CPI, retail earnings - What you need to know for the week ahead

It was a tumultuous week for stocks following a busy week filled with the midterm elections, a Fed meeting and a slew of earnings.

The S&P 500 (^GSPC) fell 0.92%, or 25.82 points, as of market close, with the tech and communication services sectors leading declines. The Dow (^DJI) slipped 0.77%, or 201.92 points, after shedding more than 300 points at its intraday low. The tech-heavy Nasdaq (^IXIC) slid 1.65%, or 123.98 points.

The widely-expected outcome of the midterm election was for a split Congress with the Democrats in control of the House of Representatives, and the Republicans in control of the Senate. Many anticipate that this will in turn result in a “government gridlock.”

“The results of the midterm elections were largely as we expected, delivering a split Congress,” Barclays said in a note to clients on Friday. “The policy implications will become clearer over the coming weeks and months, but we expect less momentum behind additional fiscal stimulus … In all, we expect the current split to lead to more of a stalemate when it comes to fiscal policy which, in turn, reinforces our conviction that US economic growth has likely peaked and should moderate over time.”

Additionally, crude oil (CL=F) got pummeled for the tenth straight session on Friday and fell below $60 a barrel. The commodity is firmly in a bear market – down more than 20% from its high. Oil has been under pressure this week after U.S. sanctions on Iranian oil exports kicked back in on Monday, and further supply and demand concerns weighed on prices.

Monday the bond market will be closed in observance of Veteran’s Day, but the stock market will be open for a regular trading session.

The week in markets

The week will be a big week for retail earnings as earnings season slowly starts winding down.

“The majority of brick-and-mortar retailers will report results over the next two weeks. EPS for the group is expected to grow at 17.6% on the back of strong consumer demand and tax cuts,” Jonathan Golub, chief U.S. equity strategist at Credit Suisse said in a note to clients on Friday.

No companies are scheduled to report on Monday, but the rest of the week’s schedule will be as follows:

Tuesday: Home Depot (HD) before market open and Tilray (TLRY) after market close

Wednesday: Macy’s (M) before market open and Cisco (CSCO) after market close

Thursday: Walmart (WMT) and J.C.Penney (JCP) before market open; Nordstrom (JWN), Applied Materials (AMAT) and Nvidia (NVDA) after market close

Friday: Viacom (VIAB) before market open

On the economic data front, the October CPI data will be released on Wednesday. Economists are expecting that core inflation rose 2.5% over last year in October. Furthermore, initial jobless claims will be released on Thursday.

“Looking ahead, we expect price pressures to steadily build, as more businesses feel pressure from tariffs. Tariff effects may be drawn out, since businesses may have some ability to absorb increased costs, but with capacity tight, they may find it easier to pass on higher input costs to consumers. We expect the CPI to climb to 0.3% in October,” according to a Well’s Fargo note released on Friday.

Barclays expects energy to be a major headwind for October CPI. “Next week, we expect the October CPI report to show prices rose 0.3% m/m and 2.5% y/y at the headline level. However, we see energy as a significant headwind to overall inflation in 2019 and forecast headline CPI to slow to about 1.5% by the middle of next year, mainly on account of the energy drag.”

Economic calendar

Monday: U.S. bond markets will be closed for Veterans Day.

Tuesday: NFIB small business optimism, October (108.0 expected; 107.9 prior); Monthly budget statement, October (-$98.0B expected, $119.1B prior)

Wednesday: MBA mortgage applications for the week ending November 9 (-4.0% prior week); Consumer price index month-on-month, October (+0.3% expected, +0.1% prior); consumer price index ex food and energy month-on-month, October (+0.2% expected; +0.1% prior); consumer price index year-on-year, October (+2.5% expected, +2.3% prior); consumer price index ex food and energy year-on-year, October (+2.2% expected, +2.2% prior); Average weekly earnings year-on-year, October (+1.1% prior); average hourly earnings year-on-year, October (+0.5% prior)

