Tech companies like Lyft want your money — not 'your opinion'

Many tech companies look very similar when it comes to one key detail in their corporate governance – and this isn’t necessarily good news for investors, according to some experts.

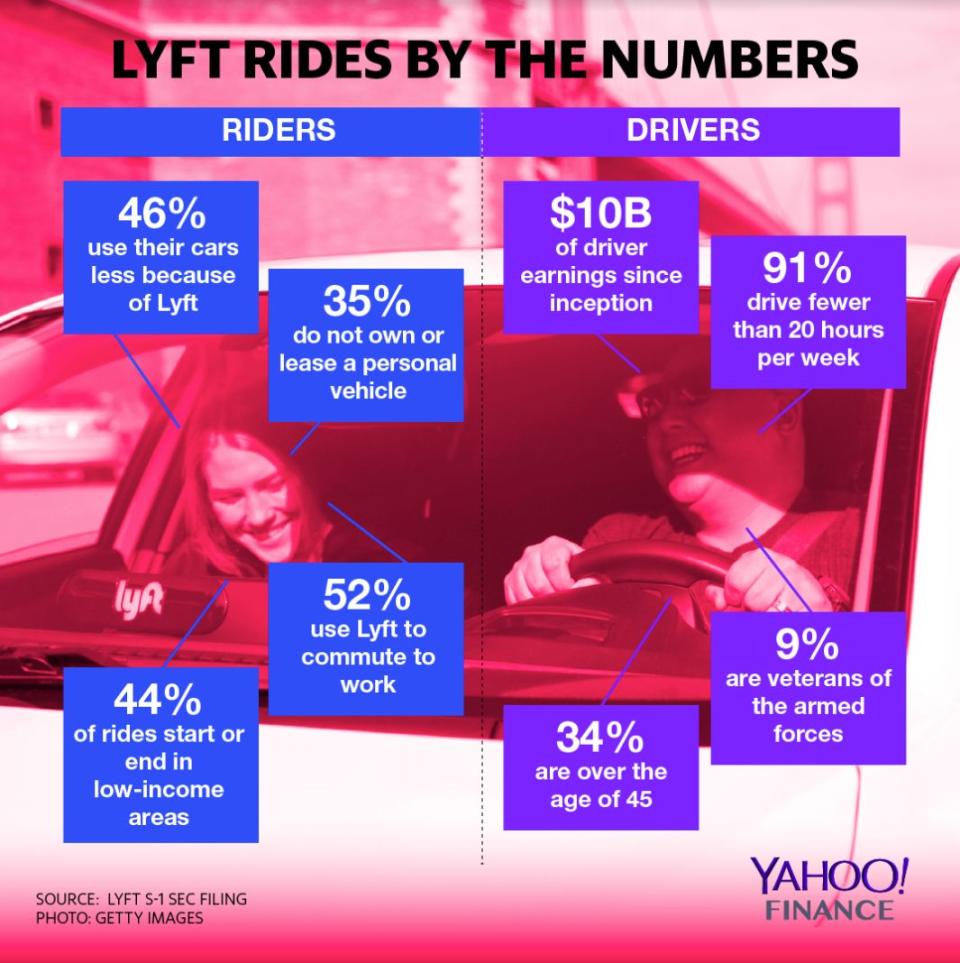

Lyft on Friday became the latest company to come to market with a dual-class share structure, issuing two classes of common stock: Class A shares, which everyday retail investors can purchase, and Class B shares, restricted to owners.

By Lyft’s description, the two classes of shares are “identical” – except when it comes to voting and conversion rights. Each Class A share allows investors to cast one vote on corporate issues, while Class B shares carry 20 votes apiece. The dual-class structure gives co-founder Logan Green about 30% of voting power on shares outstanding, and co-founder John Zimmer about 20% of voting control.

A multi-class share structure has become de rigueur among major technology firms, with companies from Facebook (FB) to Google-parent Alphabet (GOOG, GOOGL) carrying the composition. But retail investors should be wary as this form of corporate governance spills over to some companies involved in the latest batch of tech IPOs in 2019, some experts said.

“The dual-class structure destroys accountability of management to those investors,” Charles Elson, chair of corporate governance at the University of Delaware, said in an interview with Yahoo Finance. “They don’t have a voice.”

