Column: Answering Biden tax plan, conservatives absurdly claim $400,000 a year isn't 'rich'

In the category of "do we have to do this again?" the financial press and personal finance websites have experienced a recent outbreak of articles asking us to feel sympathy for families barely scraping by on healthy six-figure incomes.

The latest entries ponder whether it's possible to survive financially at $400,000 a year. The reason is that that's the income at which Democratic presidential candidate Joe Biden says he would start tax increases.

Marketwatch.com put the implications most concisely with the headline: "Joe Biden defines income of $400,000 as ‘wealthy,’ but here’s why it’s barely scraping by for some."

I bet a good portion of American households who suddenly find themselves earning $400,000 a year would likely end up with negative cash flow.

Sam Dogen, financialsamurai.com

Aficionados of personal finance writing will recognize these articles as representative of a sizable genre of fiction. The threshold figure varies from piece to piece — sometimes as high as $500,000, sometimes as low as $200,000 — but the theme is always the same: The more you earn, the greater the prospect that you'll land in the poorhouse.

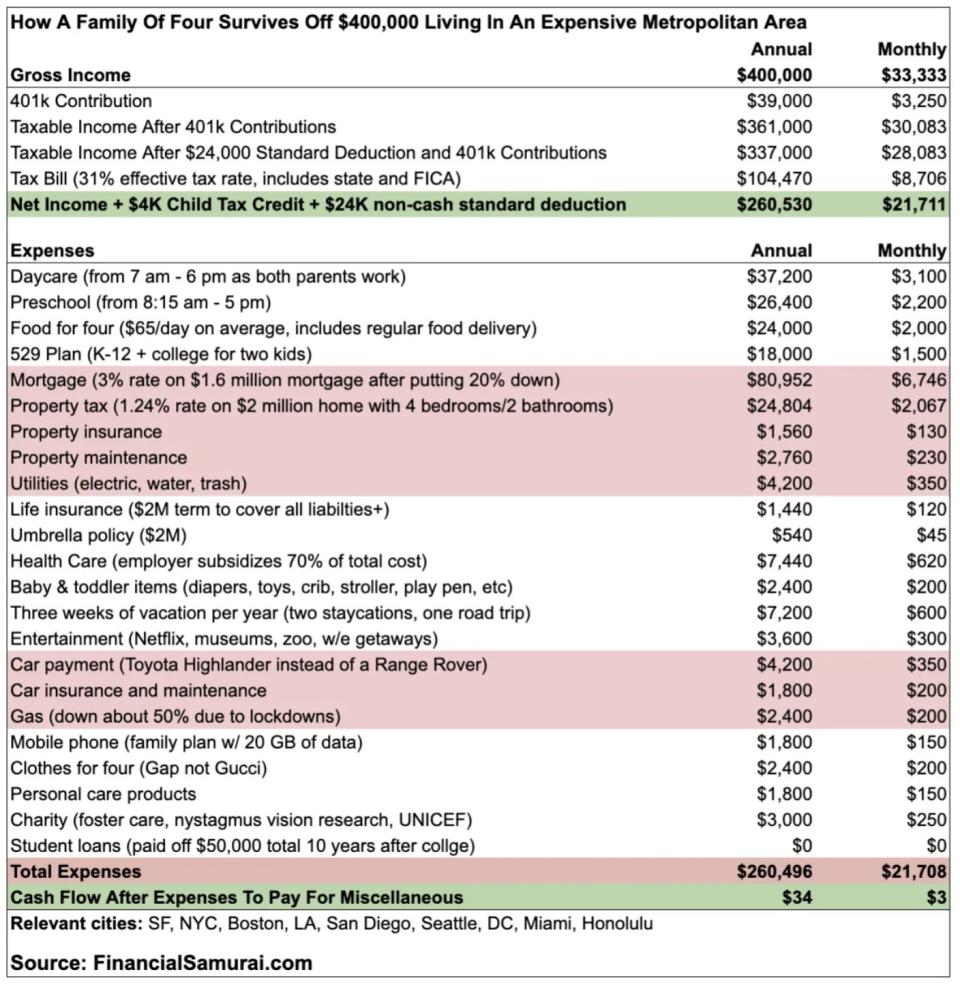

Many of these articles seem to derive from analyses produced by the Financial Samurai website, whose proprietor, Sam Dogen, lives with his family in San Francisco and typically uses the cost of living there or in New York as his baseline estimate of the expenses faced by these putative down-and-outers.

"I bet a good portion of American households who suddenly find themselves earning $400,000 a year would likely end up with negative cash flow," Dogen wrote in response to Biden's tax plan. That's pretty horrifying, given that the median household income in the U.S. last year was $68,703.

The Wall Street Journal has also joined in the fun, having written in 2014 about how "some high earners live paycheck to paycheck."

