Loyalty Ventures: A High-Risk, High-Reward Opportunity

Plano, Texas-based Loyalty Ventures Inc. (LVLT) looks like it is circling the drain. However the situation is not as bad as it appears.

The company was spun off of Alliance Data Systems (now called Bread Financial Holdings Inc. (NYSE:BFH)) in November of 2021. As part of the transaction, Loyalty Ventures paid $750 million to its former parent. To add insult to injury, Loyalty Ventures was also responsible for paying Canadian withholding taxes associated with the deal, which was funded by debt.

This debt has created a millstone around Loyalty Ventures' neck, so when the bear market began ealier this year, the stock cratered, losing over 90% of its value in short order.

Loyalty Ventures describes itself as a provider of tech-enabled, data-driven consumer loyalty solutions. It owns and operates the Canada-based Air Miles Reward Program and the Netherlands-based Brand Loyalty, which provides customized campaign-based loyalty solutions for grocers and other high-frequency retailers.

The Air Miles Reward Program is a loyalty program for sponsors who pay a fee per reward mile issued, in return for which the program provides all marketing, customer service, rewards and redemption management. The Brand Loyalty segment provides points-based programs for retailers.

Prior to the spinoff, the business was the LoyaltyOne segment of Alliance Data Systems. Last year, it had over 1,400 employees and generated $764.8 million in revenue, $75.1 million in net income and $173.4 million in adjusted Ebitda.

As of March, Loyalty Venture's balance sheet is highly leveraged and the equity cushion is small.

Note the large amount of current liability, which is mostly made up of unredeemed benefits of the Air Miles program. Customers purchase Air Miles points from Loyalty Ventures to give to its own customers as a reward for their loyalty. The sold points become a liability of Loyalty Ventures' balance sheet and, over time, they are either redeemed for rewards or are abandoned or forgotten by users. The company estimates that about 20% of these points are never redeemed. These points, called "breakage," become profit for the company as they roll off the liability side of the balance sheet.

According to the company's 10-Q filing, long-term debt consists of:

Description | March 31, 2022 | Maturity |

(in thousands $) | ||

Revolving credit facility (1) | 1-Nov-26 | |

Term loan A | 171,719 | 1-Nov-26 |

Term loan B | 490,625 | 1-Nov-27 |

Total long-term debt | 662,344 | |

Less: unamortized debt issuance costs | 20,005 | |

Less: current portion | 50,625 | |

Long-term portion | 591,714 |

(1) | As of March 31, availability under the revolving credit facility was $133.9 million. |

The company does not face debt maturity payments until November 2026 and, as of March, was compliant with debt covenants.

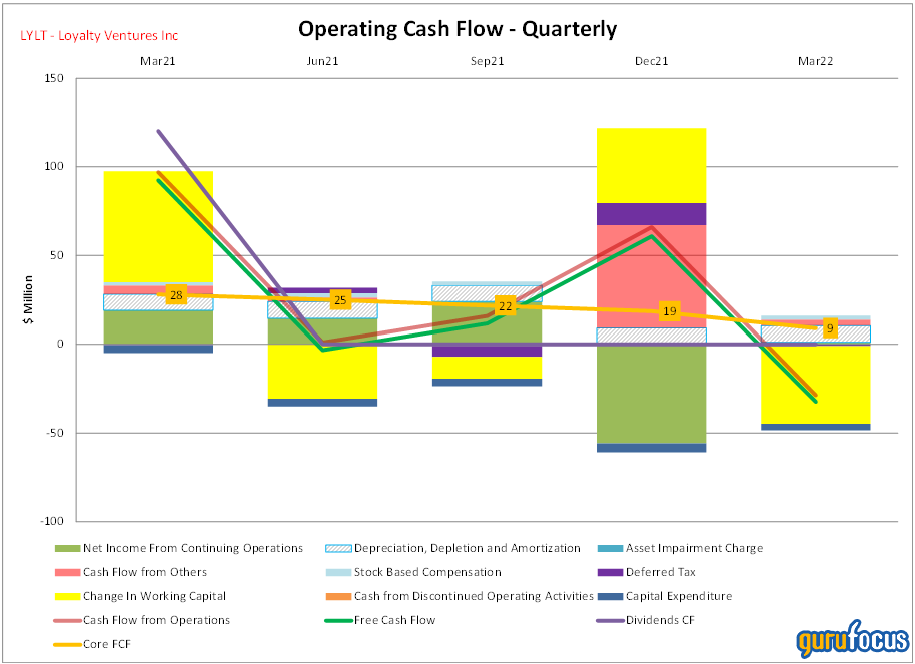

The following diagram shows the company's operating cash flow. Loyalty Ventures has large swings in working capital (yellow bars). The orange line shows core free cash flow, which is free cash flow without changes in working capital. The company's core free cash flow is positive, which is remarkable given how far the stock has fallen. However, the core FCF line does show a declining trend, so its imperative the company reverses this trend.

Conclusion

It appears the market has overreacted by dumping Loyalty Venture's stock. It is true that the company carries a lot of debt, so if there is a recession, business will go down significantly as customers are likely to cut spending. Recently, one of its largest customers, Canadian grocery chain Sobeys, decided not to renew its participation in the Air Miles program, which hit the stock hard.

While a more than 90% drawdown implies the company is likely going out of business, it does not appear that this is imminent. Sobeys represented only 10% of Loyaltys Ebitda, so the company has a lot of levers left to pull. There are no near-term debt maturities, the company is core free cash flow positive and appears to have sufficient liquidity to survive an economic downturn.

As a result, there is little doubt it will have to cut costs in the short term as well as invest in sales and marketing to rebuild the business. The company has a couple of years to stabilize operations and roll over its debt. If Loyalty Ventures can get back to making about $125 million a year in free cash flow, it can get debt under control quite quickly and will not have too much trouble refinancing.

My analysis indicates the upside to downside ratio is in favor of investment. A lot of investors likely sold out of the stock because they got it as part of the spinoff and could not be bothered to analyze the stock.

In this market, investors shoot first and ask questions later. If the company can stabilize its business and maintain its free cash flow, the upside is a multi-bagger while the downside is practically zero. There is also an interesting possibility of a takeover by private equity given the company's ability to generate free cash flow.

This article first appeared on GuruFocus.