PepsiCo (PEP) Tops Q1 Earnings & Revenue Estimates, Ups View

PepsiCo, Inc. PEP has reported robust first-quarter 2022 results, wherein revenues and earnings beat the Zacks Consensus Estimate. Both top and bottom lines improved year over year. The company continued to benefit from investments in brands, go-to-market systems, supply chains, manufacturing capacity and digital capabilities to build competitive advantages. It also gained from the resilience and strength in the global beverage and convenient food businesses.

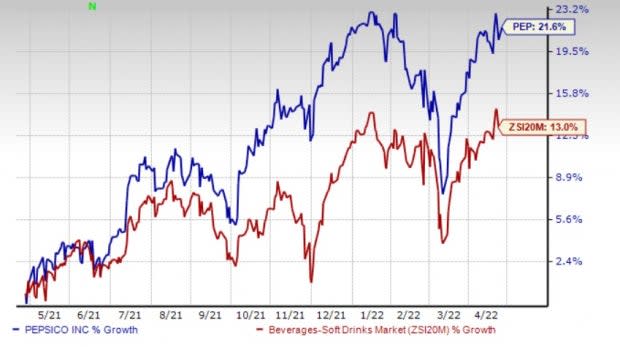

Shares of the Zacks Rank #4 (Sell) company have risen 21.6% in the past year compared with the industry’s 13% rally.

Image Source: Zacks Investment Research

Quarter in Detail

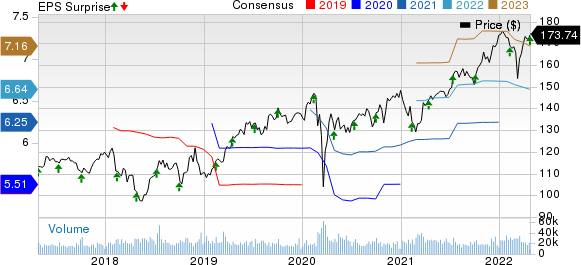

PepsiCo’s first-quarter core EPS of $1.29 beat the Zacks Consensus Estimate of $1.24 and increased 6.6% year over year. In constant currency, core earnings were up 7% from the year-ago period, backed by mitigation of inflationary pressures through cost-management and revenue-management initiatives. The company’s reported EPS of $3.06 grew 148% year over year in the quarter.

Net revenues of $16,200 million improved 9.3% year over year and surpassed the Zacks Consensus Estimate of $15,622 million. Revenues benefited from volume growth and robust price/mix in the reported quarter. Unit volume improved 3% and 6% year over year for the convenient food and beverage businesses, respectively. Foreign currency impacted revenues by 1%.

On an organic basis, revenues grew 13.7% year over year, driven by broad-based growth across categories and geographies. Consolidated organic volume was up 3% and effective net pricing improved 10% in the first quarter. Pricing gains were driven by strong realized prices across all segments.

PepsiCo, Inc. Price, Consensus and EPS Surprise

PepsiCo, Inc. price-consensus-eps-surprise-chart | PepsiCo, Inc. Quote

Revenues were aided by acceleration across both global beverage and convenient food businesses. On a year-over-year basis, organic revenues grew 13% for the beverage business and 14% for the convenient food business. Region-wise, organic revenues improved 13% for the North America business and 15% for the international business.

On a consolidated basis, the reported gross profit increased 7.6% year over year to $8,767 million. Core gross profit rose 9% year over year to $8,879 million. The reported gross margin contracted 90 basis points (bps), while the core gross margin expanded 5 bps.

The reported operating income of $5,267 million rose 127.8% year over year. Core operating income rose 6% year over year to $2,392 million and core constant-currency operating income fell 4%. The reported operating margin improved significantly to 32.5% from 15.6% in the year-ago quarter mainly due to the inclusion of gains from the Juice transaction. Meanwhile, the core operating margin declined 50 bps.

Segment Details

On a segmental basis, the company witnessed revenue growth across all segments. Revenues for the Europe segment remained flat with the last year on a reported basis. Organic revenues also ascended for all segments.

