Yahoo Finance

Yahoo Finance What the Bank of Canada’s full percentage point hike means for the housing market and your mortgage

The Bank of Canada’s surprise move to hike its policy rate by a full percentage point — with no indication it will stop there — will add to the financial squeeze faced by indebted homeowners and likely push more buyers to the sidelines of already cooling real estate sector, market watchers said Wednesday.

The move, which sent a statement about the central bank’s resolve in combatting inflation, brought the policy rate to 2.5 per cent and came in higher than the 75-basis point hike most had expected.

Industry experts expressed shock at the size of the move.

James Laird, Co-CEO of Toronto-based mortgage brokerage Ratehub.ca, said he was initially taken aback by the move until he considered the Bank’s language leading up to the decision, reiterating the need to “act more forcefully” to bring inflation down.

Laird said the oversized hike could put further downward pressure on cooling real estate markets across the country and push balanced markets across many regions to move toward buyer’s market territory.

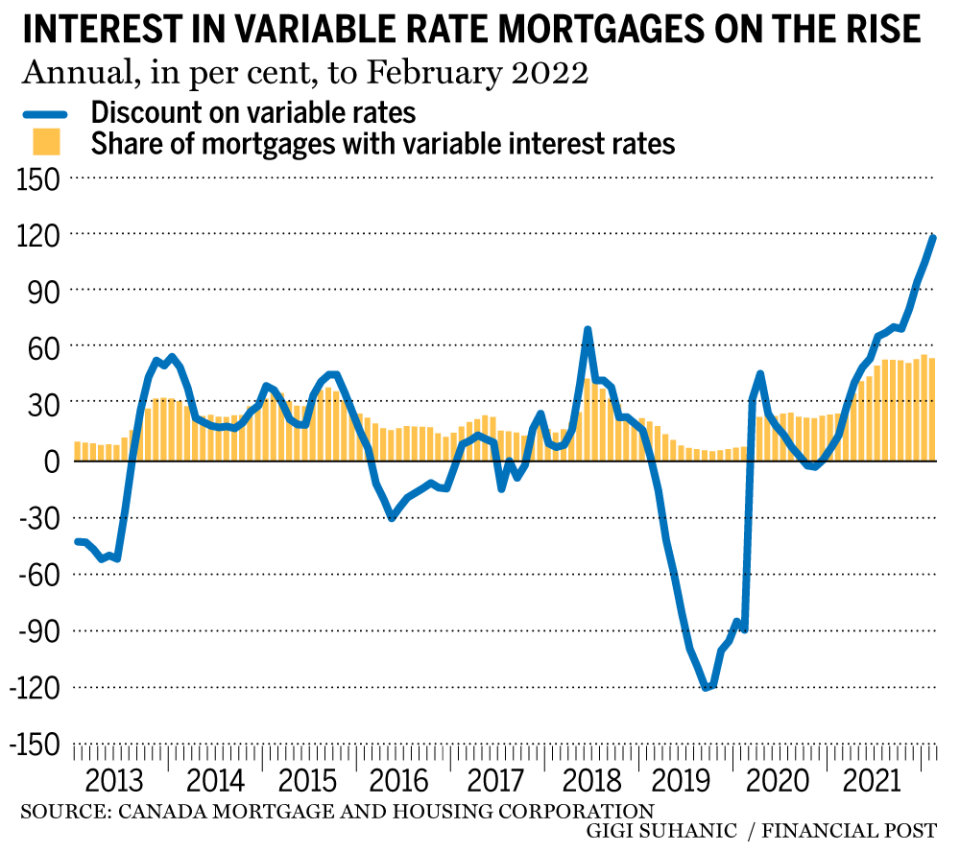

Housing markets have been cooling off rapidly since the prospect of a rate hike cycle pulled demand forward into the latter parts of 2021 and the first months of 2022, ahead of the Bank’s first hike in March.

Laird said that with a hike this large, some Canadians who have purchased at the height of the pandemic may be underwater, but Canadian families are viewing their properties more as a home rather than an investment vehicle.

“There’s not as much regret as you might think,” he said. “People are generally happy to be in a place and be able to focus on other parts of their lives because the first-time homebuyer journey (is) so challenging.”

Ron Butler, mortgage broker and owner of Toronto-based brokerage Butler Mortgage, wrote in a tweet that prime rates and the cost of home equity lines of credit are moving up in a big way.

“Huge 100 bps increase … means bank prime is now 4.70 (per cent) and most HELOC rates are 5.20 (per cent),” Butler tweeted moments after the announcement. “The purchase of a rental property accessing a HELOC on an existing property for down payment is simply becoming unmanageable.”

Butler added that he expects home prices to decline steadily as a result, but that the Bank’s hawkish language means there could be more to come.

“Now our attention switches to the September prime rate announcement. Yep … this can and likely will gets worse in six weeks.”

The Bank of Canada has already delivered three rate hikes since March: one 25-basis point increase followed by two 50-point hikes. The increases, coupled with strong messaging from central bank Governor Tiff Macklem telling Canadians to expect interest rates to rise further this year, have been working to cool housing markets across Canada —particularly in major cities.

Toronto home sales plunged just over 41 per cent in June compared to the same month a year ago while Vancouver saw its sales slip 35 per cent in the same timeframe. Home prices have been declining at a slower pace in both markets since early in the year. The market slow-down has been largely taken as a sign that prospective home buyers are treading more cautiously.

For Canadians who have already pulled the trigger on buying a home, rate hikes have been making mortgages more expensive and a full percentage increase will further weigh on household balance sheets. Canadians with a fixed-rate mortgage will not see changes to their payments until their mortgages comes up for renewal.

Interest rates are still rising, but investors should start preparing for when they come back down

Bank of Canada raises interest rate: Read the official statement

However, variable-rate mortgage holders can expect to feel the pinch within a few months. A recent report from the Canada Mortgage and Housing Corporation found that more Canadians have been piling into these kinds of mortgages during the pandemic, driving variables’ share of the market above 50 per cent.

A Canadian with a mortgage loan amount of $500,000 with a current variable rate of 2.85 per that amortizes over 20 years would have a monthly payment of around $2,735.

After a full percentage point hike brings that variable rate up to 3.85 per cent, the monthly payment would jump to $2,990. This means a Canadian in this situation could be paying $255 more a month or approximately $3,060 more each year.

Assuming an average variable rate of 1.60 at the start of the year, the combined cost of this year’s rate hikes would be approximately $554 more per month or $6,648 per year.

Financial Post

• Email: shughes@postmedia.com | Twitter: StephHughes95