Bank of Canada hikes rate quarter-point, but signals it may be the last

The most aggressive series of interest rate increases in Canada’s history might be over.

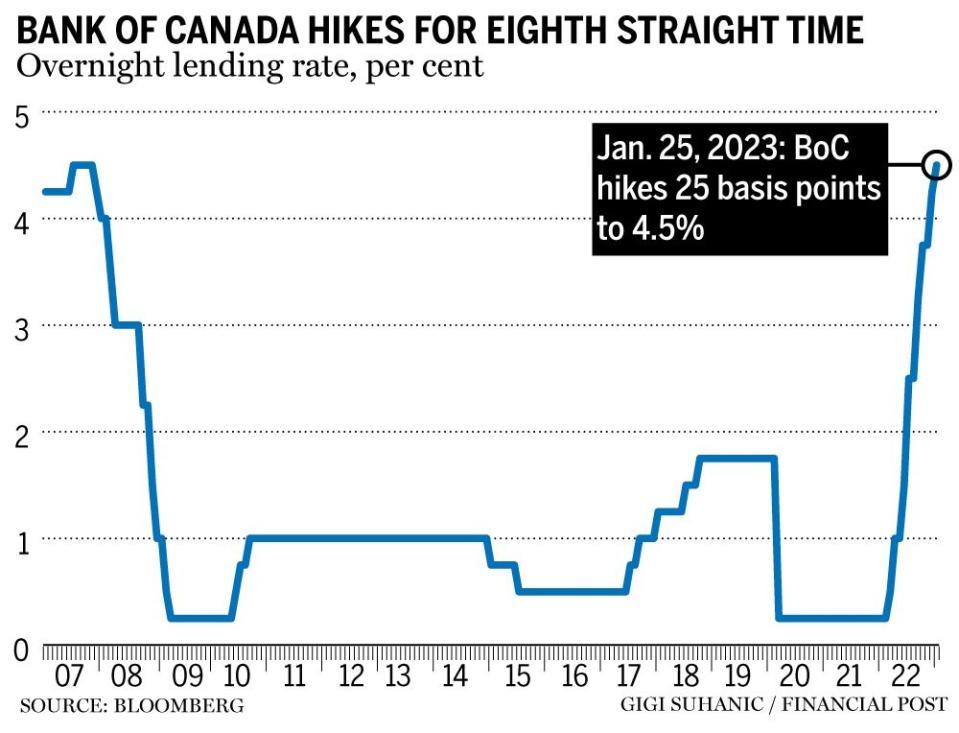

Bank of Canada governor Tiff Macklem raised the benchmark rate a quarter-point on Jan. 25, lifting the rate that private lenders use to set retail and commercial borrowing costs to 4.5 per cent — a startling surge from 0.25 per cent a year ago.

Many on Bay Street saw that coming.

Few — and perhaps no one — anticipated an explicit promise from Macklem to stop here, assuming things unfold as the central bank foresees in its latest quarterly Monetary Policy Report.

“If economic developments evolve broadly in line with the MPR outlook, Governing Council expects to hold the policy rate at its current level while it assesses the impact of the cumulative interest rate increases,” the central bank said in a statement.

“Governing Council is prepared to increase the policy rate further if needed to return inflation to the two per cent target and remains resolute in its commitment to restoring price stability for Canadians.”

That last part is meant to make sure no one confuses Macklem’s message with a declaration of victory in his fight against the worst inflation scare since the early 1980s. Embers remain hot, as Canada’s economy continues to exhibit signs of “excess demand,” including elevated prices for domestic services and surveys that suggest employers are still struggling to find workers.

Policymakers won’t be considering interest rate cuts anytime soon, and if the inflationary fever persists, the central bank will raise interest rates again. But that’s not what it sees happening.

The Bank of Canada noted that headline inflation — as measured by year-over-year changes in Statistics Canada’s consumer price index — dropped to 6.3 per cent in December from a peak of 8.1 per cent in June.

Watch the Bank of Canada press conference below

Macklem and his deputies predict that trend will continue, mostly because energy prices have declined, and because global supply chains are loosening. The Bank of Canada’s new outlook predicts that year-over-year increases in the CPI will average 5.4 per cent over the first quarter, and drop to 2.6 per cent by the end of 2023.

The updated inflation forecast is significant because it suggests price increases will be back in the central bank’s comfort zone of one per cent to three per cent before the year is over. The forecast puts inflation back at two per cent — the midpoint of that comfort zone — sometime in 2024.

“Inflation is projected to come down significantly this year,” the statement said.

That achievement won’t come without pain, some of which is already being felt by homeowners with variable-rate mortgages and anyone who relies on a vibrant real-estate market to make a living. Home prices have plunged and are expected to drop further, the central bank said. The housing industry subtracted a full percentage point from economic growth in 2022, and will subtract 0.7 percentage points in 2023, according to the MPR.

Housing is probably the industry that’s most sensitive to interest rates. It led the rapid recovery from the COVID-19 recession, when the Bank of Canada dropped the benchmark rate to almost zero and promised to keep it there for two years.

Now, housing is acting as a brake on unsustainably fast economic growth — five per cent in 2021 and 3.6 per cent in 2022 — that was stoking more demand than suppliers could match.

The Bank of Canada’s new outlook predicts the economy will grow at an annual rate of 0.5 per cent in the first quarter, down from 1.3 per cent in the fourth quarter of 2022. That’s stall speed, so the economy could easily tip into recession this year, an outcome Macklem has indicated he’s willing to accept if that’s what it takes to crush inflation, which he has identified as the bigger threat.

“Recent economic growth has been stronger than expected and the economy remains in excess demand,” the Bank of Canada said in the policy statement. “However, there is growing evidence that restrictive monetary policy is slowing activity, especially household spending.”

Canada’s economy is predominantly fuelled by household and government spending, business investment and exports. Consumption is the most important, and it will slow considerably this year as households are forced to use more of their disposable income to service debt.

The Bank of Canada said interest payments on mortgages will be about 4.5 per cent of disposable income at the beginning of 2023, up from 3.2 per cent at the same point in 2022. That percentage will only grow as homeowners renew their mortgages at higher rates, subtracting income that could otherwise have been used to spend and invest.

That’s how recessions start, but that might be what’s required to smother the inflationary pressures ignited by the recovery from the pandemic. The Bank of Canada seems to think the pain will be worth it.

“This overall slowdown in activity will allow supply to catch up with demand,” the statement said.

• Email: kcarmichael@postmedia.com | Twitter: CarmichaelKevin