These 3 Chip Giants Keep Hitting New Highs: Are They Still Buys?

The semiconductor industry is turning around. It’s no secret that chip stocks lost heavily in 2H18, and had difficulty regaining traction through much of 2019. But in recent months, many of the big chip makers have seen sharp gains.

While individual companies will show idiosyncratic reasons for gains, the sector as a whole has been positively impacted by three major factors starting in 2H19. First, and probably most important, is the continuing expansion of 5G mobile networks. The wireless switchover requires new types of modem chips to handle the new signal bands, and chipmakers are seeing increased orders from the original equipment manufacturers (OEMs). Wireless handsets, routers, modems, transmitters, towers – all of these will need the new chips.

The next main factor is continued demand for memory chips. Data centers are expanding, meeting an urgent need in the digital economy, and the chip makers are seeing orders for new, more powerful, memory and processing chips. Those same chips are also finding customers in the online gaming community. The memory and processing requirements for business and gaming applications frequently overlap, and gamers are notorious for wanting the best systems they can afford.

Finally, on the geopolitical front, the US and Chinese governments signed off on the Phase 1 agreement of a trade deal, an important development that promises to defuse the long-running trade and tariff disputes between the world’s two largest economies. Chip makers were exposed to the ‘trade war’ on multiple fronts – as exporters from both the US and China, as suppliers of parts to reexported Chinese electronic goods, and as components in goods imported to the US. Reduced trade tensions in 2020 promises to boost the chip industry.

So, we should expect to see several interesting points among the major chip stocks. They are likely to carry Buy ratings, on mixed reviews from analysts; they are likely to show modest upside, as the analysts have not yet adjusted their outlooks; and they are likely to have recent strong reviews. We’ve pulled up the data on three of the larger chip stocks, and looked at them through the TipRanks Stock Comparison tool. Here are the results.

Advanced Micro Devices (AMD)

AMD, the first stock on our chip list, has gained 43% in the past three months. The company is a leader in both the graphics processors and motherboard chipset segments, and its x86 microprocessors are major competitors to industry giant Intel. AMD can boast that strong sales are fueling growing revenues, despite lower guidance for Q1 2020.

Did the lower forward guidance really merit a 4% share price drop at the end of January? We can get an idea by looking at the Q4 numbers. AMD reported EPS at 32 cents against a 31-cent forecast. Revenue was $2.13 billion, beating expectations, growing 18% sequentially, and showing an impressive 50% gain year-over-year. For fiscal 2019, total revenue grew $6.73 billion, or 4%.

So, Q4 was strong. Looking ahead, the company guided for $1.8 billion in Q1 revenue (matching Q3 results) against an expectation of … $1.86. That 3% difference was it. And AMD shares have, since the earnings report, regained the 4% loss.

One measure of AMD’s strength comes from Mitch Steves, a 5-star analyst with RBC Capital. Steves released two notes on the stock last week – and he raised his price target in both. In the first, on February 10, he bumped his target from $53 to $64, writing, “We raise our 2021 EPS estimate to $2.10 as we think share gains in PCs will continue to move into the mid-20 percent market share range and we have higher conviction in server units in both 2020 and 2021.”

In the second note, on February 13, Steves revised his opinion after Nvidia (more below) released strong quarterly results. Nvidia’s results imply a healthy gaming sector, and AMD is well-positioned to capitalize on gaming sales. Steves’ current price target on AMD, backing his buy rating, is $66, implying an upside of 19%. (To watch Steve’s track record, click here)

AMD’s recent sharp gains have pushed the stock’s share price well above the average price target, and analysts have not yet readjusted their outlook. As Steves’ double target upgrade show, events in the chip industry are moving quickly. AMD’s Moderate Buy consensus rating is based on mixed reviews, and includes 11 Buy and 13 Holds. (See AMD stock analysis at TipRanks)

Nvidia Corporation (NVDA)

In an interconnected sector like semiconductor chips, nothing happens in a vacuum. We mentioned Nvidia above, in relation to gaming chips. This company is a market leader in graphics processing units (GPUs), a key component in both professional and gaming computing systems. The memory and performance requirements of the graphic design industry run parallel to those of high-end gamers. Nvidia’s expertise with high performance memory chips has also made its products valuable in the data center market.

With its foundations firm in several markets – professional designers, data centers, and gamers – Nvidia has built up a $186 billion market cap and an annual sales base near $12 billion. With that strong base, NVDA reported both earnings and revenue beats in Q4 2019.

On the top line, revenue came in at $3.11 billion, up 3% sequentially, an impressive 41% year-over-year, and beating the forecast by 5%. EPS was reported at $1.89, a solid 14% over the estimate – and an eye-popping 136% year-over-year gain. The GPU segment rose 40% annually, and gaming revenues were up 56%. Nvidia’s data center business showed a 33% sequential gain and a 43% annual gain. It was good news all around, even for a stock that has seen 42% growth in the last three months, on top of 76% gains in calendar 2019.

