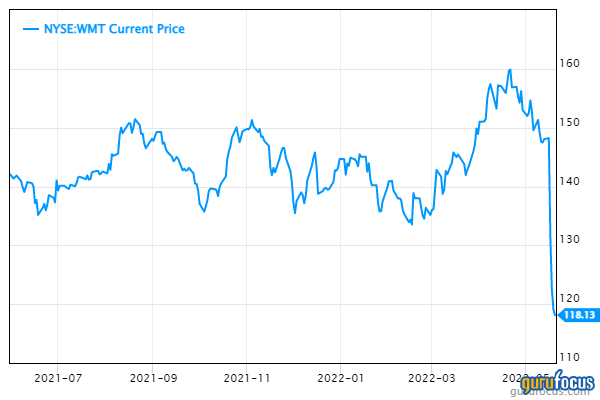

In the short term, the downward pressures from inflation and sell-offs are taking their toll. Walmart is down 16.1% year-over-year. By comparison, Target Corp. (NYSE:TGT) shares are down more than 30% over the past year. The S&P Retail Select Industry Index is down 31.63% year-to-date.

On the other hand, consumer loan balances are down. People still have savings from the early days of the pandemic, which will likely boost travel and provide an inflation buffer of sorts, at least in the short-term. To quote economist Diane Swonk, "Never underestimate the American consumer with money in their pockets."

Walmart is undervalued

Messages about Walmart and the economy in general are mixed at the moment. Bankers are still optimistic about the nation's economic outlook despite inflation, supply chain issues and other impediments. The CEO Bank of America (BAC), Brian Moynihan, recently said, Dont fight the U.S. consumer.

Hedge funds, retail investors and pension funds alike send a different message given Walmart's declining share price. Overall, hedge funds decreased their collective Walmart holdings by 7.3 million shares last quarter.

Nevertheless, GuruFocus only reports one medium risk warning for this stock for insider selling. Walmart has a GF Score of 85 out of 100, driven by strong profitability, decent strenth and GF Value and average growth and momentum.

The full picture

Walmart is much more than just the worlds largest retailer. It is a wholesale distributor through subsidiaries across the world. Additionally, it owns 600 Sams Clubs. Besides retailing, the company holds assets in media tech, retailers of outdoor goods, the largest supermarket chain in Asia, Wim Yogurt, a fashion line, accessories, art decor and real estate.

Walmarts 28 acquisitions over the past few years and multiple investments exceed $21 billion. IT gives them an edge in customer shopping. Management pays special attention to building efficiencies in its online pickup and delivery services through IT. Their IT systems sophistication is one of the main reasons behind Walmarts ascension, and I believe this can carry forward to future growth.

One promising acquisition was when Walmart bought Botmock in 2021 to expand capabilities for management to collect vast amounts of data from customers and analyze it in real-time. They know every aspect of the customers in-store, online, SMS and phone experiences. Managers can make quick decisions to control costs more efficiently and optimize the shopping experience. They will no longer need to rely on the weeks-long wait for cumbersome batch uploads to make near-term decisions.

When will growth return?

Walmart shares are now selling at their lowest so far in 2022. This was after the company reported fiscal first-quarter 2023 earnings of just $1.30 per share, which was below analysts' estimates.

Revenue was up just 2.4% to $141.5 billion, vastly below inflation. The cost of doing business was higher than forecast at $106.8 billion versus estimates for $103.9 billion. The gross margin of 23.84% was lower than expected.

I believe the bright spots in the report were U.S. comp sales that grew 3.0% and 9.0% on a two-year stack. E-commerce growth rose a mere 1%, though, for growth of 38% on a two-year stack basis. Sams Club comp sales increased 10.2%, and 17.4% on a two-year stack basis, showing a shift towards cheaper groceries. Membership income increased by 10.5%.

The next report date is August 15. It will likely be another quarter that disappoints analysts, but I believe any retailer should be happy having these numbers to report. I expect earnings per share to be $1.82 for the second quarter of fiscal 2023; I'm far more bullish on the stock than most Wall Street analysts, who have issued price targets averaging out to $157.50.

Some risks include the fact that the company has a seedy reputation in some quarters. Management is accused of fighting demands for better wages and benefits for workers, and no one with a brain can really deny that that's exactly what they're doing. Activists call it "Greed in the Suites." Operations in Germany failed, and this failure was attributed to employment policies in the country that guarantee certain benefits for workers.

Walmart focuses heavily on brick-and-mortar operations. Management is deservedly criticized for flagging in terms of e-commerce results. That is changing, but not fast enough. Digital sales grew 1% year-over-year for the first quarter, and overall revenue growth was more than twice that rate.

Last aisle

I dont buy analysts estimates that earnings per share will continue fueling a significant fall in the share price. I think shares might tumble to the $100 range in the short term if the stock market drops and the company continues disappointing on the earnings front. Nobody can stop a freight trains downslide on a dime. The drag on Walmart might continue for another quarter or two, but still, I think the 12-month average price target from analysts is undeservedly low.

Inflation is the major concern at Walmart because it eats into earnings. Other factors to consider in future retail sales are disposable income, income per capita, income inequality, household debt, and consumer confidence; these metrics are all improving for now and are the foundation for the positive forecast I envision for Walmart. Even if the economic situation gets worse, Walmart's private brand sales should get a boost from poorer consumers, which means better margins.

This article first appeared on GuruFocus.