Former Bear Stearns CEO: Lessons from the financial crisis 10 years later

Alan Schwartz was CEO of Bear Stearns before its acquisition by JPMorgan & Chase in 2008. He is currently the executive chairman of Guggenheim Partners.

He will appear at Yahoo Finance’s All Markets Summit on September 20.

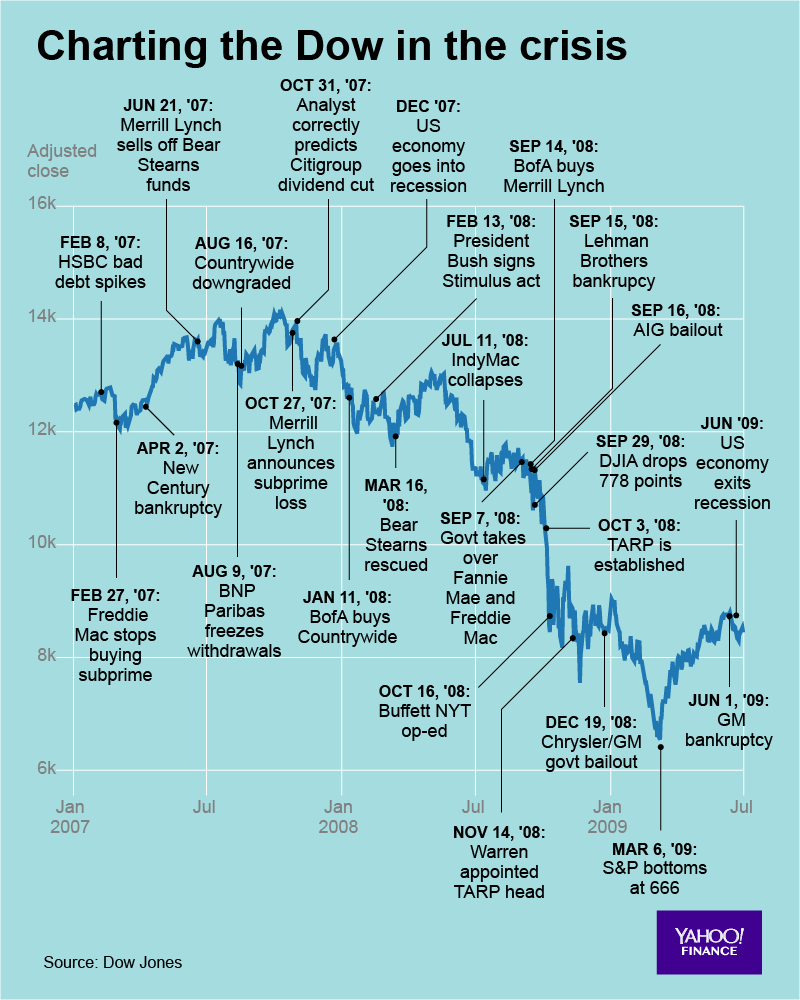

Ten years past the financial crisis, I have been asked often about the most important lessons learned from that period. While it is impossible to isolate any single decision or set of actions that could have prevented the financial crisis, I think it is instructive to understand how that market environment formed and what new variables led to destructive imbalances. That understanding can help us identify today’s burgeoning excesses that may potentially impact tomorrow’s markets.

At Bear Stearns, I worked with an outstanding group of people who built a relatively small firm into the fifth-largest investment bank. But similar to other banks, we became deeply embroiled in the crisis when our risk models, which were primarily based on previous market cycles, failed to account for the devastating impact of untested financial instruments, such as structured mortgage-backed debt.

A fertile environment for an overheated market

In the decades leading up to the financial crisis, the credit environment had changed fundamentally. A broad effort to unlock bank balance sheets and enable the free flow of credit was focused on avoiding another financial spasm like the Savings and Loan Crisis of the 1980s. The elimination of originator liability was expected to be offset by the benefit of the democratization of credit risk. Like most solutions dealing with problems of the past, it could not predict second-order impacts of new variables introduced into the environment.

At the same time, a global savings glut helped fuel the credit markets as investors relied on ratings to park assets into what they perceived as high-quality debt instruments in the form of complex securities. The relationship between the proliferation of debt instruments and rising home prices pushed both to new and unsustainable heights, taking the rate of home ownership to a record 69.2 percent by end of 2004, up from 64.2 percent a decade earlier.

The convergence of new debt instruments, demand for highly rated USD securities, and rising home prices created a fertile environment for an overheated market to develop. Decisions by home buyers, lenders, originators, rating agencies, regulators, traders, and asset managers appeared rational in isolation. But these individual decisions, “velocitized” by rising volumes, created an enormous buildup of aggregate credit exposure.

When the individual loans repackaged into untested mortgage-backed securities started to fail, the lack of transparency into the securities caused a type of “mad cow disease” event. It was difficult to identify which parts of the securities were troubled and which were safe. Investors either had to wait a prolonged period of time — time that many did not have — or eliminate their exposure to the entire category. The resulting liquidity drought in the credit markets, driven by uncertainty in the value of the securities, was debilitating for the financial system.

Although a positive reaction to the financial crisis has been to require more capital on bank balance sheets, the crisis also demonstrated that the Federal Reserve was the ultimate backstop for credit markets. While Bear Stearns held significant capital in the form of high-quality securities in March 2008, few could have predicted the freezing of the repo market, which was a critical source of liquidity for investment banks. The conversion of major investment banks into bank holding companies with access to the Federal Reserve’s discount window demonstrated that our central bank maintains a critical function of providing liquidity at times of severe stress.

A new excess that could test the markets

With 10 years past the Great Recession, are we able to avoid another crisis? In the past cycle, the perception of the housing market transformed from a reliable asset class into a major source of risk. As part of the aftermath of the financial crisis, we witnessed a flight to perceived safety into sovereign government bonds of Europe’s periphery countries, which resulted in an eventual bailout by the ECB in 2011. In the ensuing period, we have seen a continued climb in emerging market corporate debt, which is raising questions given many countries’ exposure to global trade flows.

Looking forward, the massive rise in U.S. government debt could be an underlying factor in the next financial crisis. The data portends a formidable period for the Federal Reserve to fulfill its role as lender of last resort. Despite a baseline forecast of persistent growth, the Congressional Budget Office expects federal debt held by the public to rise from 78 percent of GDP in 2018 to a historic high of 118 percent of GDP in 2038. However, I share a concern with my fellow Managing Partner and Guggenheim Partners Global CIO Scott Minerd about the optimism of that forecast and the likelihood of a recession in the next couple years.

In the event of future economic downturn, perhaps the biggest hangover of the crisis is the public’s loss of confidence in the elites from the corporate and government sectors. This combined with the residual anger at financial institutions will make it more difficult for the U.S. government to manage a future crisis.

Under these conditions, it appears that U.S. government debt is a new excess that has the potential to test the markets. Whether or not public holders — both domestic and foreign — continue to view U.S. government debt as the global benchmark of stability will be a key factor in future financial stability. Whether or not the U.S. can maintain its “exorbitant privilege,” a key benefit of its reserve currency status, could be the key factor in the ability of the U.S. to safely navigate the continued surge in government debt outstanding expected to unfold in the decades ahead.

Read more:

Warren Buffett: Every bubble is built on two words

Hedge fund titan Ray Dalio warns about what’s coming in just 2 or 3 years

Risk-taking in this corner of debt markets sounds a bit too familiar