What Is a Financial Advisor Disclosure?

Managing your finances doesn’t have to be a solo mission. Financial advisors provide expert advice and recommendations on everything from budgets to investments. In fact, industry experts say that people with financial advisors are twice as likely to meet their retirement goals. But not every advisor will fit your needs, and it can actually be quite difficult to choose.

Before making your choice, you’ll want be aware of any past disciplinary actions on an advisor or firm’s record. That’s where financial advisor disclosures come in. Read on to learn what a financial advisor disclosure is, where to find them and how to interpret them.

What Is a Financial Advisor Disclosure?

The term financial advisor disclosure can refer to two slightly different things. More broadly, a financial advisor disclosure is a report in which an advising firm publicly releases details about its background, fee schedule, services and advisors’ conduct. You can find this information in financial advisor disclosure documents such as Form ADV, a registration document submitted to the Securities and Exchange Commission (SEC) and state securities authorities.

A financial advisor disclosure can also refer more specifically to any past regulatory, criminal or disciplinary actions on a firm or advisor’s record. Disclosures are documented within Form ADV. Information on the allegation, resolution and any requisite penalties is included. Disclosures can range in severity and include issues like customer complaints, arbitration and civil proceedings, sanctions and terminations.

Making this information publicly available levels the playing field for all advisors. It also helps consumers make an educated decision. The Securities Act of 1933 and the Securities Exchange Act of 1934 require this reporting. Form ADV, including financial advisor disclosures, must be updated annually.

How to Access Form ADV

Potential and current clients of financial advisors can always request a Form ADV. The rules require firms to make these documents public and available. Whenever there is a new disclosure or a material change to information already disclosed, firms must deliver an updated ADV supplement to current clients.

You can also access a Form ADV online for free. Just go to the SEC’s Investment Advisor Search tool and look up the firm by name or central registration depository (CRD) number. Not tech savvy? You can also request a copy of a Form ADV from an SEC branch.

How to Find Disclosures on Form ADV

There are two parts to Form ADV. Part A is fill-in-the-blank style and includes identifying information about a firm, like its phone number and address, number of accounts and employees and total amount of assets under management. Part B is written in prose as a longer narrative about the firm. Structured like a brochure, it includes information about the types of advisory services offered, the fee schedule, conflicts of interest and the educational and employment backgrounds of key employees.

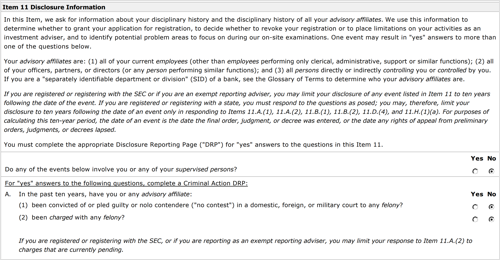

You can find information on a firm’s disciplinary information in both parts. Disclosure information is listed in Item 11 of Part A. In this section, the firm must respond yes or no to whether the firm or any of its supervised persons has been convicted of or charged with specific violations, including a criminal, regulatory or civil judicial action. If the firm answers yes to any of the questions, it must then complete a disclosure reporting page, attached at the end of Part A. In the reporting page, the firm must provide further information on the disclosure, including who initiated the action and when, the docket/case number, a description of the allegation, its current status and, if it’s resolved, how and when it was resolved.

While Part A is useful for a quick glance at whether or not a firm has disclosures and what the nature of those disclosures are, Part B provides further detail in plain prose. In Item 9 of Part B, a firm must provide a paragraph or two explaining each of disciplinary action.

How to Interpret Financial Advisor Disclosures

Not all financial advisor disclosures carry equal weight. Complaints can happen for a number of reasons and are sometimes the result of what’s going on in the industry. For instance, the 2008 market crash spurred a slew of complaints. An advisor who has been in business for several decades is more likely to have a disclosure on his or her record than an advisor who is just starting out. Moreover, some disclosures may be far in an advisor’s past.

Regardless, you should speak to prospective advisors and do your own research about any disclosures on their records. It can be a red flag if an advisor has numerous complaints on record that are similar in nature. A large number of past customer complaints can suggest a track record of dissatisfied customers. Sanctions, such as a suspension or fine imposed by the SEC or federal regulatory industry, can indicate an advisor or firm’s failure to comply with industry rules and regulations.

What to Do If Your Financial Advisor Has a Disclosure

If you note a disclosure on an advisor’s record, you should do your own research on the disciplinary action and also be sure to discuss it with your prospective advisor. Don’t hesitate to ask questions. While all disclosures are serious, some are more severe than others.

You shouldn’t move forward if you are uncomfortable with any disclosures. If there is a history of action taken against the institution, gather as much independent information as you can. If it seems to be a pattern, you may decide to steer clear.

The Bottom Line

You should be able to know everything you want about a financial advisor before you hire them. This is your money, your personal information and your future. It’s extremely important that you review a firm or individual’s Form ADV before you decide to work with them. You can also do a Google search and ask around about their practice. You can never be too careful. Once you’ve found several potential advisors, compare their brochures side-by-side to see how they differ and which offers a better service at a better value. After you’ve narrowed it down, set up meetings with a few of them. You can also use the disclosures to guide your interview questions.

Tips for Finding a Financial Advisor

As this article should’ve made abundantly clear, it’s imperative to do your research before choosing an advisor. Look at a firm’s website, Form ADV paperwork and ask any questions. A good indication that a financial advisor has your best interest in mind is if he or she is a fiduciary.

If you’re not sure where to start, get outside advice. Ask trusted friends or family members where they get financial advice. Or, use SmartAsset’s financial advisor matching tool, which will match you up with nearby advisors who suit your needs. You can also look at the top financial advisor firms in New York, or whichever city you live closest to.

Don’t forget get to ask yourself some questions, too. Financial advisors have different areas of expertise, so it’s important to consider why you want an advisor before diving into the search. If you’re looking for helping crafting a financial plan, a certified financial planner (CFP) may be useful. If you’re going through a divorce, you might want the assistance of a certified divorce financial analyst (CDFA).

Photo credit: ©iStock.com/Sezeryadigar, https://adviserinfo.sec.gov/, ©iStock.com/seb_ra

The post What Is a Financial Advisor Disclosure? appeared first on SmartAsset Blog.