College students are stressing out over finances and making “costly missteps,” according to a new survey by AIG Retirement Services and EVERFI.

The survey — which looked at responses from 30,000 students from more than 440 institutions in 45 states, out of which 80% were from Gen Z (i.e. born after 1996) — revealed some sobering statistics.

“College students cited several significant financial worries, including whether they would have enough money to last the semester (52%), fear of tuition rising (59%) and the most prevalent worry – landing a job after graduation (68%),” the report found.

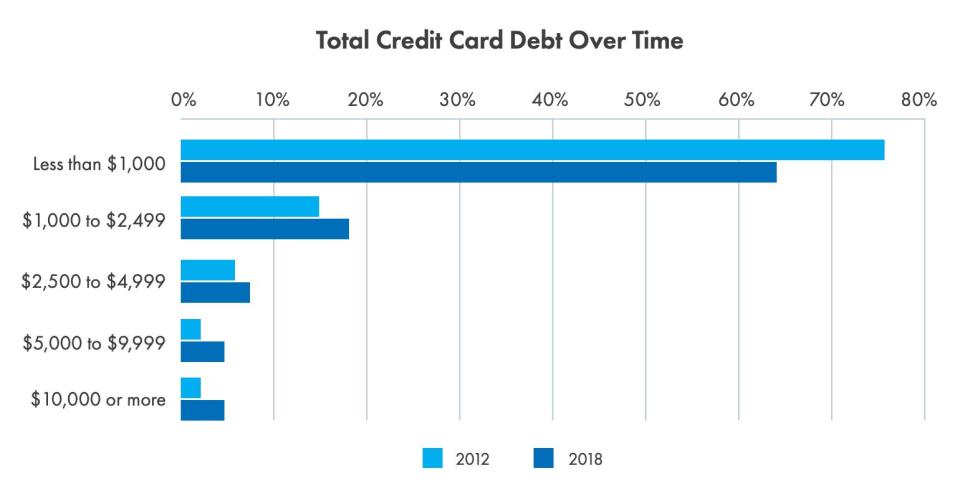

Furthermore, 65% of student loan borrowers planned to pay off their debt on time, more than one in three students have already amassed more than $1,000 in credit card debt, and 40% said they aren’t likely to pay their credit card bills on time.

‘The debt issue is real, the drivers are real’

"It's easy to look at all that data, and kind of feel a little bit depressed about it," AIG Retirement Services President Robert Scheinerman told Yahoo Finance. As "an outside observer,” he said he felt “a lot of empathy for the people who are in that debt situation.”

He added: “People are doing a good job getting prepared for academics and for school. But they're struggling with what it takes to finance school, what the obligation they're going to be, and what the implications are borrowing after they graduate,” said Scheinerman. "The equation seems to have changed… [and] the debt issue is real, the drivers are real."

Nearly half of college students also said they “do not feel prepared to manage their money,” according to the report, and there was also a “sharp decline in students who expect to adopt good financial habits over the next 12 months.”

This included things like following a budget — which is down from 76% in 2012 to 49% in 2019 — and paying bills on time, which fell from 85% in 2012 to 60% today.

Student loan stress

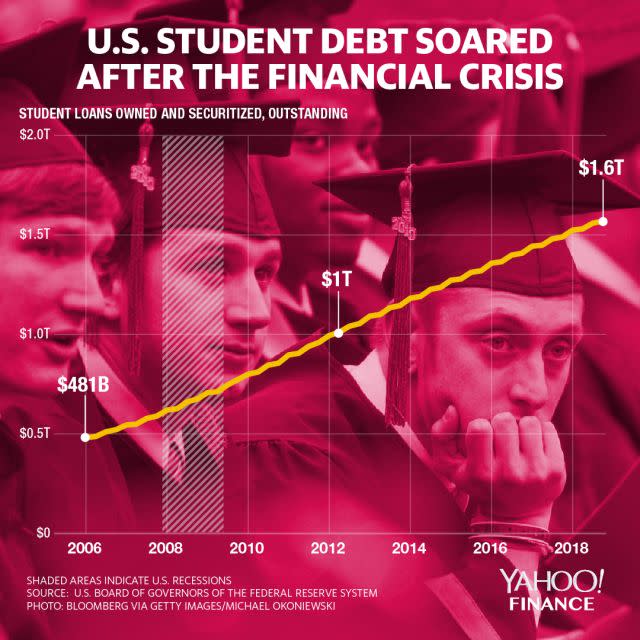

There are currently about $1.6 trillion in outstanding student loans, and borrowers are increasingly missing payments.