Revenues, on a reported basis, improved 14% in FLNA, 11% in QFNA, 5.5% in PBNA, 19% in Latin America, 14% in AMESA and 8% in APAC. Organic revenues increased 14% for FLNA, 11% for QFNA, 13% for PBNA, 22% for Latin America, 11% for Europe, 18% for AMESA and 9% for APAC.

Operating profit (on a reported basis) increased 4.5% for FLNA, 6% for QFNA, 839% for PBNA, 48% for Latin America, 30% for AMESA and 3% for APAC. Yet, it declined 204% for Europe.

Financials

The company ended first-quarter 2022, with cash and cash equivalents of $6,561 million, long-term debt of $34,590 million, and shareholders’ equity (excluding non-controlling interest) of $18,202 million.

Net cash used in operating activities was $174 million as of Mar 19, 2022, compared with $719 million as of Mar 20, 2021.

Outlook

Looking ahead, PepsiCo is optimistic about its strong position in growing the global categories, which is likely to help steer the ongoing challenging operating environment. It expects to benefit by delivering convenience, variety and value proposition to customers through its brands. However, the company anticipates higher input cost inflation for the balance of 2022.

Given the strength and resilience of its businesses, PepsiCo expects organic revenue growth of 8% for 2022 compared with 6% growth mentioned earlier. The company expects core constant-currency earnings per share to increase 8% from a year ago.

Based on the above assumption, it now estimates core earnings per share of $6.63 for 2022, suggesting a 6% increase from $6.26 reported in 2021. It earlier anticipated core earnings per share of $6.67 for 2022, indicating a 6.5% increase. PEP expects currency headwinds to hurt revenues and core earnings per share by 2 percentage points in 2022, based on the current rates. The company continues to expect a core effective tax rate of 20%.

PepsiCo remains committed to rewarding shareholders through dividends and share buybacks. The company anticipates total cash returns to shareholders of $7.7 million, including $6.2 million of cash dividends and $1.5 billion of share repurchases.

Don’t Miss These Better-Ranked Stocks

We highlighted some better-ranked stocks from the broader Consumer Staples space, namely The Duckhorn Portfolio NAPA, Ambev S.A. ABEV and Dutch Bros BROS.

Duckhorn currently has a Zacks Rank #2 (Buy) and an expected long-term earnings growth rate of 11.3%. NAPA has a trailing four-quarter earnings surprise of 122.4%, on average. The company has gained 7.1% in the past year.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Duckhorn’s current financial-year sales and earnings per share suggests growth of 9.6% and 3.5%, respectively, from the year-ago reported numbers. The consensus mark for NAPA’s earnings per share has been unchanged in the past 30 days.

Ambev currently has a Zacks Rank of 2. ABEV has a trailing four-quarter earnings surprise of 3.3%, on average. It has a long-term earnings growth rate of 7.9%. The company has gained 8.5% in the past year.

The Zacks Consensus Estimate for Ambev’s current financial-year sales and earnings suggests declines of 33.8% and 6.7%, respectively, from the prior-year reported number. The consensus mark for ABEV’s earnings per share has moved up by a penny in the past seven days.

Dutch Bros currently has a Zacks Rank #2. BROS has a trailing two-quarter earnings surprise of 93.75%, on average. It has an expected long-term earnings growth rate of 35.9%. The company has gained 43.9% in the past year.

The Zacks Consensus Estimate for Dutch Bros’ current financial-year sales and earnings per share suggests growth of 42.7% and 3.3%, respectively, from the year-ago reported numbers. The consensus mark for BROS’ earnings per share has moved down by a penny in the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PepsiCo, Inc. (PEP) : Free Stock Analysis Report

Ambev S.A. (ABEV) : Free Stock Analysis Report

The Duckhorn Portfolio, Inc. (NAPA) : Free Stock Analysis Report

Dutch Bros Inc. (BROS) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research