A2Z Infra Engineering Limited (NSE:A2ZINFRA): Time For A Financial Health Check

Investors are always looking for growth in small-cap stocks like A2Z Infra Engineering Limited (NSEI:A2ZINFRA), with a market cap of ₹4.54B. However, an important fact which most ignore is: how financially healthy is the business? Given that A2ZINFRA is not presently profitable, it’s crucial to understand the current state of its operations and pathway to profitability. I believe these basic checks tell most of the story you need to know. Though, given that I have not delve into the company-specifics, I recommend you dig deeper yourself into A2ZINFRA here.

Does A2ZINFRA generate an acceptable amount of cash through operations?

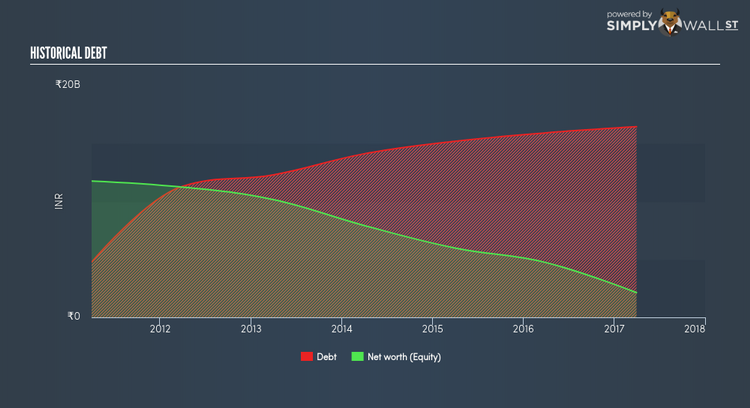

A2ZINFRA’s debt level has been constant at around ₹16.45B over the previous year – this includes both the current and long-term debt. At this current level of debt, A2ZINFRA’s cash and short-term investments stands at ₹750.33M for investing into the business. Additionally, A2ZINFRA has generated ₹670.65M in operating cash flow in the last twelve months, leading to an operating cash to total debt ratio of 4.08%, signalling that A2ZINFRA’s operating cash is not sufficient to cover its debt. This ratio can also be interpreted as a measure of efficiency for unprofitable companies since metrics such as return on asset (ROA) requires a positive net income. In A2ZINFRA’s case, it is able to generate 0.041x cash from its debt capital.

Can A2ZINFRA meet its short-term obligations with the cash in hand?

Looking at A2ZINFRA’s most recent ₹23.94B liabilities, it seems that the business has not been able to meet these commitments with a current assets level of ₹22.45B, leading to a 0.94x current account ratio. which is under the appropriate industry ratio of 3x.

Is A2ZINFRA’s debt level acceptable?

A2ZINFRA is a highly-leveraged company with debt exceeding equity by over 100%. This is not unusual for small-caps as debt tends to be a cheaper and faster source of funding for some businesses. Though, since A2ZINFRA is currently loss-making, there’s a question of sustainability of its current operations. Running high debt, while not yet making money, can be risky in unexpected downturns as liquidity may dry up, making it hard to operate.

Next Steps:

A2ZINFRA’s high debt level indicates room for improvement. Furthermore, its cash flow coverage of less than a quarter of debt means that operating efficiency could also be an issue. In addition to this, its lack of liquidity raises questions over current asset management practices for the small-cap. I admit this is a fairly basic analysis for A2ZINFRA’s financial health. Other important fundamentals need to be considered alongside. You should continue to research A2Z Infra Engineering to get a more holistic view of the stock by looking at:

1. Historical Performance: What has A2ZINFRA’s returns been like over the past? Go into more detail in the past track record analysis and take a look at the free visual representations of our analysis for more clarity.

2. Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.