Disney Is an Amusement Parks Company, Analyst Says; TV and Movies Are a Side Hustle

You would think Disneyland was the un-Happiest Place on Earth™ the way Wall Street values Disney, one media-analyst group argues.

Researchers at Moffett Nathanson are baffled by the “shocking… underperformance” of Disney shares (DIS), which are down 30 percent since the start of 2021. Considering the overall stock market is up about 30 percent in that period, the DIS movement in the wrong direction “paints a depressing picture.”

More from IndieWire

And a confusing one. The struggles of media stocks, and streamers in particular, is well known — but Disney is no pure-media company and considering the post-Covid “amazing resurgence” (see below) of its U.S. parks-and-resorts business, the analysts cannot fathom why “the market has overly punished” DIS.

Disney shares aren’t seeing the worst of the media-stock carnage — ask Paramount Global (-49 percent) and Warner Bros. Discovery (-54 percent) about that. However, the one-third decline in Disney value is too harsh. After all, Paramount (PARA) and Warner Bros. Discovery (WBD) don’t have Disney’s lucrative parks, experiences, and consumer products business.

As “the biggest driver of Disney profits,” Moffett Nathanson wrote, it should be valued like a travel and leisure company. Disney’s parks are the “overlooked crown jewel” and are of “increasing importance” to the organization’s overall financial health. And Michael Nathanson brought receipts.

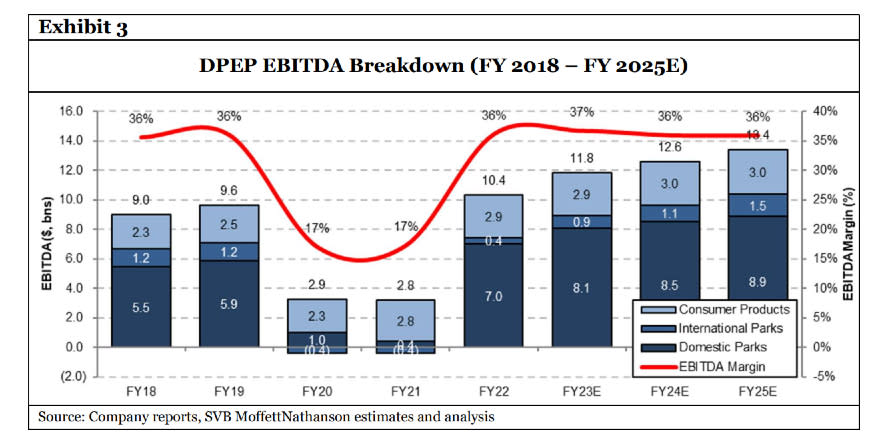

Courtesy of Moffett Nathanson

Disney’s U.S. Parks have an enterprise value (market cap + debt + cash) of $105 billion, Nathanson calculates; international parks add a bit over $30 billion more. Consumer products ($35 billion) brings the total to $170 billion. Considering the overall enterprise value of The Walt Disney Company is $230 billion, per Nathanson, all the other stuff adds up to just $60 billion. That’s cute.

Put another way, nearly three-quarters of Disney’s current value comes from its parks, experiences, and products. One quarter comes from the other two-thirds (organizationally, at least) of the company: entertainment (linear, streaming, and studios) and ESPN. A spokesperson for Disney corporate did not immediately respond to IndieWire’s request for comment on the Nathanson valuation breakdown. Disney’s current market cap, the total value of all its shares, is about $182 billion.

At a $60 billion enterprise valuation, Disney’s television and film businesses, including streaming, would be worth $100 billion less than Netflix ($163 billion EV) and lower even than Warner Bros. Discovery ($79.3 billion EV), Nathanson estimates. A spokesperson for Netflix did not immediately respond to IndieWire’s requests for comments on those estimates. A Warner Bros. Discovery rep confirmed their valuation is within the ballpark. (Unfortunately, that’s the only park WBD has here.)

“Would investors really put a significant discount on owning Disney+, Hulu, ESPN, ESPN+, India’s Star/Hotstar and even the Disney Studio (Marvel, Star Wars, Pixar, Disney Animation) and the entire Disney film and TV library?” Nathanson posed in his 18-page research report for clients, obtained by IndieWire. “We believe all of these assets should trade at a premium to Warner Bros. Discovery and at a much narrower gap to Netflix.”

Get it together, Wall Street: DIS should be worth $130 per share, he continues to argue — not the $99-and-change it currently trades for.

Equity analysts at Wells Fargo think their friends at Moffett Nathanson are being too kind to Wall Street. On February 8, following the Disney earnings report, Wells Fargo upped its DIS price target from $125 to $141. At the time, they recognized a Disney equity value of $257 billion, $167 billion of which came from Disney’s Parks/Experiences. (Equity value is like enterprise value but also considers future potential.) At the time, shares of Disney were trading about $12 better than they are today.

Disney itself is not without blame in this valuation head scratcher. For starters, there is a free cash flow issue (just $1.3 billion in fiscal 2022; it peaked at $10.1 billion in 2018), and management makes no guarantee Disney+ will actually turn a profit in 2024. Plus, Hulu’s future is a gigantic question mark with a giant pending price tag that hangs over Disney, which currently owns two-thirds of that streamer and is on the hook to buy out Comcast’s one-third in about eight months. And despite CEO-again Bob Iger’s kind words for his sports brand, ESPN’s future is nearly as much in question.

Nathanson believes with lowered content spend, Disney’s free cash flow this year will be $4.6 billion — and that’s almost entirely thanks to the parks. Another big splash from Splash Mountain.

Best of IndieWire

Where to Watch This Week's New Movies, from 'The Equalizer 3' to 'Perpetrator'

The Best Survival Movies, from ‘Cast Away’ and ‘The Revenant’ to ‘The Martian’ and ‘Alive’

Sign up for Indiewire's Newsletter. For the latest news, follow us on Facebook, Twitter, and Instagram.