How To Bounce Back Financially in 2021

If you’ve started the new year off with a resolution to improve your finances, you might be wishing you’d tackled something less daunting like going to med school or climbing Mount Everest. The problem is, we usually make sweeping resolutions to optimize our money matters when said money matters aren’t going so well. I have no personal insight on the matter, but I’m pretty sure Jeff Bezos and all the other ultra-billionaires out there didn’t ring in 2021 with the wish to dig themselves out of a financial hole. They might have resolved to become richer, but that’s another matter.

The Economy and Your Money: All You Need To Know

Follow Along: 31 Days of Living Richer

For the rest of us who didn’t directly profit from the global pandemic and might just have accrued some serious debt in 2020, getting in good financial standing can feel impossible. But there is a way out: You just have to know what to do. Here’s a step-by-step guide to bouncing back — by way of your bank account — in this still young and fragile new year.

Last updated: Aug. 10, 2021

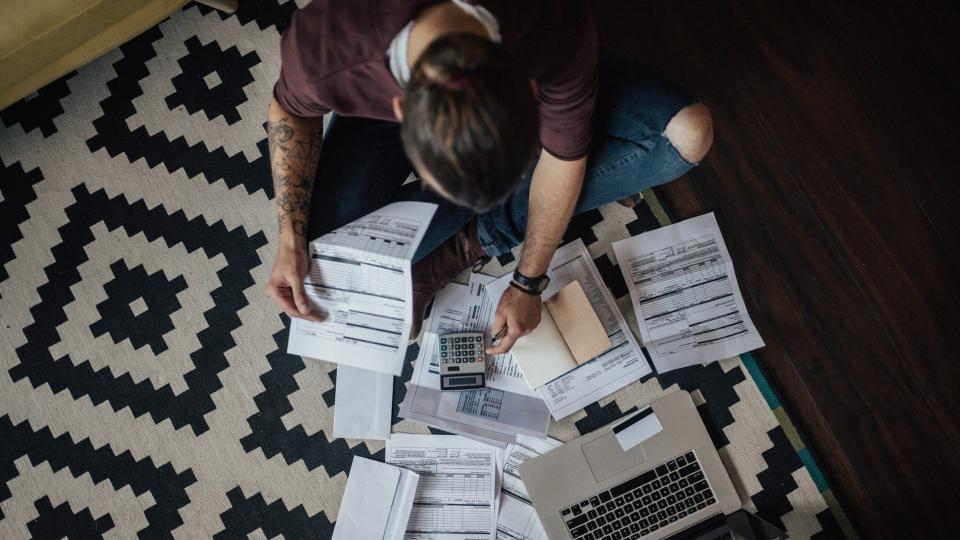

Step 1: Take Stock of Your Current Financial State

“Take time to evaluate your financial life and see where you stand,” said Brittney Castro, founder and CEO at Financially Wise and CFP at Mint. “Review your budget, update or create new financial goals for 2021, take account of all your assets, liabilities, insurances and estate documents. List all the positives in your financial life and the lessons you learned about money in 2020. Reflecting will help you see how far you’ve come while also providing motivation to reach your financial goals.”

Taking stock of your financial life also means getting up to date on your credit and where you stand there.

“I suggest getting one report from one of the three different credit reporting agencies every four months," said Jeanette Pavini, personal finance reporter and author of "The Joy of $aving." "Knowledge is power; so know what is happening with your credit. A good credit record can save you thousands of dollars over the years in interest since typically the better your credit, the lower the interest rate. Many times, our credit is in better shape than we may have thought, and if there is a problem, you can work to correct it.”

Read More: 15 Ways To Dramatically Increase Your Income in 2021

Step 2: If You’re In Trouble, Assess What Got You There

Before you budget or do anything else to dig yourself out of the hole you’ve found yourself in: Stop, breathe and take an investigative look into when things started to go wrong and how.

“In most cases, an unexpected turn of events (like the pandemic) led to your money challenges, but that does not mean that you did not play a part,” said Hussein Ahmed, founder and CEO of Oxygen Bank. “The most important thing to getting back on track is to take control of your financial life and ensure that you have enough savings to cover unexpected expenses that inevitably occur. This alone is the difference between personal boom and bust cycles.”

Learn More: Pandemic Relief Programs Are Ending — Here’s How You Can Still Get Assistance

Step 3: Assess Your Debts — and Calculate Your Net Value

“Review all debts, especially that may have occurred due to the pandemic,” said Todd Bryant, CFP, founding partner and financial planner, Signature Wealth Advisors, LLC. “Your monthly cost, your interest rates and how many years left are basic pieces of information that many people don’t know off hand.”

Millions of Americans are net worth negative — meaning their debts outweigh their assets.

