Funeral directors Dignity shed 109p to reach 570p on Friday in its biggest slump since March 12 after the competition watchdog said it had “serious concerns” about the funeral sector. Its stock is down 2.7pc so far this year.

In a final report following an investigation, the Competition and Markets Authority (CMA) said it would continue to monitor funeral service providers to ensure consumers are fairly treated and decide whether further investigation is needed.

It said the sector must be more transparent on prices, and recommended the Government set up independent inspections and a registration service.

In 2018 the watchdog said the cost of arranging a funeral had risen more than two thirds in the previous decade, and almost three times the rate of inflation.

Some smaller funeral directors sought to keep prices low, but it said others – mainly larger chains – consistently pushed higher annual price increases.

Dignity said it welcomed the report, adding that there was evidence perceived excess returns have declined since the review period expired two years ago.

Peel Hunt analyst Charles Hall wrote in a note that while the CMA’s comments were expected, they were “an important reminder that this issue is not going away”.

The bank recommends to hold the stock, saying it is clear the CMA would have proposed price regulation if the pandemic had not taken place.

Elsewhere, FTSE 250 shopping centre owner Hammerson said it was seeking a secondary listing in Dublin, to begin trading as soon as next week, to maintain a foothold with EU investors after the UK’s Brexit transition period ends.

Hammerson, which owns Birmingham’s Bullring shopping centre, is not raising any new funds or issuing new shares with relation to the admissions.

The move follows a similar step by warehouse group Segro last month, when it debuted a secondary listing in Paris alongside London. Hammerson’s stock shed 0.2p to 25.84p.

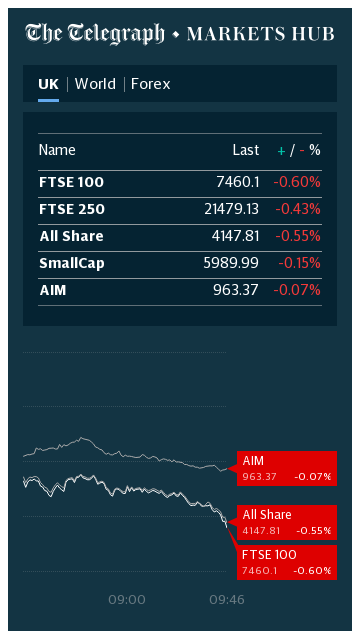

Wider markets ended the week with lacklustre momentum as a EU-UK trade deal edges closer, alongside US stimulus talks, but with no final conclusion.

The FTSE 100 edged down 21.88 to 6,529.18. It fell just 0.2pc compared to last Friday’s close.

Bunzl was one of the top risers after Stifel analyst Samuel Dindol raised the packaging group rating to “buy” from “hold”, setting a target price of £27. He said the current price offered an “attractive entry point” for the group, which was “well-hedged whichever path the pandemic takes”.

Its shares gained 65p to £24.50, while fellow packaging groups DS Smith and Smurfit Kappa also rose.

Meanwhile, Flutter Entertainment – a key drag – fell 590p to £149 after the owner of Paddy Power was hit with an $870m (£644m) judgment by Kentucky’s supreme court.

On Thursday night, the court reinstated an award of damages against US gambling firm The Stars Group that Flutter merged with earlier this year, in relation to offshore poker sites TSG operated. The ruling had originally been vacated in 2015.

Markets Hub embed test

05:19 PM

Wrapping up

That's all from us this week - thank you, as ever, for joining.

Shares of Tesla gained almost 2pc to $668 by midday in New York ahead of the electric car maker's much-anticipated entrance into the benchmark S&P 500 index.

Elon Musk's company will become the most valuable company ever admitted to Wall Street's main index, accounting for over 1pc. Its shares have surged over 60pc since mid-November when its debut in the S&P 500 was announced.

It has surged 700pc year to date, putting its stock market value at over $600 billion and making it the sixth most valuable publicly listed U.S. company, with many investors viewing it as wildly overvalued.

Turnover in Tesla shares hit about $13 billion about half an hour into Friday’s session, with trading volume topping 19 million, according to Refintiv data.

