Here's Why We Think Literacy Capital (LON:BOOK) Is Well Worth Watching

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Unfortunately, these high risk investments often have little probability of ever paying off, and many investors pay a price to learn their lesson. Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Literacy Capital (LON:BOOK). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Literacy Capital with the means to add long-term value to shareholders.

View our latest analysis for Literacy Capital

Literacy Capital's Improving Profits

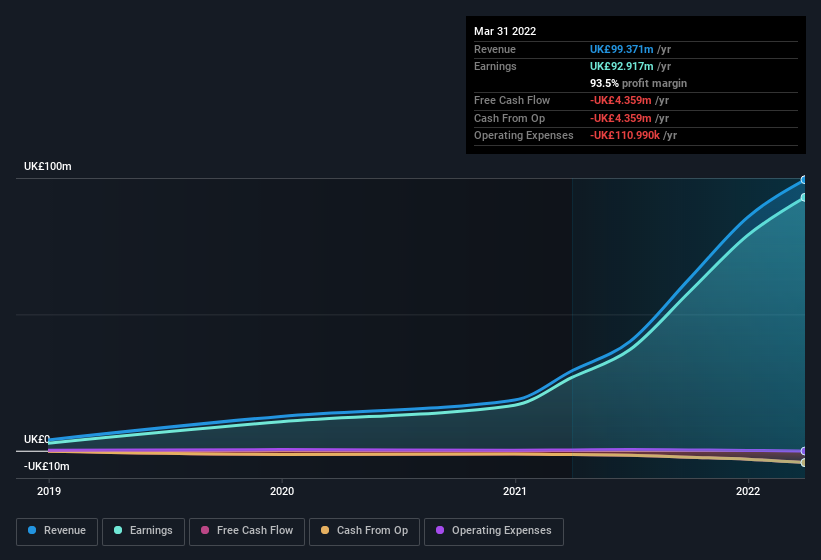

Even modest earnings per share growth (EPS) can create meaningful value, when it is sustained reliably from year to year. So it's easy to see why many investors focus in on EPS growth. It's an outstanding feat for Literacy Capital to have grown EPS from UK£0.45 to UK£1.55 in just one year. Even though that growth rate may not be repeated, that looks like a breakout improvement. This could point to the business hitting a point of inflection.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. Not all of Literacy Capital's revenue this year is revenue from operations, so keep in mind the revenue and margin numbers used in this article might not be the best representation of the underlying business. Literacy Capital maintained stable EBIT margins over the last year, all while growing revenue 239% to UK£99m. That's a real positive.

You can take a look at the company's revenue and earnings growth trend, in the chart below. For finer detail, click on the image.

Since Literacy Capital is no giant, with a market capitalisation of UK£240m, you should definitely check its cash and debt before getting too excited about its prospects.

Are Literacy Capital Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

The first bit of good news is that no Literacy Capital insiders reported share sales in the last twelve months. But the important part is that Independent Non-Executive Director Christopher Sellers spent UK£416k buying stock, at an average price of UK£3.47. Big buys like that may signal an opportunity; actions speak louder than words.

On top of the insider buying, we can also see that Literacy Capital insiders own a large chunk of the company. Indeed, with a collective holding of 70%, company insiders are in control and have plenty of capital behind the venture. Intuition will tell you this is a good sign because it suggests they will be incentivised to build value for shareholders over the long term. That level of investment from insiders is nothing to sneeze at.

Does Literacy Capital Deserve A Spot On Your Watchlist?

Literacy Capital's earnings per share growth have been climbing higher at an appreciable rate. The icing on the cake is that insiders own a large chunk of the company and one has even been buying more shares. These factors seem to indicate the company's potential and that it has reached an inflection point. We'd suggest Literacy Capital belongs near the top of your watchlist. You should always think about risks though. Case in point, we've spotted 2 warning signs for Literacy Capital you should be aware of, and 1 of them is concerning.

Keen growth investors love to see insider buying. Thankfully, Literacy Capital isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.