“In and of itself, this isn't a bad thing seeing as debts like mortgages and student loans are so ubiquitous,” said Jim Pendergast, senior vice president of altLINE. “That said, creeping liabilities such as credit card balances need to be identified as soon as possible. The only way to do that is to calculate your actual net worth, which totals all money in bank accounts, retirement accounts, investment funds and potentially real estate. Then, you subtract outstanding debts. If the total is positive, you can begin to be more aggressive with your 2021 financial goals. If it's negative, your attention needs to shift to debt repayments.”

Find Out: 11 Steps for Paying Off Credit Card Debt in 2021

Step 4: Build a Budget Around All Your Goals (Not Just Financial Ones)

“If you have had a hard financial stretch — and really, finances have changed for almost everyone as a result of the pandemic — it’s time to start fresh with budgeting,” said Tanya Peterson, vice president, Freedom Financial Network. “Rather than intended to restrict spending, a budget is a plan that will guide you in spending in line with your goals. So, start by setting goals [listing] everything from buying a house to getting out of debt, to making sure you have time for daily exercise. Then build the budget around the goals. You’ll likely modify, but you’ll know where you’re going.”

When budgeting, take care to “give every dollar a job,” as Brian Martucci, personal finance expert at Money Crashers, puts it. What this means is to understand “exactly what you spend in every discretionary and non-discretionary spending category, from housing to food to entertainment,” he said. “Use a budgeting app that links with your day-to-day financial accounts to make this easier, and remember to save (in a dedicated account) every dollar that doesn’t have a ‘job.’”

Take care to really focus on your goals though — not just what you want to cut, but what you eventually want to gain by reaching financial solvency.

“When it comes to our finances, we often rely heavily on cutting back or on the things we can't have,” said R.J. Weiss, CFP and founder of the personal finance site The Ways to Wealth. “This is not a recipe for long-term success; Instead, set financial goals that excite you. This could be travel, a home project or even rewarding yourself in a fun way for accomplishing a milestone like paying off your credit card debt.”

Read More: A Month-By-Month Guide to Expanding Your Savings Account in 2021

Step 5: Determine How To Generate More Income

Often when we set about getting our finances in order, the immediate solution that comes to mind is to cut costs. And absolutely, finding ways to save more money is important. But what if you’ve already slashed your budget to cover just essentials and are still in a financial rut? Such is the situation for millions of Americans who are struggling to cover basic expenses like rent.

“If cutting costs isn’t an option, figure out how you can create new income streams or add to the ones you already have,” said Bobbi Rebell, CFP, personal finance expert at Tally. “Start by reassessing the skills you have that can make money. For example, there are many opportunities for online tutoring now. People are also more open to online events and entertainment. Depending on your job situation you can consider asking for a raise. If you have your own business, you might consider inching your prices upward. Many clients won’t mind paying a bit more if they are happy with your work. You can also try to come up with additional add-ons to better serve clients and increase your income.”

Find Out: 100 Ways To Make Money Without a 9-to-5

Step 6: Get To Work Networking

You should also jazz up your LinkedIn, per the recommendation of Charlotte DeMocker, co-founder and COO of Penny, and reconnect with your network.

“They say it's not about what you know, but who you know. And unless you've been hiding under a rock, it is likely that you will have come across hundreds, if not thousands, of people over the course of your career — including people that you might have gone to school or college with,” DeMocker said. “Also, tap your second-degree networks. You have nothing to lose, so don't be shy: Tell your contacts that you are looking out for work or income opportunities, and ask them if they know anyone who you should be speaking to. One of the few advantages of an extended lockdown is that everyone else is sitting around at home, too. You will be surprised at how many people will be pleasantly surprised to hear from you.”

Learn More: What It’s Like To Job Hunt During a Pandemic

Step 7: Make Savings Automatic

“One lesson from 2020 is that we never know what expenses will come up or if our income will decrease,” Pavini said. “Start by trying to find ways to cut your monthly expenses and put that money into a savings account. For example, let’s say you cut your grocery bill by $10 a week. That can add up to $520 a year. Set up an autopay into a savings account on a weekly or monthly basis. Even if you are saving $20 a paycheck, it will add up.”

What To Do: How To Manage All the Extra Debt You Piled Up in 2020

Step 8: Set Up New Systems for a Better Year

“To stay organized and prevent financial uncertainty in the future, establish regular ‘money dates’ in 2021,” Castro said. “This is a dedicated time each week or month to review your financials. During your money dates, you can review your budget, track your expenses, stay on top of your accounts or handle any calls or financial to-do items. Keeping track of your goals regularly will help you notice any problem patterns early and celebrate the small wins along the way.”

More From GOBankingRates

What Money Topics Do You Want Covered: Ask the Financially Savvy Female

Nominate Your Favorite Small Business To Be Featured on GOBankingRates

This article originally appeared on GOBankingRates.com: How To Bounce Back Financially in 2021