Former Treasury Secretary Larry Summers slammed a hotly debated economic theory for suggesting that government debt should not be interpreted as a constraining factor to fiscal policy.

Modern Monetary Theory, or MMT, argues that a country borrowing in its own currency can finance fiscal stimulus by printing money. By extension, MMT would allow the government to control inflation through tax policy. Instead of asking the Fed to stabilize prices through monetary policy, the government could raise taxes when prices get too high and cut taxes when prices get too low.

Summers, who served as Treasury Secretary under Bill Clinton and later briefly headed the Obama administration’s National Economic Council, says the theory is “voodoo economics.”

“It takes ideas that have a little bit of validity and extends them to a grotesque point where they defy the laws of arithmetic,” Summers said in an interview with Yahoo Finance. “So I believe MMT is very much misguided, the premise that somehow you can always print enough money to cover all of your debts.”

The policy has been gaining traction on Capitol Hill as the likes of New York Democrat Alexandria Ocasio-Cortez and Vermont Senator Bernie Sanders fit the MMT framework with ambitious fiscal policies like the Green New Deal and universal healthcare.

Summers said MMT was to blame for hyperinflation in Latin American countries that tried variants of the economic theory. But Summers agreed with MMT’s argument that fiscal policy needs to be more efficient, adding that he thinks the government could craft better policy on global climate change and tax shelters. He just doesn’t think that should be done within the framework of MMT.

“I don’t think there’s any conflict between being in favor of reasonable economic policy and being successful politically,” Summers said.

Replacing monetary policy

Federal Reserve Chairman Jerome Powell is also among MMT’s critics. In his testimony to Congress last week, Powell said the core tenets of MMT are “just wrong” and said the Fed would be quicker and more effective at tackling inflation than fiscal policy could.

But amid concerns that the Fed’s struggles to get inflation to its 2% target, some MMT proponents argue that fiscal policies might have more teeth in handling inflation.

Summers said during low-interest rate environments, he supports expansionary fiscal policy, but cautioned against fiscal policies that might be too aggressive and saddle the government with unsustainable levels of debt.

For the fiscal year 2018, the deficit was 3.85% of GDP.

“I don’t know what so-called ‘Modern Monetary Theorists’ have in mind, but the idea that we should abandon the tool of monetary policy and somehow make the central bank subservient, seems we’ve seen that movie before,” Summers said.

Wall Street taking notice

Analysts are closely dialed into the debate on MMT, especially as the 2020 election comes into view. Morgan Stanley’s research team noted that markets should consider whether Congress is adopting a more ambivalent tone toward government deficits.

“If this became an axiom among the presidential candidates, or at least among the ones who start to break from the field, markets would likely take notice of the risk that the deficit trajectory, and de facto fiscal stimulus, could rise again in 2021,” Morgan Stanley wrote in the note published on February 13.

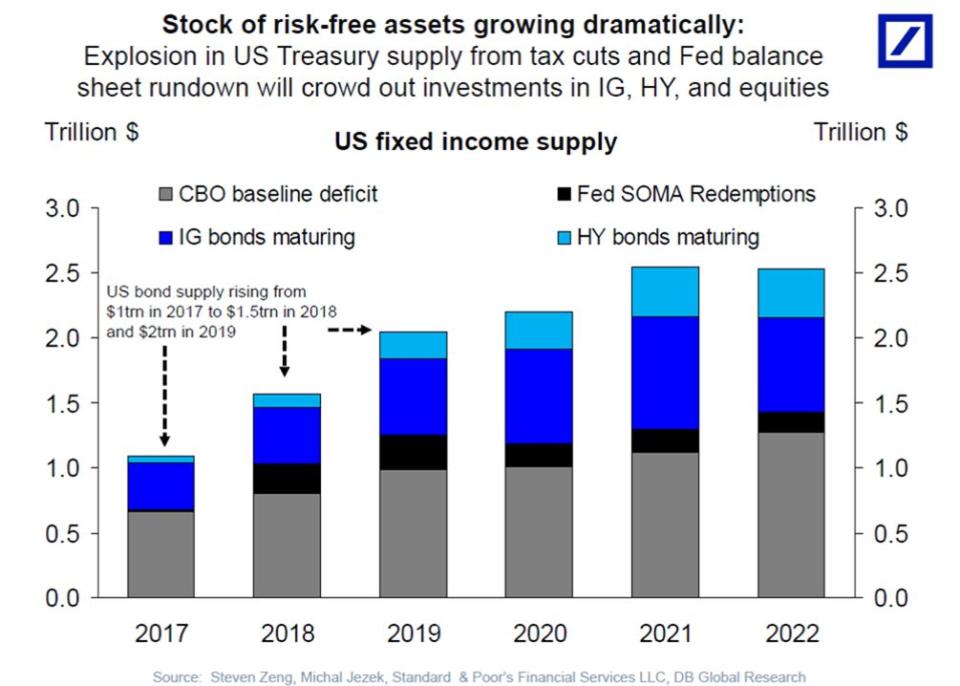

DB Global Research’s Torsten Slok wrote last month that the market makes cases for and against MMT. Given the low levels of longer-term Treasurys, Slok argues that the government could increase debt levels “without any consequences,” but argues that there is an inflection point where printing money will crowd out investments in other asset classes.

“The bottom line is that from the current level of 10-year Treasuries it may look like there is a free lunch with little impact from US deficits to US interest rates, but it is the impact of Treasury issuance on credit spreads which is most relevant for markets,” Slok writes.

Brian Cheung is a reporter covering the banking industry and the intersection of finance and policy for Yahoo Finance. You can follow him on Twitter @bcheungz.

Read more:

The Fed may be suffering from a 'credibility' issue with its inflation target

Will we get to 3% GDP growth this year? Economists say no.

Warren accuses Fed of approving bank mergers with 'rubber stamp'

Powell signals that balance sheet rolloff could end as early as October

Congress may have accidentally freed nearly all banks from the Volcker Rule