Amid student debt surge, a debate over whether $1.5T is a crisis or 'peanuts'

College graduates saddled with loans has become a major problem for the economy, and a political hot potato. So just how big is the problem, really?

It depends on who’s asking the question—and who’s answering it.

First, some hard, sobering numbers: More than $1.5 trillion of outstanding student debt is owed by borrowers today — the highest ever in history.

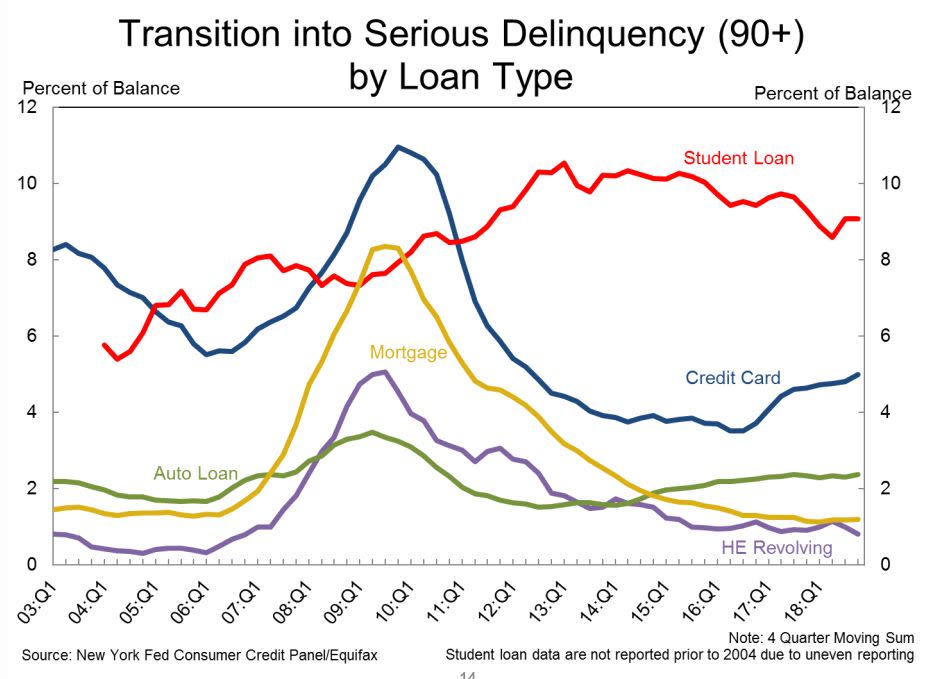

Meanwhile, with 11.5% in serious delinquency, the average borrower is struggling with thousands of dollars in student debt. The overhang has forced cash-strapped borrowers to put off major milestones like starting a family and owning a home — which many economists say is a drag on economic growth.

The student loan problem has even prompted presidential candidates like Massachusetts Democratic Senator Elizabeth Warren to propose radical reform to the system.

Former FDIC Chair Sheila Bair wrote recently that the entire concept of student loan debt should be cancelled altogether. In a New York Times op-ed, Bair called on the U.S. to “scrap debt financing of higher education and make the transition” to a system that let borrowers pay a fixed percentage of their income across a long period of time.

That arrangement would factor in pay as well as built-in protections against “life events,” she added.

‘Crisis’ or ‘peanuts’?

For many, the current inability to get out from under college debt is a real and growing problem.

However, according to some observers, unpaid student loans are a problem for the federal government— rather than a time-bomb like the housing meltdown that eventually led to the 2008 financial crisis.

As a result, student debt is “a taxpayer problem, and not a problem for the nation’s banking or financial system,” Moody’s Analytics Chief Economist Mark Zandi told Yahoo Finance in an April interview.

Along those lines, at least one economist thinks the crisis is really little more than “peanuts.”