04:49 PM

Next and US investor in talks to buy Arcadia - Sky

Philip Green

Next is in talks with a prominent US investment firm - Davidson Kempner Capital Management - about a joint bid to takeover Sir Philip Green's Arcadia, according to Sky News.

It said the two parties are holding "detailed discussions" about a combined offer for the high street empire which collapsed into administration last month.

Sky reported sources as saying the two companies were "likely, but not certain" to bid for Arcadia ahead of a revised deadline next Monday.

Under the plans, Davidson Kempner would provide the majority of the required funding and probably own the majority of Arcadia.

A sale process is being run by Deloitte has also drawn interest from bidders including Mike Ashley's Frasers Group and online fashion giant Boohoo Group.

04:22 PM

Hammerson to seek secondary listing in Dublin

Bullring

Shopping center owner Hammerson said it is seeking a secondary listing on Dublin Euronext stock market, to maintain a foothold in the EU just before the UK's Brexit transition period ends on Jan 31.

The FTSE 250 firm - which owns Birmingham's Bullring shopping centre - expects its shares to begin trading in Ireland as soon as next week, saying it wanted to guarantee its EU investor base could trade its shares on a legally recognised market.

The move will help to maintain an "efficient" business structure across its European portfolio, it said. Hammerson is not raising any new funds or issuing new shares with relation to the admission.

As of June, the firm owned and operated £1.2bn worth of shopping destinations in France and £800m worth of property in Ireland.

It said that around 27pc of its share capital was held by institutional investors based in the European Economic Area - excluding the UK - as of November 23.

The move follows a similar step by warehouse group Segro last month, when it debuted a secondary listing in Paris to sit alongside its main London base.

03:53 PM

Gov to hand £15m to councils to help fix 'broken' audit market

Grant Thornton

Ministers will hand councils an extra £15m to improve book keeping at local authorities after a review warned auditors could abandon the sector over funding cuts.

My colleague Michael O'Dwyer reports:

The decision follows findings by the accounting watchdog in October that three in five audits of local government accounts are not up to scratch.

The audits are supposed to ensure council money is spent and accounted for properly. But five out of six audits carried out by Grant Thornton, the largest player in the market, fell below the required standard, the Financial Reporting Council found this year.

Auditors have complained that cost pressures mean that councils are less well equipped to keep proper records and that funding cuts mean that external firms are not being paid enough for their work signing off on authorities’ accounts.

One senior auditor told The Telegraph that the market for public sector audits was “broken”.

Local government secretary Robert Jenrick said: “It is vital that there is a robust audit system in place across local government to deliver value for money, accountability and transparency for the taxpayer.

“We’ve seen in Croydon and Nottingham the consequences when that isn’t the case.”

03:34 PM

Bank of England spends £600,000 on staff home office equipment

Andrew Bailey

The Bank of England reimbursed £598,000 to its 4,447-strong workforce for office furniture and work-related equipment between March and October 31, according to Press Association.

This works out at £135 per employee - though it allocated a budget of up to £375 per staff member - allowing them to work remotely during the pandemic.

The news agency has more:

Details of the huge bill come after it emerged the Bank spent at least £117,000 making its Threadneedle Street headquarters and offices Covid-19 secure.

Its spending on coronavirus safety measures between March and June included £14,300 for hand sanitisers and £16,600 on masks.

The Bank, who published the figures following a freedom of information request, said: "In line with Government guidance, the vast majority of employees of the Bank of England have been working from home during the Covid pandemic."

The crisis has seen its top policymakers, including governor Andrew Bailey, work from home, especially in the spring lockdown, with rate-setters often delivering speeches and deciding on key monetary policy decisions remotely.

According to the Bank, it had just 75 staff working at its offices on May 1, which increased to 162 on September 1 before dropping again to 31 on November 1, though this was a Sunday.

The Bank said that it "always considers value for money and feels the steps taken are appropriate given the risks posed by Covid-19".

03:13 PM

Handover

That's all from me. My colleague Louise Moon will steer you through the rest of the day's events.

Thanks for following!

02:37 PM

Wall Street opens flat

Wall Street

US stocks have opened flat after little progress on a federal spending deal in Washington.