Increasing delinquencies are hurting borrowers materially, as they fall behind on major life milestones like buying a house or getting married.

Borrowers in the South (i.e., south of the Mason-Dixon line and east of the Mississippi River) are facing even more stress with high levels of debt, coupled with relatively low earnings.

More than half of the survey respondents indicated that student debt worried them. And more tellingly, only 65% of borrowers “plan to pay off their loans on time and the same percentage plan to pay them off in full, down dramatically from 88 percent in 2012.”

Easy money, bleak future

At the same time, college students were also adopting “risky credit card habits,” according to the new report, as they take on more and more debt while missing payment deadlines.

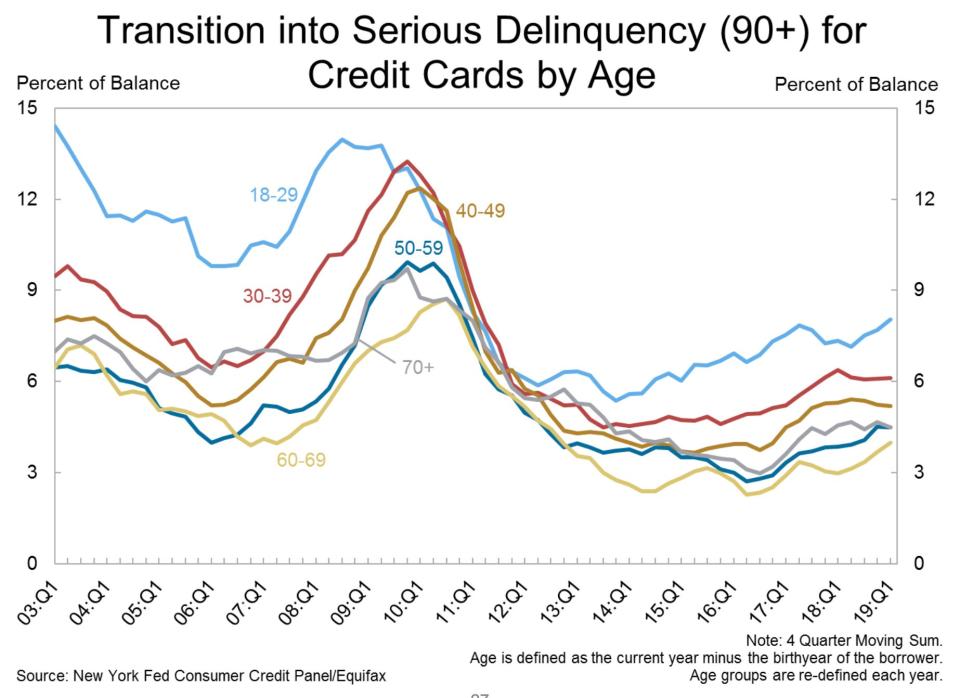

Just like student loan delinquencies, rates for credit cards are also increasing quickly, but the 18 to 29 demographic in particular was leading the upward trend.

Credit is becoming more easily available to college students, the survey found, with the use of credit cards on college campuses growing from 28% in 2012 to 46% today.

