Mortgage-Rate Rise Hits Coastal Property Markets Hardest

Preston Gannaway for The Wall Street Journal

Pricey real-estate markets on the coasts are bearing the brunt of the recent rise in mortgage rates and are likely to feel more pain as rates climb, housing economists say.

The average rate for a 30-year mortgage has risen to 4.12% from 3.5% before the election in November.

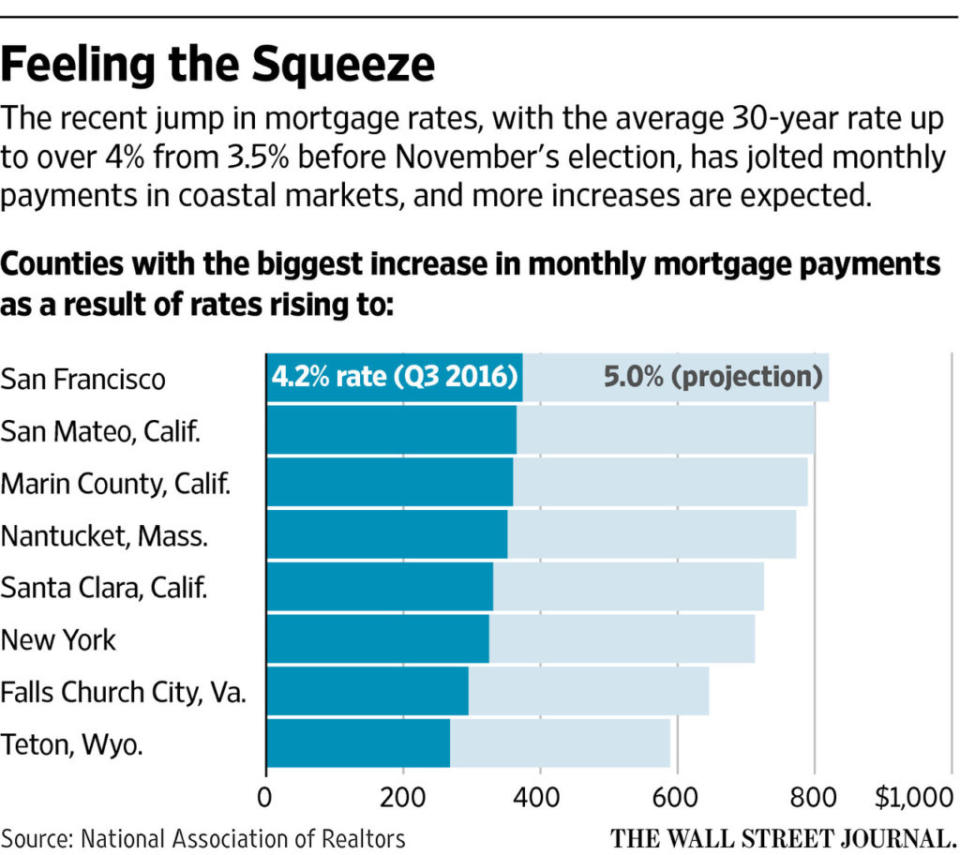

An analysis by the National Association of Realtors found that home buyers in California’s San Francisco County have seen the biggest impact of the rate jump, with a nearly $375 increase in typical monthly mortgage payments for buyers over the last couple of months.

“It’s sort of a double whammy,” said Danielle Hale, NAR’s managing director of research. At a time when apartment rents are climbing quickly, home prices and mortgage rates also are going up, making it tougher to get into the housing market, she said.

On the other end of the spectrum, Cochran County, Texas, has felt the smallest impact from rising rates, with the typical mortgage payment going up by just $13 a month since November.

The disparity reflects a deep divide in home prices between the nation’s priciest and least expensive markets. The median home value in San Francisco, at more than $1 million, is 28 times that of Cochran County, a rural area near the New Mexico border.

After San Francisco, the markets that have suffered the most from higher rates include San Mateo County in California, Nantucket County in Massachusetts, New York County and Teton County in Wyoming.

The markets that are seeing the smallest impact are scattered across such as Texas, West Virginia, Kentucky and South Dakota.

News Corp, owner of The Wall Street Journal, also operates Realtor.com under license from the National Association of Realtors.

Home prices in expensive coastal markets have seen a rapid run-up in prices, driven by a lack of fresh supply and a flood of new jobs. The median home price in San Francisco County is now 39% above its precrisis peak, according to the California Association of Realtors.

But there is evidence that buyers are reaching the limit of what they can afford. Jeff Barnett, a Realtor in Silicon Valley, said the market there has slowed, with about 5% less sales in 2016 than the year before.

“Unless you have unlimited funds, every little tick up in the interest rate lets you buy less and takes people out of the market if they’re struggling to buy their first home,” he said.

More pain could be on the horizon. The NAR expects rates to rise to 4.4% by the end of 2017 and 4.8% in 2018.

Real-estate agents are bracing for changes to the tax code that could take an even greater toll on once-hot coastal markets.

The headwind of higher rates comes as Congress is considering a tax overhaul championed by some Republicans that could include the elimination of the deduction for state and local property taxes.

Taxes typically are higher in areas with pricey real estate. And homeowners in those areas are more likely to use the deduction because they have higher incomes and are more likely to itemize on their returns. The changes could mean that buyers gravitate toward less expensive homes.

The post Mortgage-Rate Rise Hits Coastal Property Markets Hardest appeared first on Real Estate News & Advice | realtor.com®.