S&P 500 (unchanged)

Dow Jones +0.03pc

Nasdaq +0.1pc

02:04 PM

Ineos takes one-third stake in Mercedes-AMG Petronas F1 team

Ineos

The Mercedes-AMG Petronas Formula One has a new shareholder with billionaire Sir Jim Ratcliffe’s industrial conglomerate Ineos becoming a one-third owner of the team.

My colleague Alan Tovey reports:

Sir Jim, chairman of Ineos, said the team presented the company he founded with "a unique opportunity to make a financial investment in a team at the very top of its game, but which still has rich potential to grow in the future”.

Ineos became a principal partner earlier this year, and under the new arrangement Mercedes-parent Daimler will reduce its current 60pc shareholding and Toto Wolff, the team’s principal and chief executive, will raise his shareholding to a third.

The 2021 race season will see the introduction of a $145m spending cap intended to make racing more competitive and end years dominance by teams supported by huge resources from major manufacturers.

01:48 PM

IAG snaps up Air Europa in cut-price deal

IAG - REUTERS/Toby Melville/File Photo

British Airways’ owner has agreed to buy a Spanish airline previously worth €1bn – but will not need to hand over any money for up to six years.

My colleague Oliver Gill reports:

IAG, the airlines group that also owns flag carriers Aer Lingus and Iberia, has reportedly agreed a cut-price €500m deal to acquire Air Europa.

IAG announced it would buy Air Europa for €1bn more than a year ago.

The company refused to drop the deal despite cutting 10,000 jobs to save money after the pandemic crippled its finances.

The swoop for Air Europa was one of the final moves by long-term boss Willie Walsh before he retired in September to boost IAG’s presence in Latin America.

Stock markets have been on a bit of a trip already this morning, with the FTSE 100 shaking off some solid gains earlier. Overall, things look quite muted and flat as a crunch weekend approaches.

12:49 PM

Capita-led group gets £1bn Navy and Marines training contract

A consortium led by outsourcer Capita and defence and technology companies Raytheon, Elbit and Fujitsu has won a £1bn deal to train Royal Navy sailors and Royal Marines.

My colleague Alan Tovey reports:

The 12-year agreement aims to modernise how military staff are taught, as well as deliver efficiencies and reduce the time they are away from their frontline duties.

The consortium, known as Fisher Training, will oversee on-the-ground and simulator training across a range of ranks, manage the Navy’s existing educational equipment and market UK military training courses abroad in an attempt to attract new revenue to the UK.

Around 1,100 staff from across the consortium will deliver the training alongside Royal Navy personnel.

In a memo sent to staff on Thursday and seen by the Financial Times, Lloyds’ people and property director Matt Sinnott said the bank would not meet the minimum profit threshold to pay any “group performance share” awards.

The slash to the bonus pool — which was worth £310m last year and £465m in 2018 — highlights the particular challenges facing lenders that do not have investment banking operations to offset pressure in the retail banking market.

12:00 PM

Full report: Shops prepare for record Christmas after retail sales dip

My colleague Tim Wallace has a full report on this morning’s retail sales figures. He writes:

Families spent keenly through November despite a national lockdown in England, raising hopes of a bumper spree now shops have reopened in most areas.

“Retail sales will rebound in December, probably to a new record high, as people undertake their pre-Christmas shopping over a narrower time period than usual,” said Samuel Tombs at Pantheon Macroeconomics.

“Consumers have rushed back to the shops since non-essential retailers were allowed to reopen on Dec 2.”

UK manufacturers’ order books were the strongest in ten months, but stayed weak by historic standard according to the CBI.

Its order books gauge rose to -25 in December, up from -40 in November and better than the the no-change reading expected by economists.

The business group said:

The survey of 261 manufacturers found that output volumes fell at the slow pace in the three months to December as experienced in the three months to November. Output declined in seven of 17 sub-sectors, with the headline fall mostly led by the motor vehicles and transport equipment sub-sector.

Looking ahead, firms anticipate that output will fall at a similarly modest pace over the next three months. This marks a slight improvement in expectations since last month’s survey. Manufacturers also expect muted pricing pressure in the next three months.

