Is Brookfield Business Partners LP.’s (TSE:BBU.UN) Balance Sheet Strong Enough To Weather A Storm?

Small-caps and large-caps are wildly popular among investors; however, mid-cap stocks, such as Brookfield Business Partners LP. (TSX:BBU.UN) with a market-capitalization of CA$5.94B, rarely draw their attention. However, generally ignored mid-caps have historically delivered better risk adjusted returns than both of those groups. BBU.UN’s financial liquidity and debt position will be analysed in this article, to get an idea of whether the company can fund opportunities for strategic growth and maintain strength through economic downturns. Note that this commentary is very high-level and solely focused on financial health, so I suggest you dig deeper yourself into BBU.UN here. See our latest analysis for Brookfield Business Partners

Does BBU.UN generate enough cash through operations?

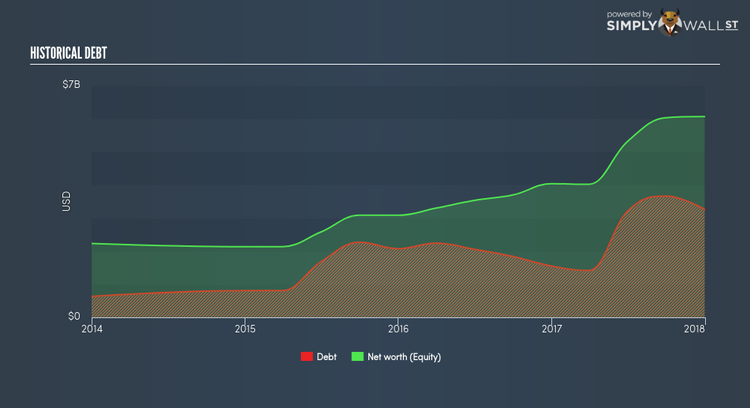

BBU.UN has built up its total debt levels in the last twelve months, from US$1.55B to US$3.27B – this includes both the current and long-term debt. With this growth in debt, the current cash and short-term investment levels stands at US$1.11B , ready to deploy into the business. Moving onto cash from operations, its small level of operating cash flow means calculating cash-to-debt wouldn’t be too useful, though these low levels of cash means that operational efficiency is worth a look. For this article’s sake, I won’t be looking at this today, but you can take a look at some of BBU.UN’s operating efficiency ratios such as ROA here.

Can BBU.UN meet its short-term obligations with the cash in hand?

With current liabilities at US$5.64B, the company has been able to meet these obligations given the level of current assets of US$7.06B, with a current ratio of 1.25x. Usually, for Construction companies, this is a suitable ratio since there is a bit of a cash buffer without leaving too much capital in a low-return environment.

Does BBU.UN face the risk of succumbing to its debt-load?

With debt reaching 53.84% of equity, BBU.UN may be thought of as relatively highly levered. This is not unusual for mid-caps as debt tends to be a cheaper and faster source of funding for some businesses. Though, since BBU.UN is currently unprofitable, sustainability of its current state of operations becomes a concern. Running high debt, while not yet making money, can be risky in unexpected downturns as liquidity may dry up, making it hard to operate.

Next Steps:

BBU.UN’s cash flow coverage indicates it could improve its operating efficiency in order to meet demand for debt repayments should unforeseen events arise. However, the company exhibits proper management of current assets and upcoming liabilities. Keep in mind I haven’t considered other factors such as how BBU.UN has been performing in the past. I suggest you continue to research Brookfield Business Partners to get a more holistic view of the stock by looking at:

Valuation: What is BBU.UN worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether BBU.UN is currently mispriced by the market.

Historical Performance: What has BBU.UN’s returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.