Such a structure makes it possible for company insiders to sell down their positions significantly while limiting dilution of control, Elson said. In one example, Facebook’s stock structure, which grants Class B shareholders 10 votes per share versus the one vote per Class A share, allows Mark Zuckerberg to maintain voting control even when offloading millions in shares.

“It means that they want your money, they just don’t want your opinion,” Elson said of firms issuing shares with distinct voting rights. “It’s pretty sad.”

Some firms have taken it to the extreme, creating classes of stock that eliminate shareholders’ voting capacity altogether. Snap (SNAP), which made its initial public offering in March 2017, has three classes of stock, with its Class A shares available to retail investors on the New York Stock Exchange carrying zero votes. Class A shareholders, however, can still attend the company’s annual shareholder meeting and ask questions.

New normal

Lyft aside, other highly-anticipated companies planning to hit the public exchanges this year have also floated multi-class stock structures. Photo-sharing platform Pinterest said in its S-1 last week that it also intends to issue both Class A and Class B shares with asymmetric voting rights. But unlike Lyft, it included a “sunset clause” stating that Class B shares will convert to Class A shares seven years after the initial public offering for holders carrying less than 50% of Class B stock.

Tech firms aren’t the only companies offering shares with discrepancies in voting rights – in fact, the Council of Institutional Investors counts more than 200 U.S.-incorporated companies with at least two outstanding classes of common stock and unequal voting rights. Retailer Levi Strauss (LEVI) returned to the public markets last week with a share structure that granted its insiders – descendants of Levi Strauss himself – two-third of the firm’s outstanding stock and 99% of voting power.

Nevertheless, tech companies have drawn some of the most scrutiny given their name recognition and existing controversy over encroachment in other aspects of consumers’ lives.

“It's a bit of an arrogance, I think a lot of people would say,” Elson said. “It's just a view that, ‘I'm the smartest person in the room, you're not. And I'd rather not hear from you.’”

To be sure, the broader retail shareholder base already tends not to be engaged with their companies’ governance. A recent study from Broadridge found that just 28% of retail investors participated during proxy season in 2018, leaving them on the sidelines for issues including executive compensation or proposed mergers and acquisitions.

But just because a majority of retail investors don’t vote doesn’t mean they should have the choice eliminated completely, Brian Hamilton, co-founder of Sageworks, said in an interview with Yahoo Finance.

Moreover, such a stock structure could also carry implications for markets as a whole, Hamilton added.

“The psychology is not good, the fairness is not good. It's not going to be the sole factor that drives prices down, but you don't want the investing public to not have faith in the markets,” Hamilton said. “And if they think things are unfair, they're not going to have faith in the markets.”

‘A real blessing’

While some are concerned about representation issues brought about by dual-class share structures, others argue the feature provides a strong incentive for management to want to bring their companies public in the first place, thereby opening up value for stockholders that wouldn’t previously have existed if the firms had stayed private.

David Ethridge, PwC managing director and former head of capital markets at the New York Stock Exchange, said he felt the permissibility of multi-class shares on U.S. exchanges was a major benefit to domestic capital markets.

“I always found that when I was at the NYSE and responsible for the IPO business there, I thought that was a real blessing for the U.S. capital markets because I felt they were more flexible than other markets were,” Ethridge said in an interview. “And I thought that was something that was advantageous for us in the U.S., so it would help us attract non-U.S. companies to our capital markets, which I thought net-net was a benefit.”

Ethridge pointed out that international exchanges – including in Hong Kong and in Singapore – have also since adopted rules allowing firms to list with multiple classes of shares.

Lyft declined to comment for this article. But while the company has granted more voting control to its two co-founders, it has taken some measures to mitigate over-consolidation in its governance. For instance, the company tapped Sean Aggarwal as an independent chairman of its board, who himself holds Class A shares.

—

Emily McCormick is a reporter for Yahoo Finance. Follow her on Twitter: @emily_mcck

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and reddit.

Read more from Emily:

S&P 500, Nasdaq close at highest level in 5 months

Boeing 737 Max groundings ‘pressure’ U.S. economic data: Wells Fargo

Beer sales are lukewarm and pot could be part of the problem