10:48 AM

IfO reaction: It will get worse before getting better

Here’s some reaction to this morning’s IfO survey data.

ING macro head Carsten Brzeski said Germany’s economy is stuck between lockdowns and vaccine hopes, entering a period of “hibernation” that will probably result in a double-dip contraction. he added:

A double dip in the fourth quarter looks inevitable, even though the strong performance of the manufacturing and construction sector up to now should make this contraction a very mild one.

Before drowning in despair, the silver linings are visible. By springtime, the rolling out of the vaccine should have gained momentum and the better weather should help to significantly ease the restrictive measures and hence support the economy. Plus, the ongoing fiscal and monetary stimulus as well as an improving global economy should support and benefit the German economy throughout 2021. Hang in there.

The latest PMI data suggested that activity in the country’s manufacturing sector is continuing to accelerate:

Melanie Debono from Capital Economics is slightly more upbeat on Germany’s prospects, saying the rising IfO survey score “supports our view that Germany will avoid a contraction in Q4”. She said that new restrictions coming into effect this week would mean activity stays “subdued”, however, adding:

All told, the recent tightening in lockdown measures means that services and retail activity will continue to struggle in the near term. But, on balance, we now think that Germany’s economy may expand a touch in Q4 thanks to the continued strong growth in industry.

10:30 AM

Flutter shares dip on $870m Kentucky judgement

Shares in Paddy Power-owner Flutter Entertainment have dipped slightly after the group was hit with a $870m judgement by Kentucky’s Supreme Court.

The court reinstated an award of damages against The Stars Group, the US gambling company that Flutter merged with earlier this year, in relation to offshore poker sites that TSG operated. The ruling had originally been vacated in 2015.

Officials ruled PokerStars, part of TSG, had to take responsibility for losses incurred by Kentuckians who played in illegal offshore games. Under Kentucky law, the state is entitled to triple damages. In its ruling, the court said:

The Commonwealth of Kentucky has losses due to PokerStars' illegal internet gambling criminal syndicate. The amount recovered in this case may not cover the actual cost suffered by the Commonwealth of Kentucky.

Flutter said it was “wholly surprised” by the ruling, which was made yesterday. It added:

As previously disclosed, the gross gaming revenues that TSG generated in Kentucky during the relevant period were approximately $18 million. There are a number of legal processes available to Flutter and having taken legal advice, Flutter is confident that any amount it ultimately becomes liable to pay will be a limited proportion of the reinstated judgement.

Goodbody’s Gavin Kelleher said the ruling was an “unwelcome development” for Flutter.

09:54 AM

Synairgen shares jump after efforts to speed up Covid-19 treatment test

Drug developer Synairgen’s shares have popped today after the group said it is updating the trial programme for its Covid-19 treatment to accelerate testing.

The British company said a phase three trial of its SNG001 treatment is “expected to commence imminently”.

Synairgen’s share price has risen massively this year after its treatment showed positive results.

Chief executive Richard Marsden said:

With this adaptation we should be able to reduce the time taken to complete the trial, which, together with an expedited review from the FDA, could allow us to get this therapy approved for patient use in Covid-19 more rapidly.

09:27 AM

Germany business confidence improves

Business confidence in Germany improved this month on hopes that trading will pick up in the first half of 2021.

The latest readings from the IfO Institute found increases in overall business climate spurred by rsing expectations and an improved assessment of the current situation. The headline index rose to 92.1 – economists had anticipated a small drop to 90.

IfO president Clemens Fuest said Europe’s biggest economy was showing “resilience”, noting that manufacturing sentiment had improved strongly alongside “somewhat” of a rise in service confidence.

09:00 AM

Wagamama’s owner warns of ‘significant disruption’ from lockdowns

Wagamama - Mike Egerton/PA Wire

The owner of Wagamama said almost two-thirds of its restaurants will either shut or only serve takeaways as tie restrictions hammer the hospitality sector.

