Is Franco-Nevada Corporation a Buy?

Precious metals-focused Franco-Nevada Corporation (NYSE: FNV) provides exposure to gold and silver, but does things a little differently from a miner. That difference, however, has big implications for investors. If you are looking to put a little gold and silver into your portfolio, Franco-Nevada could be the perfect option. That's true even though the stock is up around 30% over the past year.

It's no miner

Franco-Nevada is what's known as a streaming and royalty company. That means it provides cash up front to miners for the right to buy silver and gold at reduced rates in the future. To give you an example of this, Franco-Nevada has a streaming deal at the Antapaccay mine, which is owned by commodity giant Glencore. Franco-Nevada paid $500 million up front and gets to buy gold and silver for 20% of the spot price until certain production targets are met and 30% of spot thereafter.

Image source: Getty Images.

Franco-Nevada has locked in low prices no matter what happens to the price of gold and silver. There are expansion opportunities at the mine as well, so the life of the mine and the stream to which Franco-Nevada is entitled could be extended over time. But this is just one deal -- Franco-Nevada has 340 investments, around 80 of which are oil and gas properties that make up roughly 7% of revenue (more on this in a second). These assets run the gamut from producing to development stage.

Slow and steady

When you step back, it's probably best to look at Franco-Nevada as a specialty finance company that gets paid in silver, gold, a small collection of other metals, and oil and natural gas. There are some key takeaways. For example, the company's streaming and royalty model means it never has to get its hands dirty operating the assets in which it invests. It also has wide built-in margins. Miners have to operate their assets, which is no easy task, and commodity downturns can lead to steep drops in margins as miners adjust operations to shifting gold and silver prices.

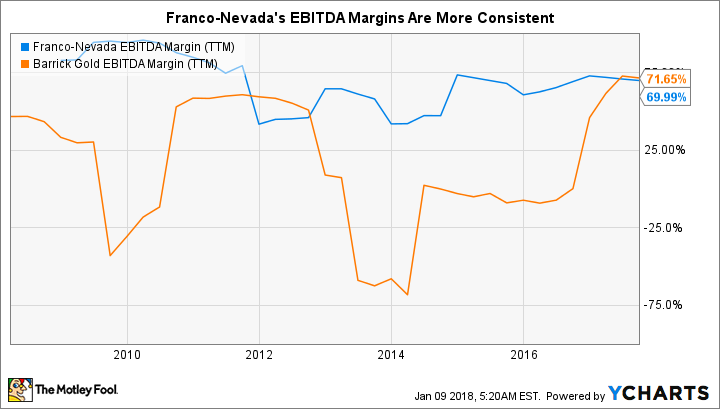

FNV EBITDA margin (TTM) data by YCharts.

Let's put some numbers on that last statement to show how big a deal this is. The chart above compares Franco-Nevada's EBITDA margins over the past decade to those of gold mining giant Barrick Gold (NYSE: ABX). The latter's margins twice fell deep into negative territory over the span while Franco-Nevada's margins remained relatively stable throughout the period. Yes, commodity prices will impact Franco-Nevada's top and bottom lines, but it has a clear edge over miners when it comes to profitability.

With so many investments, Franco-Nevada also provides more diversification than you can get from a miner. A problem at one mine isn't likely to derail Franco-Nevada's business. The oil and natural gas investments, meanwhile, have taken on new importance recently. At first, oil and gas may seem like an odd extension, but the same basic business model (providing cash, not operating assets) has been used to put money to work opportunistically in an out-of-favor sector. That's a positive in my eyes because it increases diversification without materially altering Franco-Nevada's business.

A good run

Diversification and low built-in prices are two key reasons to like Franco-Nevada. It's also increased its dividend every full calendar year since its late 2007 IPO. The yield is a modest 1.1%, but dividend increases will give you something to hold on to when commodity prices are weak. Indeed, despite the differences between Franco-Nevada and miners, gold and silver prices still drive the top and bottom lines. So the dividend will help you stick around to get the full diversification benefit provided by precious metals through the entire commodity cycle.

If you want to add precious metals exposure to your portfolio, I believe Franco-Nevada's streaming model is among the best ways to do it. That remains true even though the stock has had a good run over the past year. Sometimes, it's worth paying more for the better option.

More From The Motley Fool

Reuben Gregg Brewer has no position in any of the stocks mentioned. The Motley Fool has no position in any of the stocks mentioned. The Motley Fool has a disclosure policy.