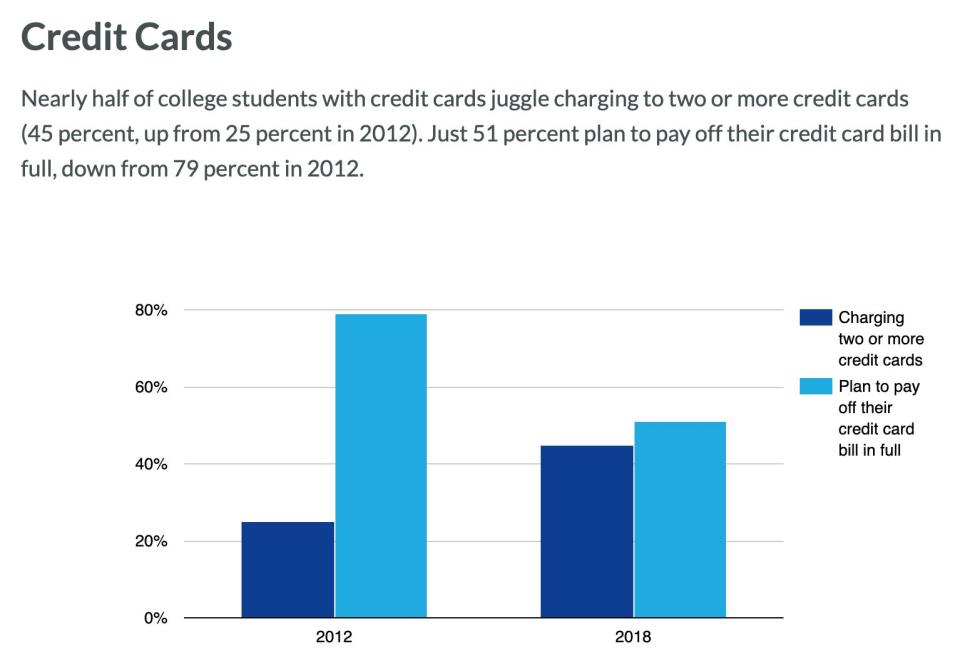

Additionally, “nearly half of these students juggle charging to two or more credit cards,” the survey stated, which is up from 25% in 2012 to 45% today.

It doesn’t end there — more than one in three students with these credit cards have “amassed more than $1,000 in credit card debt,” which shows “a significant uptick since the survey began.”

Yet, only half say they would pay that credit card bill off entirely the following year.

But one in five have already damaged their credit scores with late payments. And again, with only 60% committing to paying their bills on time, 40% are left to feel more pain.

Unsurprisingly, banks are seeing more and more borrowers miss their payment deadlines by more than 90 days, pushing themselves into serious delinquency.

And the net charge-offs for credit card debt — which refer to the loans removed from the balance sheet because it was uncollectible — increased by $543.4 million over the last year, the largest such dollar increase relative to other loan categories, according to the Federal Deposit Insurance Corporation.

Large lenders like Capital One and Discover have subsequently tightened credit limits.

Retirement planning is ‘frustrating’ for Gen Z

And when it came down to retirement, it was no surprise that Scheinerman saw "people who are stressed out.”

He noted that “the likelihood of people living to age 100 is going up,” he explained. “So you have to plan for a long retirement, and then they've got these student loans, but in some cases, very large that slowing me down. It is frustrating."

He suggested two options for college students.

The first was to provide an on-site financial advisor for the students to help them plan for their future.

The other solution was for employers to put together a new type of benefit that helped student debt-laden employees to pay off their loans and save for retirement, which is already in motion on Capitol Hill.

Scheinerman referenced a bill called the “Retirement Parity for Student Loans Act,” which was introduced in Congress by Senator Ron Wyden (D-OR) in December. The bill would allow “certain employer-sponsored retirement plans to make matching contributions for an employee's student loan payments as if the loan payments were salary reduction contributions to the retirement plan.”

That bill would "give a safe harbor to employers to connect savings tools between their 401k or for 403b or other retirement plans and student loan payments,” Scheinerman said, adding that “that's not something that's easy to do today, because the rules don't allow it.”

“It's positive that we see policymakers starting to recognize his problem starting to think about ways to do something about this problem is a good start.” Scheinerman said, with a caveat: “The devil’s in the details, [and] we want to know and see exactly what something is.”

—

Aarthi is a writer for Yahoo Finance. Follow her on Twitter @aarthiswami.

Read more:

Household debt hits $13.6 trillion as student loan and credit card delinquencies rise

Elizabeth Warren unveils 'broad cancellation plan' for student debt

'The clock is ticking' on U.S. consumer loans — and that could mean a slowdown, Deutsche Bank warns

Read the latest financial and business news from Yahoo Finance

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.