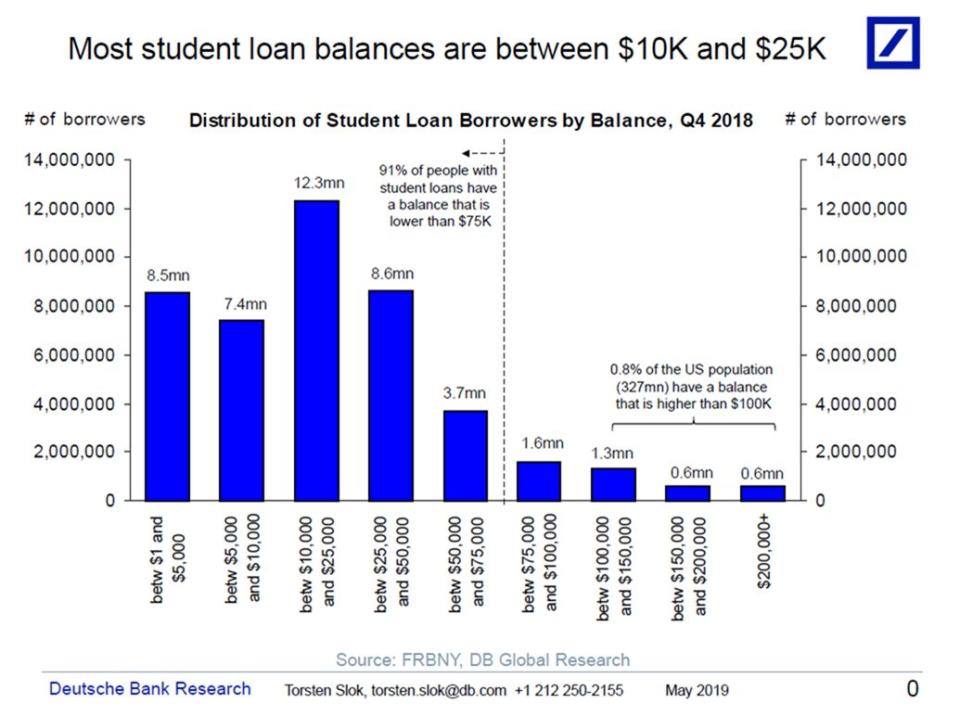

Deutsche Bank’s chief U.S. economist Torsten Slok, citing Federal Reserve data, points out that U.S. household net worth is over $100 trillion.

Along with the fact that outstanding student loans are largely below $75,000 — and that less than 1% of the population has a balance larger than $100,000 — Slok said in a recent note that the crisis is a “micro” rather than a “macro” issue.

From Slok’s perspective, the number of outstanding loans don’t warrant alarm for one simple reason: Household wealth is growing exponentially. Indeed, Fed data show that collective household net worth has nearly doubled since the onset of the Great Recession.

It suggests that despite climbing secondary education costs and a soaring loan burden, households have the propensity to pay back loans.

Credit cards, car debt a bigger worry?

Yet Slok also previously pointed out that household debt — particularly credit card and auto loan debt, but not student loans — was a bigger problem to watch. He insists because “the clock is ticking,” with an increasing number of delinquencies on those personal loans.

