Should You Invest In The Oil & Gas Stock Solo Oil Plc (AIM:SOLO)?

Solo Oil Plc (AIM:SOLO), a GBP£18.64M small-cap, operates in the oil and gas industry which has persevered through a prolonged oil price downturn since mid-2014. However, energy-sector analysts are forecasting for the entire industry, negative growth in the upcoming year , and a massive growth of 41.87% over the next couple of years. This rate is larger than the growth rate of the UK stock market as a whole. Is now the right time to pick up some shares in oil and gas companies? Below, I will examine the sector growth prospects, and also determine whether SOLO is a laggard or leader relative to its energy sector peers. Check out our latest analysis for Solo Oil

What’s the catalyst for SOLO’s sector growth?

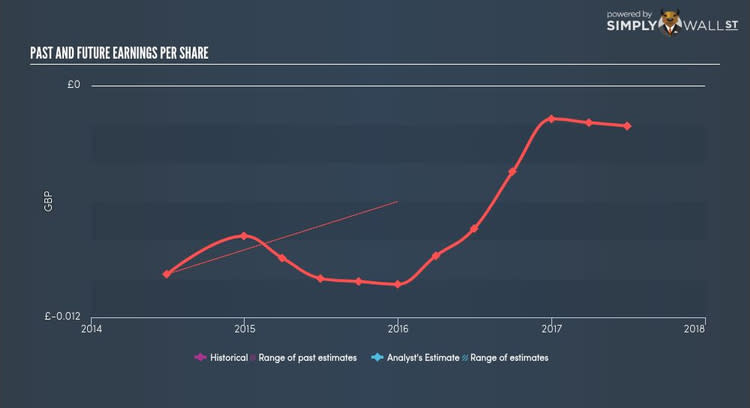

The oil price collapse triggered a wave of cost reduction among energy businesses as the sector as a whole faced negative growth over the past five years. Large energy businesses have slashed their growth expenditures by over 40% since the collapse, and reduced headcount by nearly half a million workers. Only now has the sector begun to emerge from its turmoil, and in the past year, the industry turnaround delivered growth of over 50%, beating the UK market growth of 11.30%. SOLO lags the pack with its sustained negative earnings over the past couple of years. The company’s outlook seems uncertain, with a lack of analyst coverage, which doesn’t boost our confidence in the stock. This lack of growth and transparency means SOLO may be trading cheaper than its peers.

Is SOLO and the sector relatively cheap?

Oil and gas companies are typically trading at a PE of 14x, in-line with the UK stock market PE of 19x. This illustrates a fairly valued sector relative to the rest of the market, indicating low mispricing opportunities. However, the industry returned a lower 5.74% compared to the market’s 12.78%, illustrative of the recent sector upheaval. Since SOLO’s earnings doesn’t seem to reflect its true value, its PE ratio isn’t very useful. A loose alternative to gauge SOLO’s value is to assume the stock should be relatively in-line with its industry.

What this means for you:

Are you a shareholder? SOLO recently delivered an industry-beating growth rate in earnings, which is a positive for shareholders. If you’re bullish on the stock and well-diversified by industry, you may decide to hold onto SOLO as part of your portfolio. However, if you’re relatively concentrated in oil and gas, you may want to value SOLO based on its cash flows to determine if it is overpriced based on its current growth outlook.

Are you a potential investor? If SOLO has been on your watchlist for a while, now may be the time to enter into the stock, if you like its ability to deliver growth and are not highly concentrated in the oil and gas industry. Before you make a decision on the stock, take a look at SOLO’s cash flows and assess whether the stock is trading at a fair price.

For a deeper dive into Solo Oil’s stock, take a look at the company’s latest free analysis report to find out more on its financial health and other fundamentals. Interested in other energy stocks instead? Use our free playform to see my list of over 300 other oil and gas companies trading on the market.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.