As we've reported before, these articles invariably depend on sleight-of-hand. They offer their own definitions of "rich" and list as necessary or unavoidable expenses many items that ordinary families would consider luxuries.

Let's take a look at Dogen's latest, which was cited by CNBC and Marketwatch. His bottom line is that his putative $400,000 family — two full-time working parents, two kids — ends up with a shocking $34 at the end of the year "to pay for miscellaneous." Consequently, he asks: "Is $400k really considered rich?"

Dogen defines a rich lifestyle as one that includes driving a luxury car "or two," having a NetJets account for private jet travel at $10,000 an hour, front-row seats to NBA games and a 100-foot yacht "to sail the high seas with mysterious people." No one earning a mere $400,000 a year could afford all that, he says, which one supposes would be true.

Dogen's "middle-class" lifestyle, which he suggests is barely achievable on $400,000, includes owning a three- or four-bedroom home, raising two kids and paying their state college tuition, saving for retirement with a 401k plan or IRA, and going on two to four vacations a year.

Obviously, there's a lot of daylight between these two marks. One can be considered wealthy, even extremely wealthy, even without a NetJets account or front-row seats for the Lakers and a luxury yacht. Similarly, one can maintain a middle-class lifestyle as Dogen defines it on much less than $400,000 a year.

The real legerdemain comes in Dogen's list of expenses. Let's stipulate that a family's necessary expenses are food, shelter and healthcare. Everything else is elective. Even here, however, Dogen places his thumb on the scale by endowing his family with what ordinary families might consider gratuitously lavish, even prodigal, tastes.

Housing? Dogen's family lives in a hypothetical $2-million home. He rationalizes that figure by observing that the median home in San Francisco costs $1.65 million.

"I assure you that $2 million is just a regular home in a larger metropolitan area," he writes, but that's manifestly untrue. In Orange County, California, which is well within the Los Angeles metro area, the median home price is $776,000, according to Realtor.com. For Dogen's hypothetical home, insurance, property tax, maintenance and utilities bring total housing costs to just over $114,000 a year.

Food? Dogen's family spends $65 per day, or nearly $24,000 a year. That's well in excess of what the U.S. Department of Agriculture estimates for its highest-cost "liberal food plan" for a family of four with two pre-teens, which works out to about $16,000, or $43 per day.

Dogen notes that with two full-time working parents, the family must pay for "regular food delivery." Does that jack up food costs by 50%? Doubtful.

Dogen estimates healthcare costs at $7,440 a year, which actually seems a little low, even though the family's coverage is subsidized by their employers.

That covers the necessities. What about the rest?

Dogen lists $39,000 in 401k contributions. That's the maximum permitted for two working spouses, combined. The question here is how many families earning a median income or even a mid-six-figure income could max out their contributions by socking away 10% of their income for retirement.

Most can't. That's why the median retirement savings for households with any retirement account at all is only $60,000. Retirement plans such as 401k plans are relative luxuries; the participation rate in such plans drops sharply with income, not because middle- and lower-income households are imprudent about retirement, but because they don't have the disposable income.

This family spends nearly $64,000 a year on their children's day care and preschool, and save another $18,000 in their 529 college plans. They pay nearly $2,000 a year for life insurance ($2-million policy) and on umbrella liability coverage.

Then there's spending on vacations, an automobile, clothes, charity, entertainment and "personal care products."

No one would suggest that all these expenses are necessarily unwise or morally wrong. What they are is optional, the result of decisions that the couple could have made differently. They could live in a smaller house or trade the city for the suburbs. Put less into their savings, cut their term life insurance to $1 million.

That's why asserting that the family has only $34 left from their $400,000 income is, essentially, a lie. One might better assert that from their after-tax income of $295,530 and after necessary spending on their home, food and health coverage, they have nearly $150,000 left to spend on anything else they choose — retirement and college savings, childcare, vacations, "personal care," what have you.

That $150,000, mind you, is well more than twice what the median American family has to spend on everything. If this family ends the year with $34 at hand, it's because they've put $39,000 in the bank for their retirement and $18,000 in their college funds — they still have that money, which is growing tax-free — and made numerous other expenditures that many average families have to do without.

As we observed in 2017, the motivation underlying these articles is insidious. They strive to show that, in certain cities, $400,000 places them in the same middle-class boat as you or me. They aim to reassure the wealthy that their financial travails are not their own fault — they’re inevitable costs of living, like taxes or funerals.

More to the point, they're designed to make us weep for households that might face a higher tax burden in a Biden administration — after getting an enormous tax break from the Trump administration and its GOP handmaidens. The tax cut, it should be repeated, delivered the biggest bang for the buck to households earning $300,000 or more. They got an average break of more than $13,000 a year.

So should you cry for these hard-pressed earners of $400,000? Obviously not.

This story originally appeared in Los Angeles Times.