Nvidia’s strong quarter impressed Cowen analyst Matt Ramsay. Ramsay, who rates 5-stars by TipRanks and is ranked #37 overall in the analyst database, reiterated his Buy rating for Nvidia and raised his price target on the stock by 35%, to $325. His new price target implies an upside potential to the stock of 12%.

In his note on NVDA, Ramsay wrote, “[We] believe the results and guidance are driven by a cloud CapEx recovery and the driving force of real-time conversational AI with the scaled ramp of Ampers still to come.” (To watch Ramsay’s track record, click here)

All in all, NVDA shares hold a Strong Buy rating from the analyst consensus, based on 23 Buys and 6 Holds given in recent weeks. Shares are not cheap, selling for $289.79. The average price target is $308.85 which suggests room for a modest upside of nearly 7%. (See Nvidia stock analysis at TipRanks)

Micron Technology (MU)

Last on our chip list Micron, the chip industry’s fifth largest player by sales volume, with over $30 billion in annual sales. The company saw its supply chains – both for manufacturing components and finished products – highly impacted by the US-China trade dispute, but the recent Phase 1 agreement relieved that pressure. Micron compensated by lowering guidance on fiscal Q1, and now the results are in.

Micron cleared the lower bar. EPS met the estimates, while revenues beat. The top line number was $5.144 billion for the quarter, 2.3% over the forecast – but, down 35% year-over-year. The annualized drop reflects the lower demand and higher costs in 2019, due to industry pressures related above. EPS, at 48 cents, was as expected, but also showed a steep yoy decline. Still Micron met the analysts' expectations for the quarter, investors were satisfied, and the stock is up 7.2% since the earnings release.

Micron’s position leading the DRAM chip segment gives the company a clear path to profit from the 5G switchover as the new networks expand nation- and worldwide. And, as with Nvidia and AMD, Micron boasts profitable business in the gaming and data center markets. The company’s diverse customer base should allow it to weather a period of lower earnings, while it adjusts to the new market’s new demands.

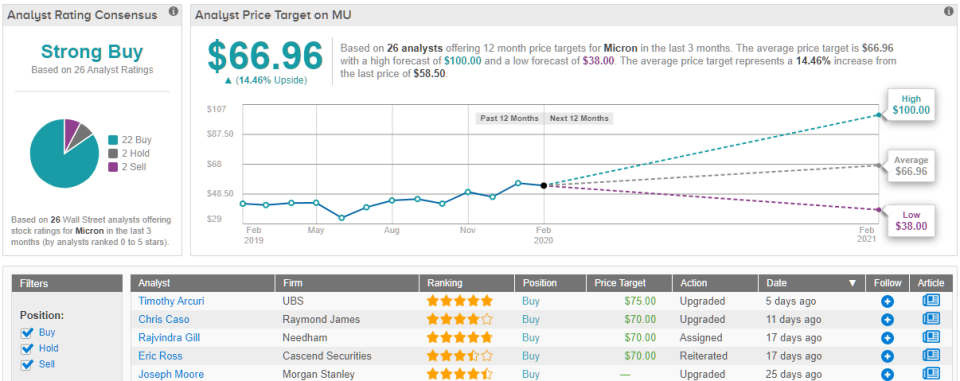

In the last few days, MU shares have received two upgrades from Wall Street analysts. The first, on February 6, came from 4-star analyst Chris Caso of Raymond James. Caso sees the demand for DRAM memory chips as “likely to improve further at the year progresses.”

With that in mind, Caso raised his outlook on the stock from Neutral to Buy and set a $70 price target. Caso’s target implies an upside of 19% to MU shares. (To watch Caso’s track record, click here.)

The second upgrade came on February 16, from Timothy Arcuri, 5-star analyst with UBS. Arcuri also raised his outlook from Neutral to Buy, and went further with the price target. He bumped that up by 59%, from $47 to $75. The new price target indicates real confidence in the stock, along with a robust 28% upside potential.

Supporting his upgrade, Arcuri writes, “After only modestly outperforming the S&P 500 over the past two years, we believe the time has finally come when Micron can materially outperform over a sustained period of time… Micron is in a much stronger position in a structurally better industry on the cusp of a cyclical upswing that, for DRAM, should last deep into C2021.” (To watch Arcuri’s track record, click here)

Micron shares are selling for $58.50, and the average price target of $66.96 suggests that there is room for a 14% upside to the stock. The Strong Buy analyst consensus rating is based on no fewer than 22 Buys, against just 2 Holds and 2 Sells. (See Micron stock analysis at TipRanks)