My colleague Simon Foy reports:

The Restaurant Group (TRG) said from Dec 19, when the new tiers come into effect in England, 103 of its sites will shut, 142 will provide delivery and takeaway services, leaving just 145 open for sit-in dining.

The company said the restrictions were “significantly worse” than when initially introduced in October, adding that it expects “significant disruption” to trading while the draconian measures remain in place.

TRG said: “Clearly the mix of locations impacted across the tiers will continue to evolve, but if UK tiering allocations were to remain the same as currently in place throughout the first quarter of 2021, this will have a significant adverse impact on the group, and indeed the wider hospitality sector.”

The group shut more than 100 restaurants because it would have been "uneconomical" to keep them operating, it said.

Michel Barnier has given the European Parliament a stark warning about Brexit talks, telling them: “It’s the moment of truth, we have very little time remaining just a few hours”.

The EU’s chief negotiator said the possibility of a deal “is here”, but the path to secure it “is very narrow” – emphasising fishing as the main outstanding issue left to be resolved.

If no deal is agreed before transition, Mr Barnier suggested that negotiations would continue after transition. “If it is not today, it will have to be later,” he said. The UK and EU have “strong links” and “I expect an ambitious level in that relationship,” he added.

The FTSE 100 has opened flat as European stocks cool off from the ten-month high they reached yesterday. London’s blue-chips are being offered some support by a weaker pound.

Bloomberg TV - Bloomberg TV

07:53 AM

Sir Ian Cheshire to step down as Barclays UK chair

Sir Ian Cheshire

Sir Ian Cheshire will step down as chair of Barclays UK at the start of next year, the bank announced.

He will remain on the board until Barclays’ AGM in May to offer support during the transition.

Barclays UK said over the coming years it “will need a concerted focus on its plans to position the bank to support customers against a backdrop of an economy recovering from the effects of the COVID-19 pandemic and a continuing low interest rate environment”. It added:

With regret, Sir Ian has informed the group that he is unable to accommodate the increased time commitment and duration required to see through this programme.

Crawford Gillies, currently a senior independent director at Barclays, will succeed Sir Ian as chair.

Barclays also announced Julie Wilson is to join its board as a non-executive director from April. She will take up the role after leaving her position at Legal & General, where she have been a NED since 2011. The lender said she “will bring significant corporate finance, tax and accounting experience to the board”.

07:36 AM

Pound dips ahead of open

With less than half an hour until the London open, the pound is currently down slightly against the dollar – taking the edge off the two-year high it was pushing yesterday.

07:24 AM

Online sales at highest level since June

Online retail sales represented 31.4pc of the total in November, the highest proportion since June. Internet retailers’ market shares rose by nearly 75pc only the twelve months to the end of November.

07:19 AM

Clothing and fuel sales drop

Looking at sales broken down by sector, the drops were widespread, with clothing stores and fuel sellers taking a big knock and remaining below pre-pandemic levels. The ‘other non-food’ category also did poorly, with many non-essential retailers force to shut their doors during the month.

07:14 AM

Unadjusted figures show pre-Christmas boom in effect

Retail figures are seasonally-adjusted in order to avoid showing the distorting effect Christmas has on sales. Comparing the unadjusted figures, a typical pre-Christmas boom is clear to see:

The ONS notes that the timing of Black Friday can have a major effect on the figures:

In 2020, the official Black Friday was on 27 November, falling within our November period, which covers four weeks from 1 November to 28 November. However, Black Friday fell outside our November reporting period in 2019 and was included in the December reporting period.

The figures suggest 2020’s seasonally-adjusted sales volume run-rate is slightly below last year:

07:08 AM

Retail sales hold above pre-pandemic levels

Despite a dip last month, overall retail sales remained higher than pre-pandemic levels:

Here are some of the key findings highlighted by the Office for National Statistics:

Clothing store sales saw a sharp fall in sale volumes when compared with the previous month, at negative 19.0pc, as did fuel sales, which decreased by 16.6pc.

Food stores at 3.1pc and household goods stores at 1.6pc were the only sectors to show growth in monthly volume of sales.

The year-on-year growth rate in the volume of retail sales increased by 2.4pc, with feedback from businesses suggesting that consumers had brought forward Christmas spending.