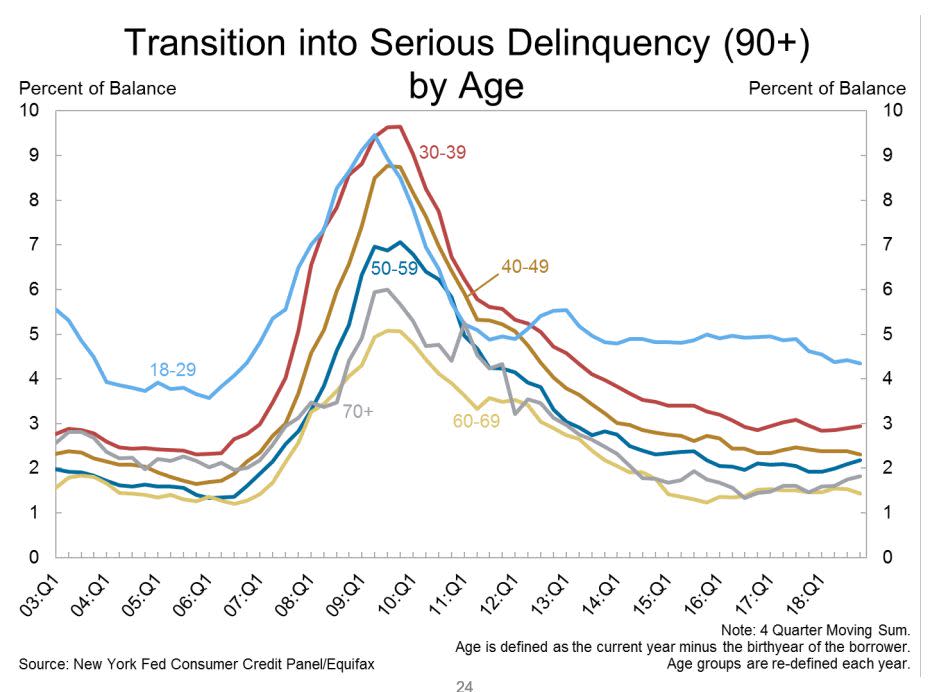

That troubling trend is underscored by recent figures from the New York Fed. With student loans transitioning into seriously delinquent territory of 90 days late or more during the first quarter of 2018, credit card debt and auto loans backlogs also inched higher, the central bank showed.

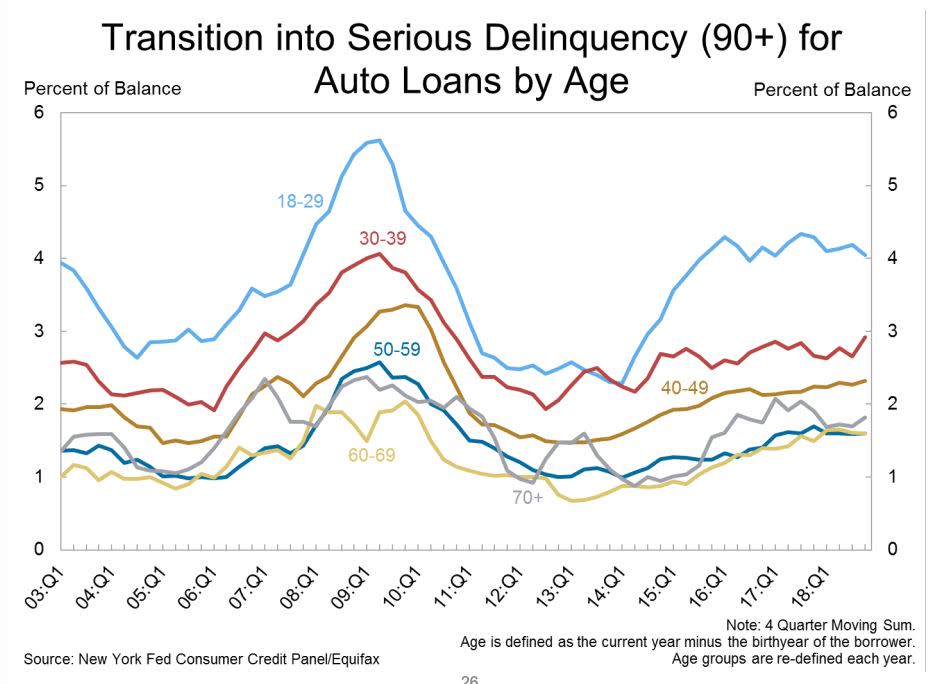

The Fed’s data said the biggest reason why the 18 to 29 age group (i.e. millennials) was facing serious delinquency on their personal loans was because of their failing auto loans.

