Why Uber has clawed back to its IPO price while Lyft still has a ways to go

Since their rocky introduction to public markets, Uber (UBER) and Lyft (LYFT) have managed to claw back from steep losses that dragged their stocks below their respective initial public offering (IPO) prices.

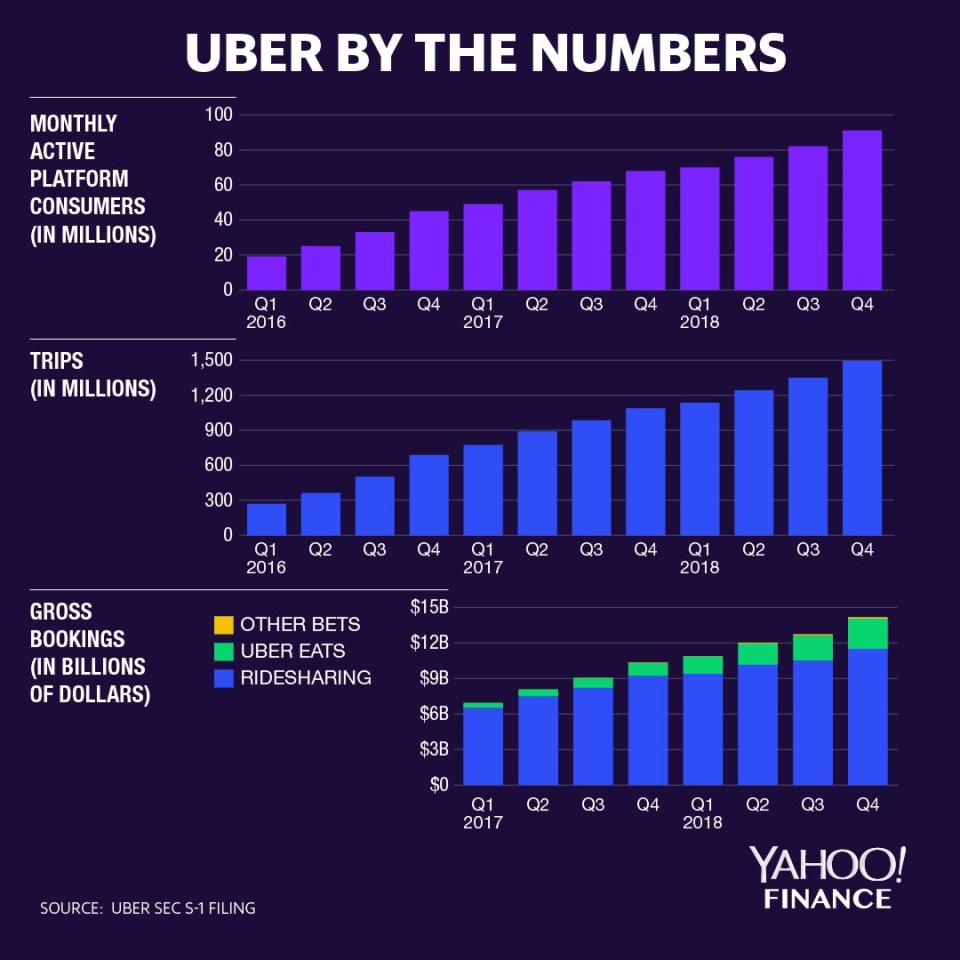

Among the flood of privately-held companies valued above $1 billion (otherwise known as unicorns) coming to market, Uber and Lyft were the hottest names in the bunch.

That is, until they actually went public and saw their freshly minted share prices plunge. And for now, it seems as if the one getting the most benefit of the market’s persistent doubts is Uber.

After its lockup period expired this week, the ride hailing giant basked in a raft of bullish calls from Wall Street analysts. The bulls, however, seemed to downplay one significant problem: Uber is bleeding money, and has no road to profitability in the near term.

In fact, Uber’s price action since its IPO has been far more forgiving than Lyft’s—which was hammered as low as $47.17, tumbling from a first day intraday trading high above $88 after pricing at $72 per share.

The former closed trading on Wednesday at $45 per share, retaking its initial price; while Lyft closed above $63 — soaring more than 6% on the day but still well below its IPO level.

Although Lyft has more than its share of praise and bullish recommendations from analysts, the playing field and optimism appears tilted toward Uber. It raises the question of whether the market is too optimistic about the latter —and too pessimistic about the former.

So why is that?

Uber’s “future profitability to come from fewer subsidies, long-term pricing power and reduced costs as the company benefits from its growing size,” analysts from RBC Capital Markets explained.

Amid praise for Uber’s food delivery, shared bikes and scooters, and other initiatives, the company “will benefit from insurance leverage as its businesses other than ride-sharing grow larger,” RBC said.

Whither Lyft?

That bullishness contrasts sharply with Lyft, Uber’s nearest competitor. The former, which is also losing money, faces stiff challenges that some think are a barrier to becoming profitable, or at least overtaking Uber.

Those problems include high costs for asset ownership on the supply side, and industry specific costs like driver incentives and insurance.

“Lyft is the number two player in its core business, operating against a larger, well-funded competitor,” said analysts from Stifel. The firm, however, maintains a Buy rating on Lyft’s stock with a 12-month price target of $68.

Still, “Lyft sustains heavy losses, which we expect to expand in absolute dollar terms in 2019 as the company invests in its core ride sharing business, bikes & scooters,” among other things, Stifel pointed out.

And not unlike Uber, “the viability of Lyft’s long-term business model is unproven,” the firm noted.

Separately, HSBC cut its price target on Lyft to $52 from $60, maintaining its rating on the stock as a Hold.

Among other factors, Lyft stressed that Lyft has too high of a fixed cost base and that it needs to “significantly scale its business” in order to make a profit.

“Lyft needs to significantly scale its business and grow gross bookings at least 2.5x-3x to reach profitability, in our view,” HSBC added. “As with many other marketplace-type businesses, the leading player does not take all, but takes the lion’s share of profits due to scale.”

Uber-bullishness overdone?

At least one market observer is skeptical of Uber’s future. Elliot Lutzker, a securities lawyer and former SEC prosecutor, took aim at the company’s reliance on autonomous driving, while arguing Lyft has more potential for growth on the market that some think.

“Uber is losing so much money betting on the car they may not make,” Lutzker told Yahoo Finance in an interview.

“Lyft, a smaller company, has just as good a chance,” he added. “If Uber is not making money today and their workers go on strike for being undercompensated and they have to pay them more money, they are going to be even less profitable.”

The buzz over Uber is strongly reminiscent of the early years of the Dotcom era, a bubble that burst nearly 20 years ago, and left countless investors in the red.

But analysts, in what might ultimately become famous last words, think this time really is different.

“In contrast to traditional Internet companies, Uber is a digital app powering offline behavior”--namely transportation and food delivery, said analysts at Raymond James this week. By extension, that includes rival Lyft.

“This elevates cost in the early years, but arguably creates a more defensible long-term position,” the firm added.

Editor’s note: Uber priced at $72 per share.

Donovan Russo is a writer for Yahoo Finance.

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and reddit.