Online retailing accounted for 31.4pc of total retailing compared with 28.6pc in October 2020, with an overall growth of 74.7pc in the value of sales when compared with November 2019.

07:03 AM

Retail sales down 3.8pc month-on-month

UK retail sales fell 3.8pc month-on-month in November, leaving them just 2.4pc higher year-on-year and snapping six months of gains. That is slightly better than was expected.

06:52 AM

What’s expected from today’s data

Today’s retail figures are expected to show a chunky month-on-month dip of 4.2pc in November, according to polling by Bloomberg.

That would leave sales (including auto fuel) 2.4pc higher year-on-year, but would snap a run of consistent monthly growth that started in May.

High-frequency data from various sources suggests that footfall fell sharply last month, with much of the country in some form of lockdown, but there’s also been some suggestion that early Cristmas shopping and pre-Brexit stockpiling may have padded figures somewhat.

06:47 AM

Agenda: Brexit talks tick on as retail data looms

Good morning. Retail data dominates the agenda today, with sales figures for November due out at 7am. They’re expected to show a contraction in spending last month, with a large number of retailers closed due to heightened restrictions in much of the UK.

It’s scheduled to be quiet on corporate front, but with Brexit ticking along in the background there’s the perennial chance of big news on that front.

5) Vaccines give shot in the arm for confidence: Emergence of vaccines has given consumers a shot in the arm, as they reported their biggest surge in economic confidence for almost a decade.

What happened overnight

Asian stock markets were mixed on Friday after Wall Street hit a new high on optimism about economic stimulus and coronavirus vaccine development despite a spike in US unemployment claims.

Tokyo, Hong Kong and Sydney retreated while Shanghai gained. Seoul swung between small gains and losses.

Also on Friday, Japan's central bank extended an emergency loan program by six months and left monetary policy unchanged, as expected.

The Nikkei 225 in Tokyo lost 0.2pc to 26,760.96 while the Shanghai Composite Index added 0.1pc to 3,409.31. The Hang Seng in Hong Kong lost 0.7pc to 26,499.90.

The Kospi in Seoul was up 0.2pc at 2,774.38 at midday while Sydney's S&P-ASX 200 sank 1.1pc to 6,683.20.

India's Sensex opened down 0.3pc at 46,723.73. New Zealand, Singapore and Bankok also retreated while Jakarta rose.

Coming up today

Corporate: No FTSE 350 companies due to report.

Economics: Retail sales, GFK consumer confidence (UK), IFO business climate index (Germany)

Costco made buying a gold bar as simple as tossing it in a shopping cart. Adam Xi, 33 years old, called five different dealers to get a price he could accept for the gold bar he bought at Costco in October. Costco shoppers are spending as much as $200 million monthly on gold, according to a Wells Fargo estimate.

(Bloomberg) -- Super Micro Computer Inc. shares are seeing their biggest drop in about two months on Friday, after the maker of servers announced the date of its third-quarter results but didn’t pre-announce results.Most Read from BloombergElon Wants His Money BackDubai Grinds to Standstill as Flooding Hits CityNew York’s Rich Get Creative to Flee State Taxes. Auditors Are On to ThemIsrael Reported to Have Launched Retaliatory Strike on IranRecord Rainfall in Dubai? Blame Climate Change, Not Clo

Is the shine starting to come off Super Micro Computer stock? Shares of the server maker, better known as Supermicro, fell 14% Friday morning, putting the stock on track for its fifth decline in six sessions.

Microsoft has been one of the pioneers in the field of AI, but this tech giant is also set to win big time from the growing adoption of this technology.

If you are still holding to Nvidia stock, here is a key sell signal to watch for: Shares dipped below the 50-day moving average Friday. Nvidia's chart shows that its relative strength line, which compares the company's stock performance to the S&P 500, is flattening. Chief Executive Jensen Huang recently addressed students at his alma mater of Oregon State University and stated that "artificial intelligence is the technology industry's single greatest contribution to social elevation."

Tesla's growth story was about leading the paradigm shift to EVs, and an affordable car was a part of that story. Now without it, the narrative has changed.