Buy General Electric at $6.50 Before It Jumps 150%

After a disappointing summer, General Electric (NYSE:GE) finally looks set to recover. As air travel starts to return, the numbers paint a clear post-pandemic picture: that GE stock is no longer a value trap.

Source: JPstock / Shutterstock.com

Value investors have been waiting for a very long time. GE stock has lagged the S&P 500 by over 20% since June, adding to almost two decades of underperformance since CEO Jack Welch’s retirement in 2001.

Finally, the wait seems to be over. Since joining in late 2018, turnaround CEO Larry Culp has quietly sold off GE’s less profitable businesses. And despite the coronavirus pandemic, here’s why GE has become the most attractive aviation company in my Quantitative Stock Ranker (QSR) list.

InvestorPlace - Stock Market News, Stock Advice & Trading Tips

GE Stock: An Aviation Powerhouse

Jack Welch would barely recognize the slimmed-down GE of today. In March, the company shed its BioPharma segment to Danaher (NYSE:DHR) for $21.4 billion. Then in a stunning move just two months later, the company said “goodbye” to its 129-year-old light bulb business in a sale to Savant Systems, a maker of home automation technology. These moves follow years of dismantling within the former conglomerate.

Today, GE dominates the lucrative jet-engine servicing business (as well as medical imaging devices). And unlike the fractured airline industry, the consolidated jet-engine business earns stunningly high margins: GE’s aviation segment controls 59% of the world’s market and makes a 20% operating margin. That’s because cost-conscious airlines are willing to spend more on fuel-efficient engines, even if they come with pricey service contracts.

Source: Data courtesy of Statista

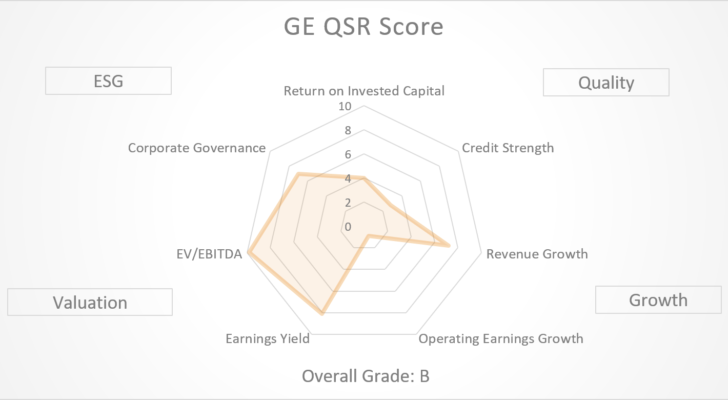

These profits haven’t gone unnoticed in my QSR scoring system. GE now gets an “A” in its “quality-for-growth” score, putting it in the top 10% of all U.S. large-cap companies.

GE’s Return to Pre-Pandemic Growth

It’s not, however, all good news. To create these fortress margins, GE sacrificed one crucial item: growth.

Since peaking in 2007, GE’s EBITDA has shrunk by 81% as it spun off assets. Profits in aviation, its crown jewel, sank 89% in H1 2020 as aircraft usage tumbled. Today, GE’s QSR Growth score sits at an anemic “C+,” pulling down its overall QSR grade to a “B.”

Source: Data courtesy of Gurufocus

So, what would raise GE’s scores? A return to growth.

While the International Air Transport Association (IATA), an international airline trade association, estimates that airline demand won’t return to normal until 2024, July and August have seen some improvements. By the end of August, domestic air travel in China reportedly returned to 98% of last year’s levels, while the U.S. returned to 42%.

Source: Data courtesy of TSA

These numbers come as welcome news to GE’s bottom line. Analysts now estimate GE’s EBITDA to rise from $4.15 billion in 2020 to $13.7 billion by 2024 as jet engines reenter service. Such an increase (after years of falling EBITDA) would raise GE’s QSR Growth score to a “B+,” pushing its overall score to an “A.”

That makes GE the top-scoring company in the U.S. aviation industry.

Southwest: D-

American: F

Delta: F

United: F

Boeing: F

What Can Go Wrong? GE Capital

GE’s balance sheet might remain a cause for concern. The company receives a “C” grade for financial strength, despite having $41.4 billion in liquidity.

Why? That’s because GE Capital, GE’s financing arm, remains a dark horse.

GE has long struggled with its legacy capital business, despite spinning off its long-term care and mortgage insurance segments in 2004. In 2018, Bank of America claimed GE Capital had “zero equity value.” It warned that the company could lose billions in lawsuits.

GE’s management has moved to shore up the company’s balance sheet. In 2018, GE Capital had a 5.7:1 D/E ratio. By 2020, that figure had shrunk to a more manageable 4.2:1.

It’s still far from perfect; AerCap Holdings, the largest aircraft leasing company globally, has an even lower 3.7:1 ratio. And last Thursday, rival Rolls Royce (OTCMKTS:RYCEY) reported a record 5.4 billion pound loss and warned of potential bankruptcy (signaling possible turbulence in the jet engine industry). But these moves should be enough to help GE survive until air travel returns. In April, Moody’s, a bond rating service, reaffirmed its investment-grade Baa1 rating.

Source: Data courtesy of Gurufocus

Will GE Stock Rocket Back?

The QSR scores have been quick to spot GE’s comeback. Over 60% of the firm’s revenues now come from its high-margin aviation and medical businesses. Its loss-making renewable energy segment has recently scored some notable contract wins.

Analysts estimate that GE will generate over $99 billion revenue and $13.7 billion EBITDA by 2024. Putting these numbers into a two-stage discounted cash flow (DCF) model shows GE has a fair value of $16.5, a 152% upside to current prices.

Source: Data courtesy of Finbox.com

There’s a good chance GE will finally meet these expectations as years of turnaround start to pay off.

As we head into 2021, investors looking to play into the airline recovery story should strongly consider GE stock, an undervalued diamond in the rough.

Tom Yeung, CFA, is a registered investment advisor on a mission to bring simplicity to the world of investing. On the date of publication, Tom Yeung did not have (either directly or indirectly) any positions in the securities mentioned in this article.

More From InvestorPlace

The post Buy General Electric at $6.50 Before It Jumps 150% appeared first on InvestorPlace.