Open enrollment for 2018 marketplace has begun: 6 changes you can expect

Have questions about open enrollment on the ACA health insurance marketplace? We’re here to help. Submit your questions to MONEYQUESTIONS@YAHOO.COM and they may be answered by our experts in an upcoming Yahoo Finance Facebook Live Chat Tuesday, December 5th, 2017 at 2PM EST.

There’s a great deal of uncertainty surrounding the Affordable Care Act, aka Obamacare, as the Trump administration and Congress go back and forth on repealing and replacing the health care law. Like many confused Americans, you might be wondering if you can still enroll for 2018 coverage.

The answer is yes! Open enrollment officially begins today. Here are six key changes to expect as you shop for coverage.

Pricier premiums

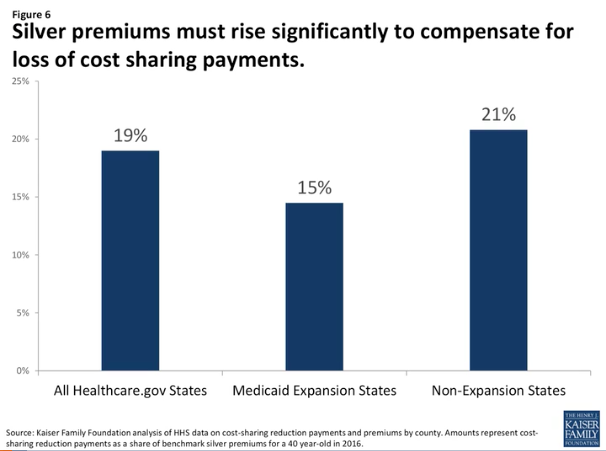

You can expect premiums to go up by 15% to 21%, depending on whether or not your state has expanded Medicaid, according to a cost analysis by the Kaiser Family Foundation. The rise is largely due to the discontinuation of cost-sharing reimbursements, or CSRs. In years past, the government issued CSRs to insurance companies to help reduce costs for consumers. But in the past month, as the Trump administration has ended these cost-sharing subsidies, insurers have raised their premiums to make up for it.

There is, however, good news for low-income enrollees as insurance companies are still required by law to provide lower deductibles and copays for benchmark silver plans (one of 4 categories of the Health Insurance Marketplace) to those who earn incomes up to 250% of the poverty level. You may be eligible for these subsidies if you’re single earning between $12,060 and $30,150 in 2018; for a family of four, your household income must be $24,600 to $61,500. In 2017, 57% of the marketplace enrollees were eligible for these cost-sharing reductions.

Find out what savings you’re qualified to receive on healthcare.gov and using an interactive marketplace calculator, get an estimate of what your plan could cost you, including any premium tax credits and subsidies you may be eligible for.

Subsidies shield increases for the majority of enrollees

Even if premiums have gone up, close to nine million enrollees will be shielded by subsidies. For example, a single 30-year-old earning $24,000 in California may only have to pay $3 more in 2018 for a silver plan that costs $47 more than it did in 2017, according to the Kaiser Family Foundation.

If you’re not eligible for subsidies, check your state for options to keep your plan affordable for your family.

You have half the amount of time to sign up for health care

Enroll now, because this year you have a lot less time to get it together. To sign up for coverage that takes effect January 1, 2018, you have between November 1st and December 15th to enroll—that’s six weeks less than in prior years.

Keep in mind that toward the end of the enrollment period, health care navigators will be swamped helping last-minute enrollees, so get ahead by acting early, especially if you need in-person assistance to enroll. You might also run into some technical glitches if you wait to the last minute as the site will likely be bogged down by heavy traffic.

Anticipate changes in the marketplace and shop around

Shopping around will save you money. If you already have marketplace coverage, automatic renewal is still an option, but it’s not recommended. With all the changes to the marketplace, your insurer may have dropped out, your subsidy allowance could’ve changed, and if you don’t take action by December 15, you might not like the plan that you’ve been re-assigned to.

And unlike previous years, you won’t have the chance to change your plan in January if you don’t like the one that you’re automatically enrolled placed in. So log into your account on healthcare.gov and explore all your options. But note that every Sunday from noon to midnight, the federal site will be closed for scheduled maintenance. But many states have their own health insurance exchange, so check your state-specific marketplace to enroll.

New rules that allow insurers to deny your coverage

There are a couple of new rules that rolled out this year under the Marketplace Stabilization Regulation by the Department of Health and Human Services.

First, insurers are allowed to refuse your coverage for 2018 if you owe them money. To avoid this, settle up before the enrollment deadline or consider coverage from a different insurer. If you want to dispute that you owe back payments, there isn’t an established appeals process so it’s best to reach out to a trained health care navigator from your state to find out what steps you can take.

The second rule is called “Failure to Reconcile.” This means that if you’re behind on your taxes, you could be denied the premium tax credit. In other words, if you received a premium tax credit in 2016, but you haven’t filed your 2016 tax return, you could be denied the premium tax credit for 2018.

To be in compliance, fill out tax reconciliation form 8962, which is what the IRS uses to reconcile your actual 2016 income with how you estimated the income your tax credit was based on.

Finally, it’s on YOU to spread the word

Funding for outreach and advertising has been cut by up to 90%. So it’s no wonder that only 5% of those uninsured know the deadline to enroll. With the shortened enrollment period, providing consistent reminders about key dates and information will be critical, says Jennifer Tolbert, Kaiser’s director of state health reform. But it will prove to be more difficult with fewer outreach events and in-person appointments with trained marketplace assisters. All the more reason to jump on this now by going to localhelp.healthcare.gov and typing in your zip code.

Remember, you are required to have coverage—or pay the penalty for going without. The tax penalty for not having health insurance in 2018 is the same as 2017’s: the greater of $695 or 2.5% of your household income, with a maximum limit of $2,085. Payment must be made when you file your federal income tax return.

Have any other questions? Reach out to me on Twitter and stay tuned for more updates right here on Yahoo Finance.

Jeanie is a senior producer and reporter at Yahoo Finance. Watch more from Jeanie here and follow her on Twitter @jeanie531.