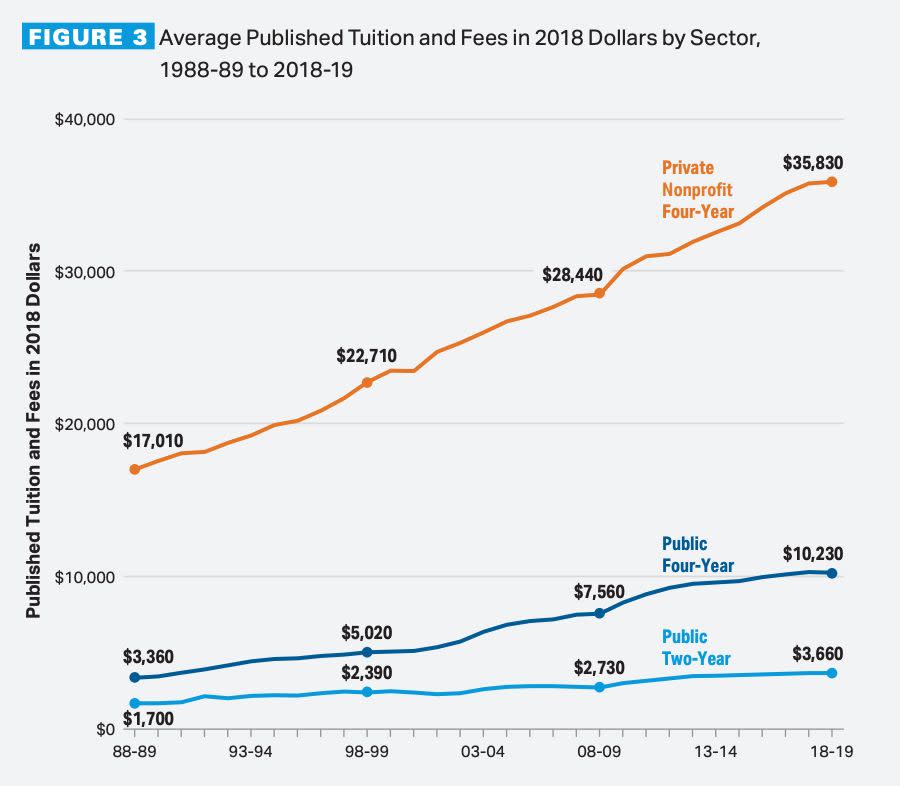

College costs climb higher

According to a report from USAFacts, nearly 62% of undergraduate students got a loan during the 2015- 2016 school year, up from 52.5% in the 1999-2000 school year. During that time frame, the average loan amount soared by a whopping inflation-adjusted 22.

Loan balances have been ballooning largely because it costs more to attend college. Costs at higher institutions have been steadily rising over the years — and most of the price inflation doesn’t even include daily expenses, and room and board.

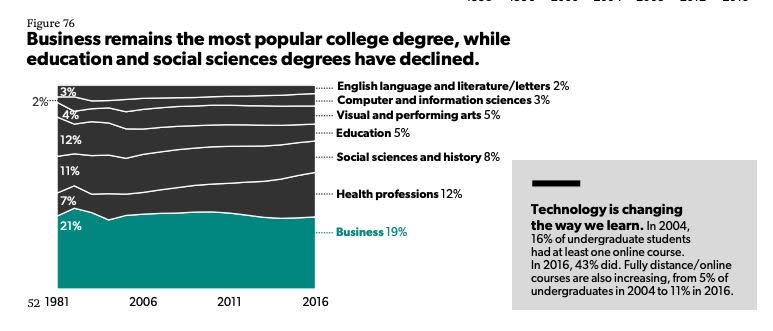

Some critics have faulted students taking on obscure coursework that doesn’t lead to more lucrative career choices. Yet overall costs have risen for everyone— even as data shows degrees in business and health care are increasingly popular.

Possible solutions to the ‘crisis’

While opinions differ on the “micro” versus “macro” dimensions of the student debt crisis, most argue the reality of debt saddled graduates require immediate attention.

For some people, “student loans enable positive life outcomes and for others they do not,” said David Klein, CEO and co-founder of CommonBond, a platform that provides affordable student lending through a pool of investors.

Klein told Yahoo Finance that “the main cause is an uneven distribution of outcomes by school. Some colleges and universities very effectively prepare students for gainful employment post graduation, while other schools do not.”

His solution is to boost transparency in the college system in a way that prevents excessive borrowing. That includes schools publishing the costs of school each year, loan repayment requirements, and a benchmark of how graduates from their program make post-graduation.

“Those three pieces of information will enable people to make smart choices based on data and value,” he said.

Aarthi is a writer for Yahoo Finance. Follow her on Twitter @aarthiswami.

Read more:

Elizabeth Warren unveils 'broad cancellation plan' for student debt

Dimon: U.S. student loan debt is ‘now starting to affect the economy’

'The clock is ticking' on U.S. consumer loans — and that could mean a slowdown, Deutsche Bank warns

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.