Thursday: Empire Manufacturing, November (20.0 expected; 21.1 prior); Philadelphia Fed Business Optimism, November (20.0 expected; 22.2 prior); retail sales advance month-on-month, October (+0.6% expected; +0.1% prior); Import price index month-on-month, October (+0.1% expected, 0.5% prior); Import prices index year-on-year, October (+3.4% expected, +3.5% prior); Export price index month-on-month, October (+0.0% expected, +0.0% prior); Export price index year-on-year, October (+2.7% prior); Initial jobless claims for week ending November 10 (215K expected, 214K prior); Business inventories, September (0.3% expected, 0.5% prior)

Friday: Industrial Production, October (+0.2% expected, 0.3% prior)

Now, here’s what caught Myles’ eye:

The election did not change the story for the U.S. economy

The rocky month for the stock market and a bitter midterm election cycle did not shake U.S. consumers.

These events also did not change the biggest story for the U.S. economy as we approach 2019, which is that amid concerns over higher rates, stock market volatility, and the negative impacts from tariffs, consumer spending should remain solid. And when consumers are in good shape, it is hard for the economy to roll over.

On Friday, the University of Michigan released its latest reading on consumer sentiment, which included some responses gathered the day after this week’s midterm elections; responses collected after the election were in-line with those gathered beforehand, indicating a consensus election results did not move consumers to change their economic outlook.

“The unchanged data meant that the Sentiment Index remained higher thus far in 2018 (98.4) than in any prior year since 2000,” said Richard Curtin, chief economist for the survey. “The stability of consumer sentiment at high levels acts to mask some important underlying shifts. Income expectations have improved and consumers anticipate continued robust growth in employment, but consumers also anticipate rising inflation and higher interest rates.” (Emphasis ours.)

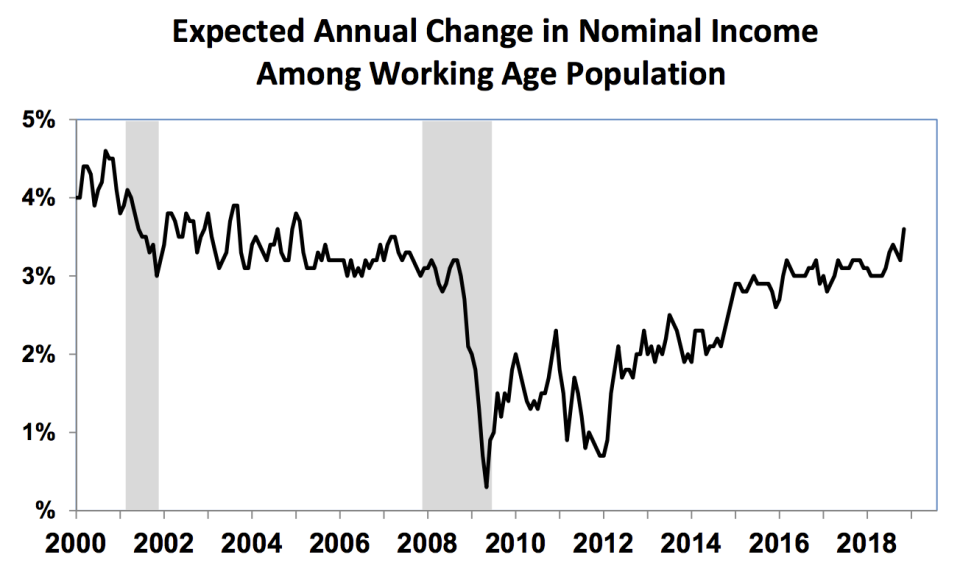

Friday’s data from the University of Michigan notably showed that expectations for wage increases over the next year from the working-age population, which covers those between the ages of 25 and 54, are now at their highest level since February 2005. More money in pockets of consumers means more money spent by consumers. A positive for overall economic growth.

In October, average hourly earnings growth hit 3.1%, the fastest pace of wage gains for workers since 2009. And with survey data suggesting that consumers remain both confident overall and expect their wages to rise, the consumer spending engine that accounts for 70% of overall GDP growth would appear likely to remain in good shape.

Heidi Chung is a reporter for Yahoo Finance. Follow her on Twitter: @heidi_chung.

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and reddit.

More from Heidi:

Investment strategist details ‘the thing that worries me most going into 2019’